The contrast between Staking and Credits in Onchain Market Applications

Staking imposes a real structural constraint on the lending market because it restricts the one thing these markets cannot function without: abundant and highly liquid collateral.

INSIGHTS

4/27/202613 min read

The contrast between Staking and Credits in Onchain Market Applications

Staking imposes a real structural constraint on the lending market because it restricts the one thing these markets cannot function without: abundant and highly liquid collateral.

Analysis • April 27, 2026

On-chain credit – the overlooked platform of DeFi

Just like in traditional finance, credit is the foundation of DeFi . It plays a central role in liquidity, driving growth for the entire onchain economy. However, much of the onchain discourse is overly focused on transaction speed and technical performance , thinking in terms of throughput and execution efficiency , while overlooking what truly supports real-world financial markets: credit. Without robust credit applications, decentralized finance would be nothing more than an empty shell. This is also true for traditional finance: the banking system , credit cooperatives , and lending institutions are the framework that supports the entire economy. Unlike decentralized exchanges (DEXs) , which perform best on high-performance chains and can operate with low liquidity, lending protocols generally require ample liquidity and high-quality assets to function optimally.

"No amount of throughput or block space can replace deep liquidity and high-quality assets. Ethereum , despite being one of the slowest and most expensive blockchains in history, is still leading the lending market – because it possesses sufficient quality assets and deep liquidity." __Core perspective from HCCVenture Research

Among the most active DeFi networks , Ethereum stands out as a prime example. Despite being one of the slowest and most expensive blockchains in history, it boasts the largest and most sustainable on-chain lending market , an ecosystem containing the most high-quality and liquid assets on the market. A crucial but often overlooked structural constraint in on-chain lending markets is the network's native staking mechanism . High staking rates reduce the supply of underlying assets , thereby limiting the potential for growth in the credit market. This report analyzes the subtle yet powerful relationship between staking dynamics and the development of the on-chain credit layer.

Layer 1 Economics - Two Competing Yields

On blockchains using a P roof-of-Stake mechanism like Ethereum and Solana , token holders face a crucial choice: where should they invest their assets to optimize returns? With native proof-of-stake ( PoS ) blockchain coins like ETH or SOL , two main sources of profit exist simultaneously and compete structurally:

Participate in the core protocol: Staking - secure your grid and receive block rewards.

Participating in the financial market: DeFi - lending, liquidity provision, and derivatives trading.

Over-allocating resources to one side will stifle the other. Despite workarounds through Liquid Staking Tokens (LSTs) , history shows users still favor staking – harming DeFi liquidity. Although Liquid Staking Tokens (LSTs) have emerged as a bridge – allowing users to both stake and participate in DeFi – the reality is that the majority of users still lean towards traditional staking, leading to an unintended consequence: a significant reduction in available capital for the DeFi market.

Why is staking always the most popular choice?

This bias has clear structural origins. Staking is enabled right from the network's launch, is not limited by scalability, requires less proactive effort, and offers more stable and predictable returns. Meanwhile, the DeFi ecosystem needs time to mature and always carries risks at both the market and application levels.

Furthermore, staking is " set and forget " – users simply lock their tokens and receive regular rewards, without constantly monitoring the market or worrying about liquidation. In contrast, DeFi requires deeper understanding, involves smart contract risks and market volatility, and takes time for the ecosystem to mature. The most serious consequence of staking gaining significant traction without a commensurate LST is:

A large amount of native assets are locked in validators , making them unusable for deployment in DeFi.

The shortage of quality assets forces lending applications down the risk curve , accepting lower-quality collateral such as memecoins or DAO tokens.

Protocols that require importing assets from other chains or tightening market parameters both limit efficiency and scale.

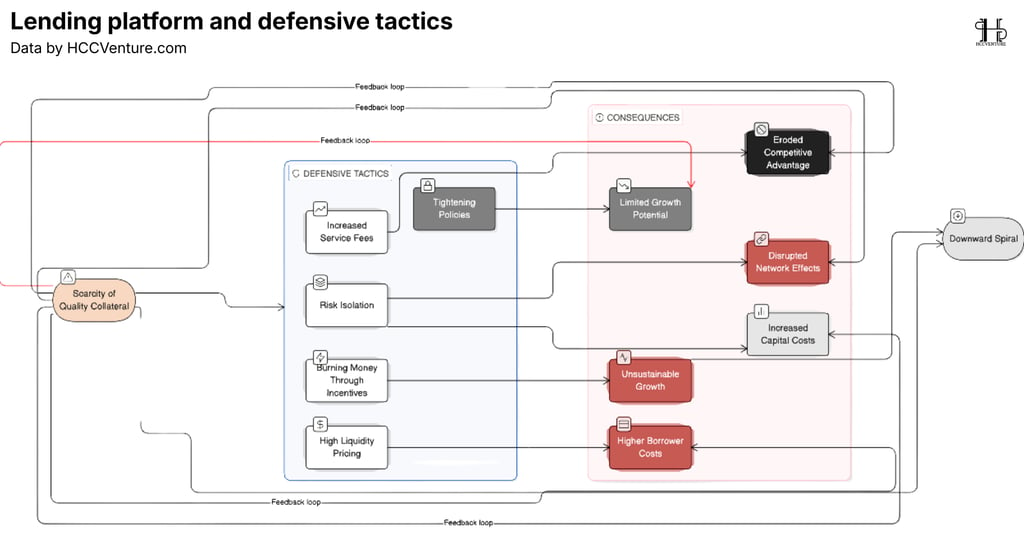

Domino effect when assets are locked up

For a lending market to thrive, it needs a prerequisite: a large reserve of reputable, easily tradable collateral assets. For L1 blockchains, this means the chain's native token (like ETH, SOL), its liquid staking versions (stETH, jitoSOL), and the financial products built on the platform. But when a large portion of native tokens are locked in staking without being converted into LST or liquid derivatives, a supply crisis occurs. The lending market suddenly lacks the high-quality " raw materials " needed to operate.

Faced with this situation, lending platforms are cornered and forced to choose between three imperfect options:

Option A: Lower Quality Standards. Accept riskier asset classes – meme tokens, DAO governance tokens – to maintain operations.

Option B: External Sourcing - Importing assets from other blockchains, typically wrapped Bitcoin. However, this creates dependency and cross-chain risks, and involves intense competition with other chains for the same limited capital.

Option C: Tighten Conditions - Apply more conservative parameters - reduce LTV (loan-to-value), limit loan limits, increase interest rates.

In an environment where quality collateral is scarce, lending platforms often have to combine multiple defensive tactics simultaneously:

Isolated Pools : Dividing liquidity into separate pools disrupts the network effect and increases the cost of capital.

Tightening policy : Establishing high safety thresholds, limiting the growth potential of both the platform and the underlying assets.

Paying a high price for liquidity : Offering attractive interest rates above market rates to attract stablecoin providers – but this means borrowers will incur higher costs.

Increasing service fees : Compensating for low revenue from limited volume by raising fee rates – further eroding competitive advantage.

Burning money through incentives : Spending heavily on token incentive programs to stimulate artificial growth – an unsustainable long-term strategy.

On newly launched blockchains, staking is the default option simply because there's nothing else to do. The staking architecture of the chain also plays a crucial role – a delegated PoS system with instant staking/unstaking capabilities encourages different behavior compared to validator-based models like Ethereum with withdrawal queues. When staking yields are too attractive, especially when accompanied by additional benefits like airdrops and reduced transaction fees, DeFi applications have almost no chance of competing in terms of absolute profitability.

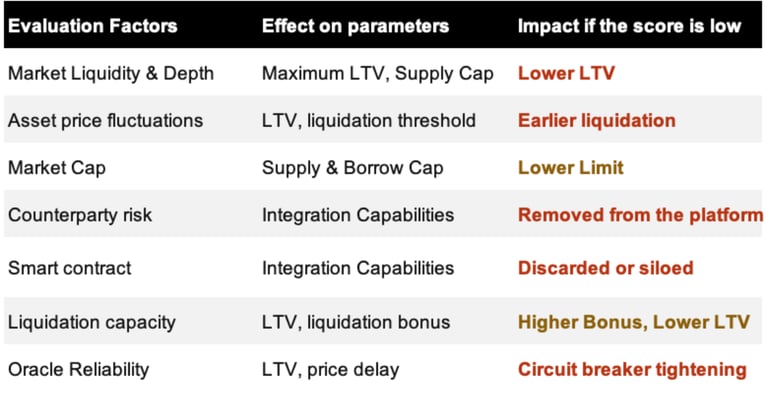

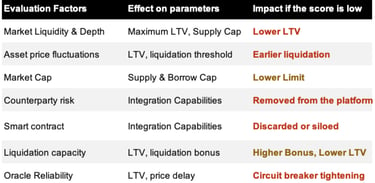

Asset quality and asset valuation parameters

To understand why high staking ratios are detrimental to the credit market, it's necessary to understand how lending protocols determine risk parameters. The quality and risk of collateral are assessed from multiple perspectives:

Low-quality assets will drag down the entire parameter system . When the majority of native assets are staking and the remainder are unqualified, protocols must compensate by imposing tighter parameter systems, which reduces both capital efficiency and the platform's attractiveness to borrowers.

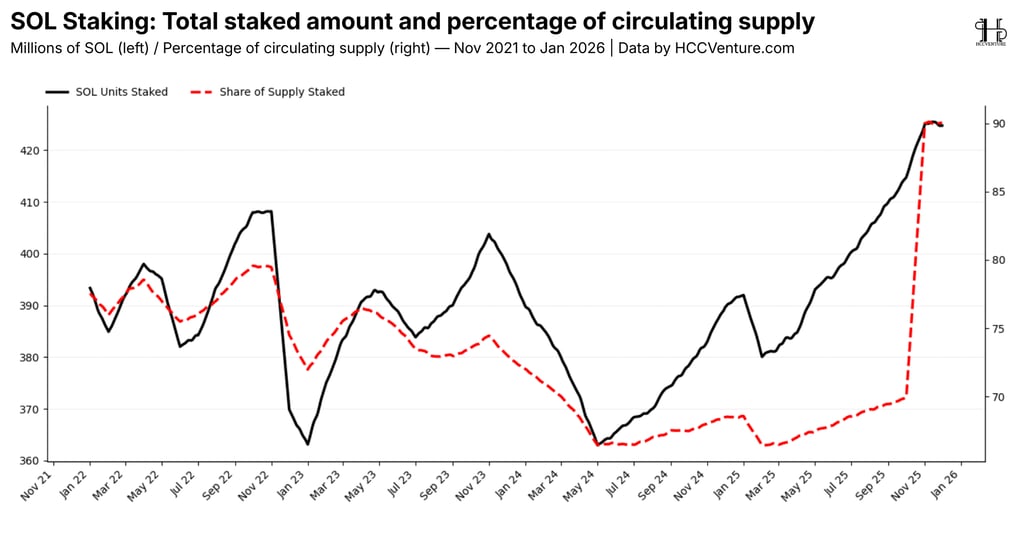

Solana's Core Staking Value

Solana represents an interesting case study – a blockchain that achieves impressive network performance but struggles with a less-noticed structural weakness: the depletion of underlying asset liquidity within the credit ecosystem. From a traditional metrics perspective, Solana is an undeniable success story. In terms of on-chain activity, the chain is among the world's leading – from the number of transactions processed to the trading volume on DEXs. The SOL token ranks 5th in market capitalization among all Layer-1 assets, accompanied by a large and active user community.

These achievements—high market capitalization, a large user base, a vibrant trading ecosystem—have created a veil that obscures the more serious problems occurring beneath the surface. These factors, in theory, should provide a favorable foundation for the lending market to thrive, eliminating much of the "noise" that often hinders smaller chains. But the reality is different.

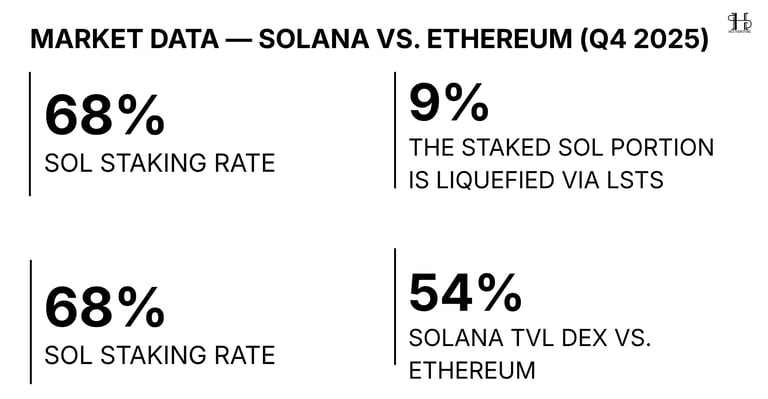

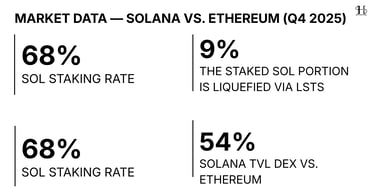

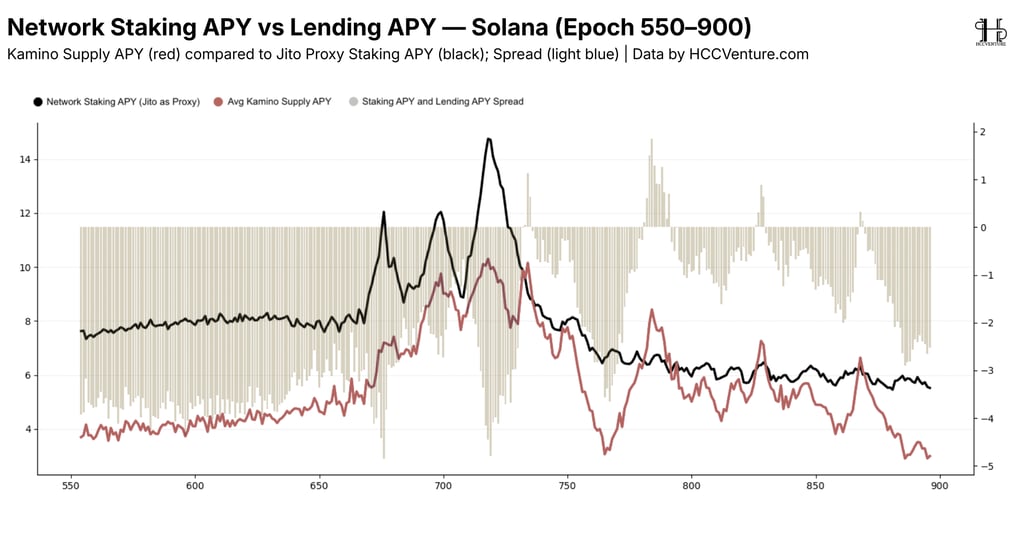

However, the resounding technical and trading success is obscuring one reality: staking is systematically stifling Solana's credit market . The 68% staking ratio on Solana, combined with only 9% of staked funds being liquified via LSTs, creates four negative synergistic effects:

The majority of the SOL supply is locked in validators, preventing access to DeFi.

Only a small fraction of staked assets are liquidated, limiting on-chain collateral.

The LST market is fragmented across more than a dozen providers, undermining the network effect.

With a staking yield of around 6% and an unstaking time of only about 48 hours, this creates a high opportunity cost for DeFi users.

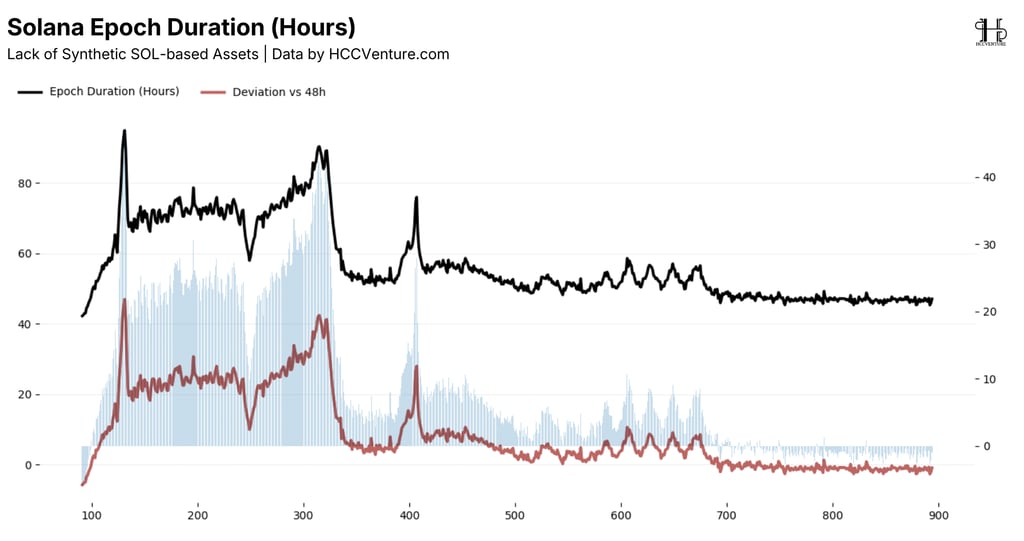

What makes the situation worse is Solana's epoch design, which allows for unstaking within approximately 48 hours. This means the liquidity risk of staking is almost negligible – users can " exit " quickly if needed.

Compared to Ethereum —where unstaking queues can stretch for weeks under congestion conditions—Solana's fast unstaking makes staking far more attractive than DeFi. Users ask: " Why take the risks of DeFi when I can stake safely, receive 6%, and withdraw within 2 days if needed? "

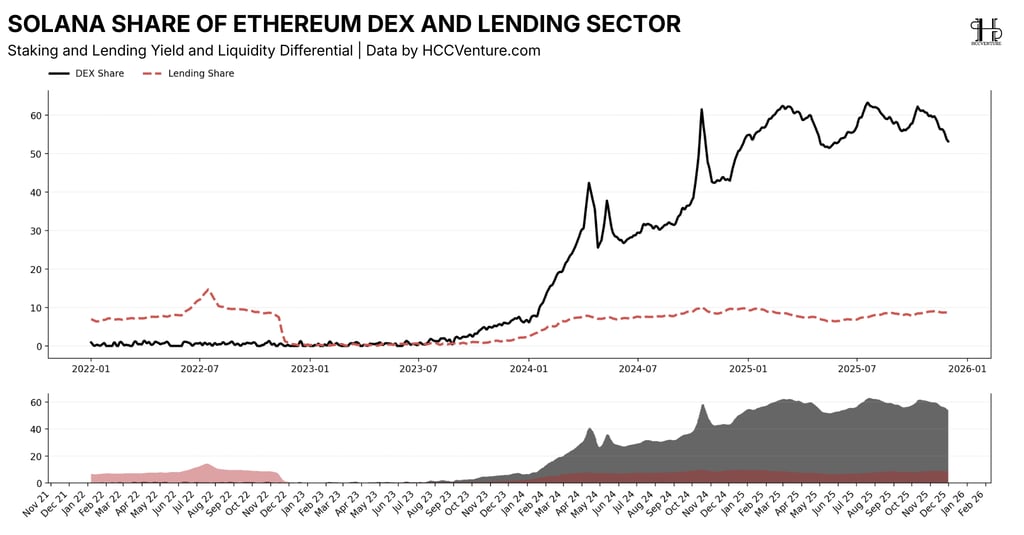

While Solana has established a clear competitive position on many fronts, from DEX transaction volume and relative market capitalization to network performance metrics like the number of transactions in its decentralized lending segment, the story is different. Solana's TVL in the lending sector still lags significantly behind Ethereum, and this disparity is not accidental. When compared side-by-side, the signal is quite clear: Solana DeFi's weakness lies in its liquidity depth and collateral diversity , not in its technical capabilities or user activity level.

The loan balance on Solana is only about 10% of that on Ethereum, with its historical peak not exceeding 18%. Meanwhile, the TVL of DEXs on Solana reaches 54% of Ethereum and is still growing. This divergence is not a contradiction; it reflects a structural characteristic: DEXs can operate efficiently even with a thin underlying asset base, because any token can be issued and priced on a minimal underlying liquidity layer, even without actual underlying assets. Credit markets do not have that flexibility.

When weighed against each other, the yields offered by DeFi lending protocols on Solana are often not attractive enough to offset the risks users bear, especially since native staking remains a much more competitive option. Data as of December 28, 2025, illustrates this quite clearly: the base SOL supply interest rate (excluding incentive rewards) fluctuates at 5.4% on Kamino , 2.8% on both Solend and Save , and 3.2% on JupLend , while native staking maintains a yield of around 6% with significantly lower risk margins.

In places where the protocol pushes the supply ratio beyond that threshold, the difference typically doesn't come from pure lending interest. Instead, the figure is inflated by a combination of token incentive rewards and liquid staking yields, meaning users must accept receiving rewards in tokens with a finite lifespan and susceptibility to dilution, or face double risk by participating in the protocol and staking simultaneously. Considering the yield risk, the advantage clearly favors direct staking.

Furthermore, Solana's withdrawal times are tied to epoch boundaries (approximately 432,000 slots). At the end of each epoch, all users who signaled their intention to withdraw within that period will receive their assets back. Since epoch 717 (December 2024), epochs have consistently lasted around two days, so users typically don't have to wait more than ~48 hours to access their staked SOL. With higher staking yields and minimal and predictable liquidity risk , the rationale for allocating SOL to lending applications, or DeFi in general, becomes even weaker. Another issue is Solana's complete lack of a synthetic asset ecosystem built on staking yields, which has been a huge growth driver for Ethereum . On Ethereum, Aave V3 Core has absorbed up to $7 billion in total assets ( Ethena PTs, sUSDe ) along with over $6 billion in liquid restaking tokens. Solana has not yet experienced comparable growth.

The only notable exception is the JLP token – a native synthetic asset Solana receives from providing liquidity to the Jupiter Perps Pool, but JLP remains a volatile asset, unlike the stable Pendle PTs on Ethereum which allow for loop strategies that scale borrow activity. The divergence between DEX and lending on Solana speaks volumes. Solana's DEX TVL is 54% of Ethereum's and continues to rise. Lending TVL is only 10% and once peaked at 18%. This confirms that Solana has liquidity and asset issues, not technological or operational ones . DEXs can operate with a thinner underlying asset liquidity layer than any token that can be created and traded. But the credit market requires deep and high-quality collateral to scale.

The Ethereum model and lessons from history

Ethereum began as a Proof-of-Work (PoW) chain, where network security is completely independent of the native assets. This has key implications: without staking mechanisms , the entire theoretically circulating supply of ETH can be deployed to lending protocols. There are no competing yield benchmarks, and the only way for ETH holders to earn profits on-chain is through DeFi with market-determined interest rates. The PoW mechanism also incentivizes supply circulation as miners continuously sell ETH to cover operating costs.

POS Validator Design - Friction leads to LST

When Ethereum transitioned to PoS, it opted for a validator-based model instead of delegated PoS. This design set a minimum threshold of 32 ETH to run a validator – a significant capital barrier that forced those with less to seek pooling solutions like Lido, Rocket Pool, or Origin. All of these issued LSTs. Furthermore, from December 2020 to the Shanghai upgrade in April 2023, staked ETH could not be withdrawn; those who did not want their capital locked indefinitely were forced to stake through LSTs. As a result, by the time Shanghai activated, 19.14 million ETH had been staked, with nearly a third through Lido in the form of stETH.

The queue mechanism creates a sudden change when inconvenience occurs.

Ethereum uses a controlled queue mechanism for staking and unstaking ETH as a security measure. While offering clear security benefits, it creates uncertainty and liquidity risk surrounding staked ETH. At certain times, the ETH unstake process took up to 46 days, and staking up to 71 days. This inconvenience is precisely what drives users to DeFi to earn passive income on ETH instead of facing the risks and uncertainty of queues.

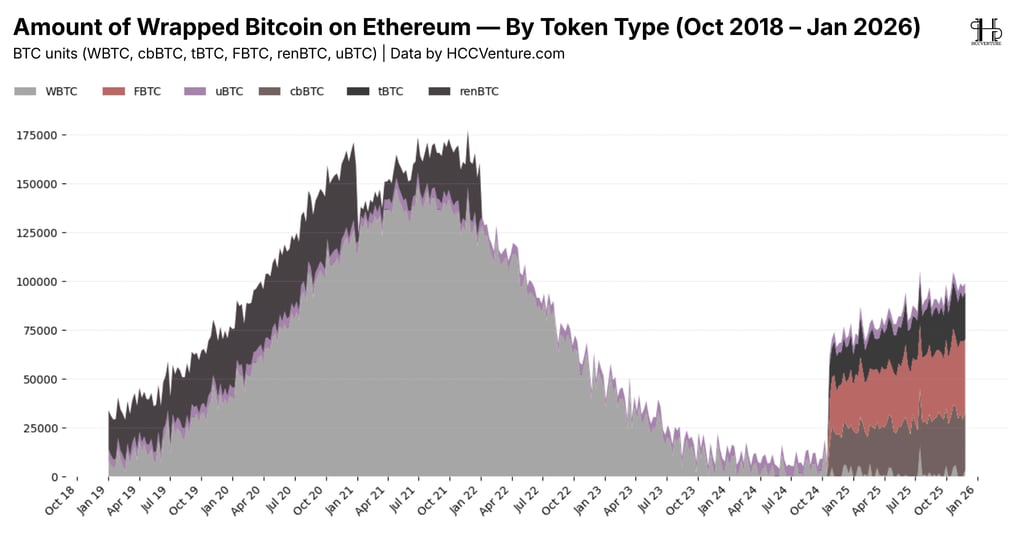

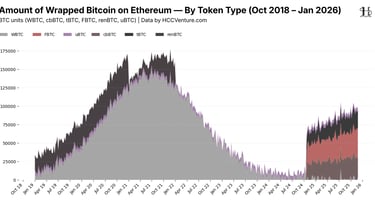

Using exogenous assets Wrapped Bitcoin as leverage

Ethereum quickly integrated wrapped bitcoin into its lending market. When WBTC began gaining significant traction in 2019–2020, Ethereum was the dominant smart contract platform with a mature wallet infrastructure and established onboarding flows from centralized exchanges. No other chain could compete. Today, wrapped bitcoin remains the core collateral in the Ethereum lending market, with billions of dollars offered on Aave, Sky, and Morpho—an exogenous platform that scales Ethereum credit far beyond the limits of native assets.

Overall, high-quality, "mobile" collateral assets, such as packaged Bitcoin tokens, are relatively finite and actively seeking to be used in DeFi. Therefore, attempts to import this type of asset ultimately redistribute rather than add, where the loss of one chain or asset benefits another. If the WBTC fallout hadn't occurred, it's unclear whether the question of needing an alternative to WBTC would ever have arisen. The high liquidity of stablecoins attracts BTC collateral, thereby reinforcing the depth and security of stablecoins, creating a self-reinforcing cycle. Breaking this cycle poses a significant challenge to emerging ecosystems.

Solutions to escape the Staking trap

Reduce staking APY by cutting inflation.

By slowing down the rate of new token issuance (inflation), networks narrow the automatic yield advantage of staking. This also weakens the pure staking incentive to offset dilution. More importantly, it narrows the gap between DeFi yield and staking yield, both in absolute and relative terms.

However, this is not a panacea. Decisions to cut inflation are highly political and difficult to reach consensus on, especially on networks with many established stakeholders. And for some chains with fast unstaking mechanisms, the risk-adjusted advantage of staking may still persist even after a reduction in APY.

Importing high-quality collateral assets.

If an ecosystem lacks quality collateral, it can import from another chain. Wrapped bitcoin is the most popular option due to asset size, the absence of Bitcoin in native DeFi, and the decentralized nature of the holding community. But this path is fraught with obstacles.

The market is inherently opportunistic and highly competitive. A user pledging cbBTC to borrow USDC will simply go to the place with the best parameters, lowest cost, and deepest liquidity, regardless of the chain. Ethereum currently dominates in all three dimensions: stablecoin depth, borrowing cost, and LTV ratio.

Furthermore, once a borrow position is opened, the collateral becomes "sticky" but difficult to move because it is locked until the loan is repaid. This creates a significant incumbent advantage for Ethereum and makes it difficult to challenge its position.

Tailwind important from SEC Clarity LST

In August 2025, the U.S. Securities and Exchange Commission (SEC) confirmed that liquid staking activities surrounding " Protocol Staking " do not constitute the offering of securities under the Securities and Exchange Act of 1933 or the Securities and Exchange Act of 1934. This is a significant legal signal, paving the way for institutions that had been staking but avoided LSTs due to regulatory concerns to now participate in the LST market with greater confidence. As a result, more staked assets can be liquidated, increasing the collateral available for the credit market.

This guidance, while an external driver of potential growth in the on-chain lending market, is a crucial alternative driver for DeFi liquidity and the creation of synthetic collateral. The clarity from the SEC could encourage more staked supply to be liquidated, making underlying assets more readily available in the credit market or DeFi in general. While not a panacea for ecosystems struggling with high staking rates, the legal clarity surrounding LSTs is a powerful driver that could enhance liquidity, strengthen collateral diversification, and accelerate the development of lending applications.

Conclusion: Collateral is everything

Ultimately, staking creates a real constraint on the lending market because it restricts the one thing these markets cannot function without: abundant and negotiable collateral. Successful chains will be those that break down the collateral cyclical barrier, enabling scalability, borrowing demand, and the emergence of new collateral types. Ethereum's history shows that when native assets are freely deployed into DeFi, collateral generates more collateral, and the lending market expands accordingly. This isn't just a lesson for Solana—it's the framework for assessing the credit potential of any emerging L1 PoS.

Glossary of terms:

Stake Rate: The percentage of circulating supply that is staked, different from Staking APR (yield paid to stakers).

LST: Liquid Staking Token, a token representing staked assets, is tradable and can be used as collateral.

LTV: Loan-to-Value, the maximum ratio of the loan amount to the value of the collateral.

Supply Cap: The limit on the total amount of assets that can be provided to a lending protocol.

Siloed Design: A market structure that is segregated, preventing collateral from one pool from affecting another, often due to the risk of low asset quality.

Disclaimer: The information presented in this article is the author's personal opinion in the field of cryptocurrency. This is not financial or investment advice. All investment decisions should be based on careful consideration of your personal portfolio and risk tolerance. The views expressed in this article do not represent the official stance of the platform. We recommend that readers conduct their own research and consult with experts before making any investment decisions.

API & Dữ liệu: Dune, Atermis, Tokenterminal, Solanascan

Compiled and analyzed by HCCVenture

Join the HCCVenture organization here: https://link3.to/holdcoincventure

Research and Analysis

On-chain credit – the overlooked platform of DeFi.

Layer 1 Economics - Two Competing Yields

Why is staking always the most popular choice?

Domino effect when assets are locked up

Asset quality and asset valuation parameters

Solana's Core Staking Value

The Ethereum model and lessons from history.

POS Validator Design - Friction leads to LST

The queue mechanism creates a sudden change when inconvenience occurs.

Using exogenous assets Wrapped Bitcoin as leverage

Solutions to escape the Staking trap

Reduce staking APY by cutting inflation.

Importing high-quality collateral assets.

Tailwind important from SEC Clarity LST

Conclusion: Collateral is everything.

Explore HCCVenture group

HCCVenture © 2023. All rights reserved.

Connect with us

Popular content

Contact to us

E-mail : sp_contact@hccventure.com

Register : https://linktr.ee/holdcoincventure

Disclaimer: The information on this website is for informational purposes only and should not be considered investment advice. We are not responsible for any risks or losses arising from investment decisions based on the content here.

TERMS AND CONDITIONS • CUSTOMER PROTECTION POLICY

ANALYTICAL AND NEWS CONTENT IS COMPILED AND PROVIDED BY EXPERTS IN THE FIELD OF DIGITAL FINANCE AND BLOCKCHAIN BELONGING TO HCCVENTURE ORGANIZATION, INCLUDING OWNERSHIP OF THE CONTENT.

RESPONSIBLE FOR MANAGING ALL CONTENT AND ANALYSIS: HCCVENTURE FOUNDER - TRUONG MINH HUY

Read warnings about scams and phishing emails — REPORT A PROBLEM WITH OUR SITE.