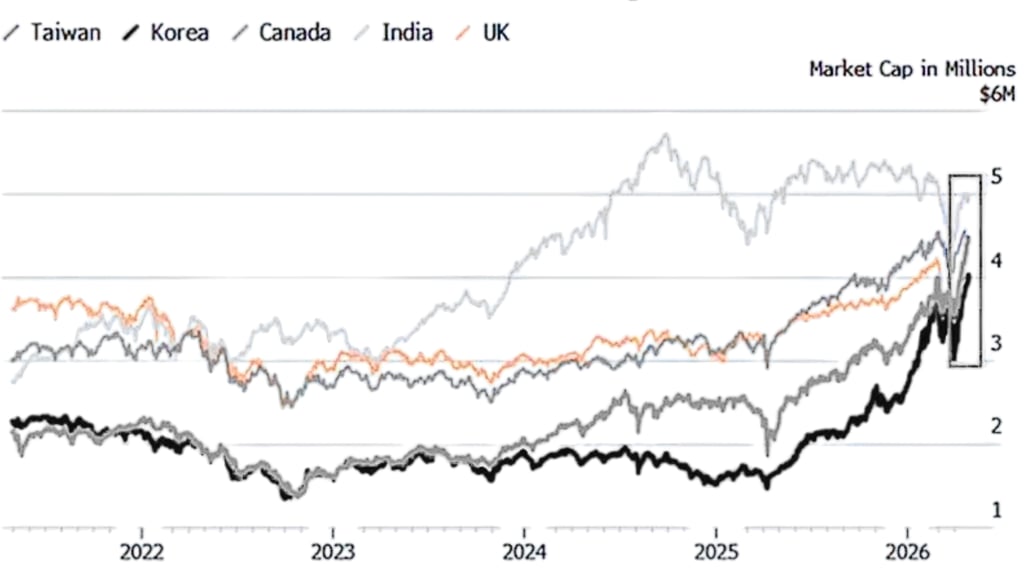

Taiwan has surpassed India to become the 5th largest stock market

Taiwan's surpassing India in market capitalization shows a wider shift in emerging stock market dynamics, where exposure to technology hardware and artificial intelligence.

5/27/20264 min read

The continuous growth of TSMC Taiwan

The increase in the stock price of Taiwan Semiconductor Manufacturing Company (TSMC) is the main driving force that helps Taiwan surpass India in total market capitalization, with the world's largest contract-based chip manufacturer benefiting disproportionately from the sustainable global demand for advanced semiconductors used in artificial intelligence systems, data centers and high-performance computing applications.

The company's 49% increase in 2026 has pushed the market capitalization to the scale of trillions of dollars, while raising Taiwan's overall market value through mathematical effects, in which a single component accounts for more than 40% of the benchmark has a great impact on total capitalization regardless of the size or depth of the wider market in other sectors.

This focus creates an unusual momentum in which Taiwan's stock market performance depends significantly on global awareness of the sustainability of AI infrastructure construction and TSMC's competitive position in the semiconductor manufacturing sector, rather than reflecting Taiwan's comprehensive economic activity on a diverse industrial basis.

This phenomenon reflects several historical periods in other markets, where dominant technology companies achieved a similar level of index concentration, including Nokia's highest proportion on the Finnish stock market during the mobile phone boom or Samsung Electronics' sustainable dominance over Korean stock indexes, but is a relatively new phenomenon for a market of absolute scale like Taiwan when show extreme dependence on a single stock.

Structural differences in market structure

Taiwan's semiconductor-focused market structure is in stark contrast to India's more balanced industry structure, which spans across the banking, energy, consumer goods, industry and service sectors, creating fundamentally distinct risk-return profiles, attracting different groups of investors depending on the macro-economic cycle phase and current thematic preferences.

The focus on technology hardware helps the Taiwan market capture most of the capital flow during the investment phases in AI infrastructure that governs global equity allocation decisions, but also exposes investors with greater downside risks as the cycle of inverted semiconductor demand or alternative technologies appear to challenge existing manufacturing platforms. India's diversification brings stability in specific industry-specific corrections but limits participation in the uptrend as narrow topics such as AI hardware have high valuations.

Structural differences explain much of the recent performance difference, with global investors prioritizing direct exposure to semiconductor manufacturing value chains rather than broader economic growth stories with no direct connection to artificial intelligence development. The Taiwan market leverages TSMC's position as an essential supplier of advanced processing chips needed for training large-scale language models, implementing inference systems, and supporting data center infrastructure that powers AI applications, while India's technology sector is primarily focused on software services, IT outsourcing, and digital platforms that benefit from apply AI but do not produce important hardware for the technology transition. This difference is profoundly significant when capital flow focuses on companies that earn direct revenue from spending on AI infrastructure rather than indirect beneficiaries whose benefits are realized for a longer period of time.

Exchange rate fluctuations and the impact of import costs

The prolonged weakening of the rupee throughout 2025 and early 2026 has created more obstacles to stock market performance by increasing the cost of importing crude oil, electronic goods and industrial goods that India buys on the dollar-valued market, with high energy prices particularly affecting inflation dynamics and limiting the flexibility of the Reserve Bank of India's monetary policy.

Brent oil prices traded between $85 and 95 in early 2026, combined with a weaker rupee, pushed up domestic fuel costs, raising concerns about inflation, making it difficult for the central bank's efforts to support growth through interest rate adjustments without affecting the task of price stability. This inflationary momentum caused by imports distinguishes India from emerging markets that export energy that benefit from the strength of commodity prices.

The current account deficit expanded to 1.8% of GDP in the fourth quarter of 2025 reflecting the structural challenge, in which import demand continuously exceeds export income plus remittance flows, requiring continuous foreign capital to finance the gap and maintain exchange rate stability.

Foreign direct investment (FDI) flows decreased to $15.2 billion in the first two months of 2025 compared to $18.7 billion in the same period last year, reducing the natural dollar inflow supporting the rupee, making the currency more vulnerable to investment capital flows as foreign institutional investors rebalance their portfolio from Indian stocks. Financial challenges become more severe in periods when both FDI and FPI fall, eliminating offset capital flows that often help minimize the impact of exchange rates.

Taiwan's vulnerability before the semiconductor industry cycle

The focus of the Taiwan market on TSMC not only makes investors affected by the semiconductor demand cycle but also the geopolitical tension around the Taiwan Strait, which periodically escalates and creates higher risks for Taiwan's assets despite the strong corporate fundamentals. This focus means that global events affecting the semiconductor industry in general or the political situation of Taiwan in particular can cause unusually large index fluctuations, unrelated to the performance of most member companies, because the 42% weight of TSMC in the benchmark index transmits external shocks throughout the market regardless of the prospects of banking, retail or industrial companies.

Exposure to the semiconductor industry carries cycle risks due to the industry's historical model of building production capacity, then oversupply adjustment as demand growth does not absorb expanding output, although the current AI infrastructure investment cycle seems to maintain a strong utilization rate and pricing power, which distinguishes it from the typical recessions of the memory industry or commodity logic.

TSMC's ability to lead in advanced chip manufacturing technology and manufacturing complexity creates barriers to the rapid expansion of production capacity of competitors, potentially extending the current cycle beyond historical time as super-scale data center operators and cloud infrastructure providers maintain a robust deployment schedule to support the sustainable demand for advanced chips. Time uncertainty creates analytical challenges, in which the optimistic scenario assumes that the construction of AI infrastructure lasts for many years, while the pessimistic scenario predicts that demand will soon normalize or competitive pressure reduces profits.

Disclaimer: The information presented in this article is the author's personal opinion in the field of cryptocurrencies. This is not financial or investment advice at all. Every investment decision should be based on careful consideration of your personal portfolio and risk tolerance. The opinion in the article does not represent the official position of the platform. We recommend that readers do their own research and consult experts before making any investment decisions.

Synthesized and analyzed by HCCVenture

Follow HCCVenture organization here: https://link3.to/holdcoincventure

Explore HCCVenture group

HCCVenture © 2023. All rights reserved.

Connect with us

Popular content

Contact to us

E-mail : sp_contact@hccventure.com

Register : https://linktr.ee/holdcoincventure

Disclaimer: The information on this website is for informational purposes only and should not be considered investment advice. We are not responsible for any risks or losses arising from investment decisions based on the content here.

TERMS AND CONDITIONS • CUSTOMER PROTECTION POLICY

ANALYTICAL AND NEWS CONTENT IS COMPILED AND PROVIDED BY EXPERTS IN THE FIELD OF DIGITAL FINANCE AND BLOCKCHAIN BELONGING TO HCCVENTURE ORGANIZATION, INCLUDING OWNERSHIP OF THE CONTENT.

RESPONSIBLE FOR MANAGING ALL CONTENT AND ANALYSIS: HCCVENTURE FOUNDER - TRUONG MINH HUY

Read warnings about scams and phishing emails — REPORT A PROBLEM WITH OUR SITE.