Report from PWG US – A turning point in Crypto asset legal policy

The PWG is the opening chapter of 21st century digital asset law, defining how the US will lead the world in crypto, stablecoins, DeFi. It combines financial freedom, USD stability, and global policy innovation.

INSIGHTS

11/13/202510 min read

Find out what a report from PWG is?

The President's Working Group on Digital Asset Markets (PWG) is a task force established by the White House to develop a comprehensive digital asset strategy for the United States. The 166-page PWG report marks the first time the US government has implemented a comprehensive legal framework for crypto , instead of just issuing fragmented guidance through agencies like the SEC or CFTC .

PWG is also an important milestone in how the US views crypto: no longer just a speculative tool, but a next-generation financial infrastructure, with an “open market & innovation first” philosophy , opening up innovation while maintaining the national financial order.

Contents of the PWG report

The group was established pursuant to Executive Order 14178 , with the goal of defining a comprehensive strategic vision for blockchain, stablecoins, DeFi, and other digital asset applications in an increasingly competitive global environment. The primary concerns are financial stability, protecting the position of the US dollar, while not stifling technological innovation. The PWG represents the US effort to establish a transparent, unified, and predictable regulatory framework that allows businesses and investors to operate safely in the volatile crypto market.

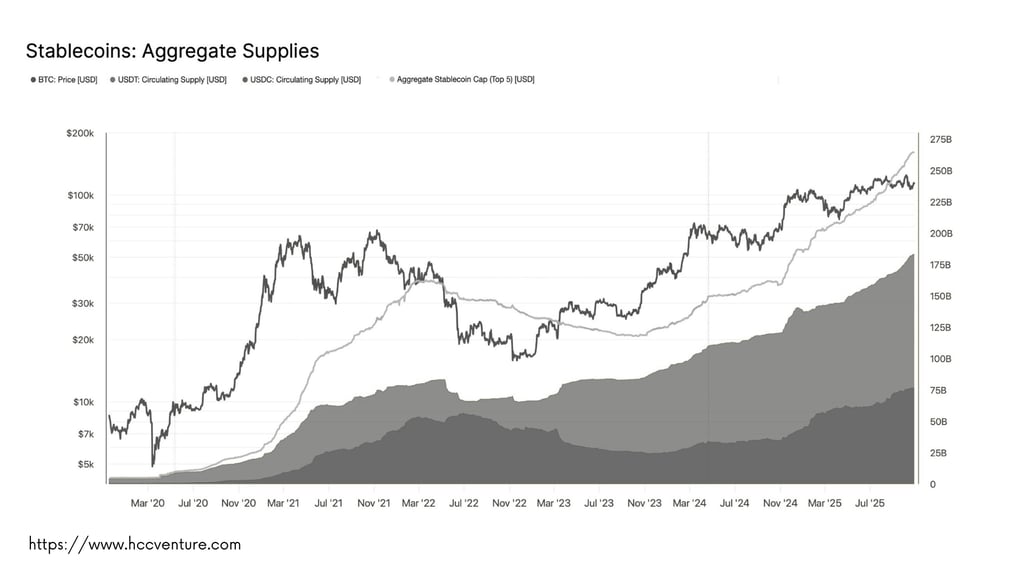

According to CoinMarketCap 2025 data , the stablecoin capitalization has exceeded $230 billion , accounting for about 12% of the total crypto market capitalization. Meanwhile, the total value locked (TVL) in DeFi platforms is estimated at about $120 billion , indicating that DeFi and stablecoins have become important financial ecosystems. These figures reflect the rapid growth and global influence of the crypto market, and highlight the urgent need for a comprehensive legal framework to protect USD, support innovation, and mitigate systemic risks. The chairman of the compilation group, David Sacks , emphasized that:

“Digital assets are no longer a speculative niche. They are foundational to the next generation of financial infrastructure.”

(Translation: Digital assets are no longer speculative – they are the foundation of next-generation financial infrastructure.)

The PWG has been called by the international community as America’s first “Crypto Blueprint” , demonstrating the United States’ strategic commitment to putting blockchain at the heart of national economic policy. The global context is also a factor in understanding the significance of the PWG:

China has rolled out e-CNY , with a centralized CBDC model, full control of transactions, and is expanding testing in many provinces and cities, to strengthen national financial control.

The European Union (EU) is developing a MiCA framework that emphasizes investor protection over promoting innovation, with strict registration and transparency rules, expected to be fully implemented by 2025.

Singapore (MAS sandbox) tests fintech and crypto solutions on a smaller scale, focusing on innovation, but still maintaining strict AML and stability requirements.

In this context, PWG affirms the US position : both protecting the global USD advantage and facilitating the development of transparent, flexible, and innovative blockchain solutions. The US strategy is based on the philosophy of “open market & innovation first” , which means opening up to innovation while maintaining the national financial order, encouraging global competition, and laying the legal foundation for sustainable development of crypto and DeFi projects.

It can be concluded that PWG is an important milestone, marking the US officially considering crypto as economic infrastructure , no longer just a speculative tool. From here, all policies on blockchain, stablecoin, DeFi, tax and digital asset management are shaped according to the philosophy of combining innovation and risk management , opening a new era for the digital finance industry in the US and globally.

Overall goals

The PWG proposes to focus on four main core policy directions :

Promote open innovation and transparent blockchain-based global competition, including supporting open networks and innovation exemption programs to encourage development without the constraints of legacy regulation.

Protect USD position through stablecoins instead of state-issued CBDCs, with a ban on CBDC issuance to avoid centralized control.

Respect for personal financial freedom, especially the right to self-custody, ensuring individuals have control over their assets without interference.

Ensure financial stability through a flexible supervisory framework that does not stifle innovation, with a focus on systemic risk management and public-private partnership.

PWG emphasizes that the US does not apply a total control model like China but chooses a market-driven approach . This both encourages innovation and protects the global position of the USD. Stablecoins are seen as a soft weapon of the USD, while self-custody is the foundation for personal financial freedom .

Globally, this approach helps the US maintain a competitive advantage over China with e-CNY – which is being tested in many provinces, and the EU with Digital Euro being deployed under the MiCA framework.

The tension between security and privacy becomes central to the discussion of illicit finance, as policymakers and regulators struggle to find a delicate balance between protecting national interests and preserving individual liberties. This push-pull is most evident in the fact that mixing services are mentioned only once in the entire recommendation, and even when they appear, the Inter-Agency Working Group (PWG) avoids taking a definitive position. Instead, it only suggests that regulators should “ evaluate next steps .”

Meanwhile, the assessment of decentralized finance (DeFi) takes a more robust tone, particularly regarding the compliance responsibilities of service providers under the Bank Secrecy Act (BSA) and the regulatory directions outlined in the bill on futures market structures. The report outlines a set of four criteria to determine whether a software application is subject to regulation, and clearly highlights the expectations and limitations of the so-called “promise” of DeFi.

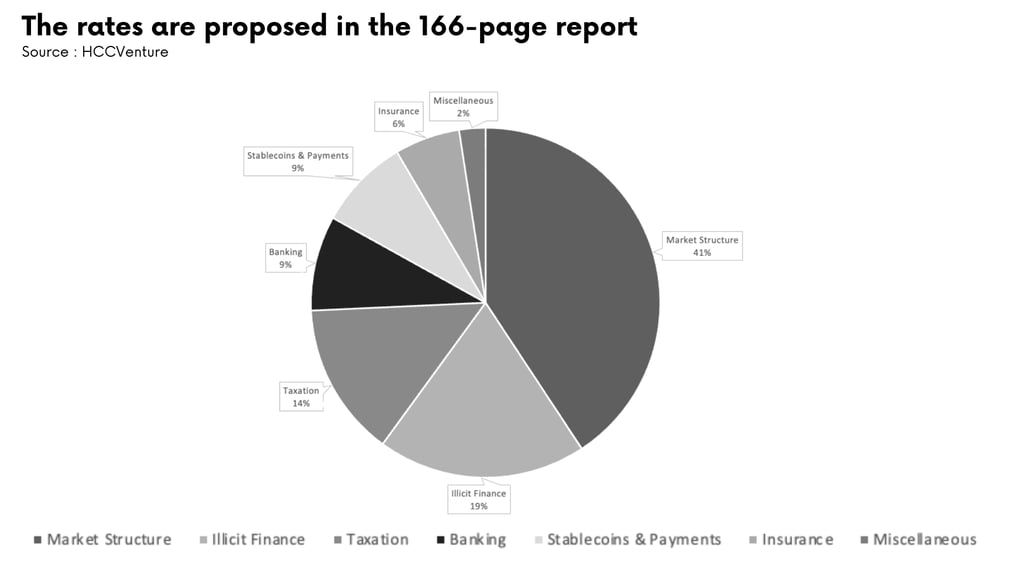

Market structure

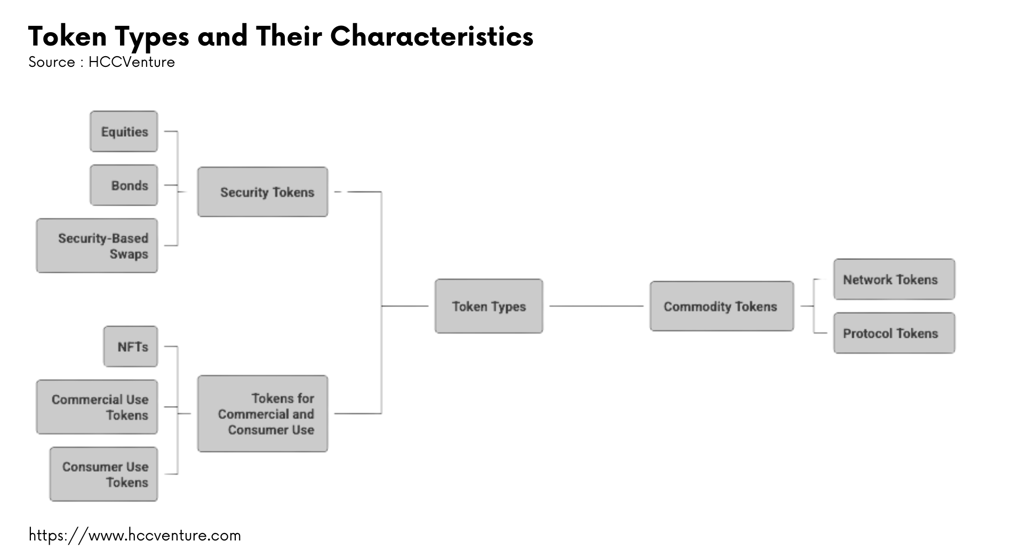

In this proposal, the report envisions a clear classification mechanism, according to which digital assets are divided into three groups: security tokens, commodity tokens, and tokens for commercial or consumer purposes.

PWG clearly defines the roles of management agencies:

CFTC: Spot market monitoring for non-securities crypto (BTC, ETH, LTC…).

SEC: Focuses on security tokens , which represent shares, profits, or investment contracts.

The report introduces three groups of tokens: Security, Commodity, Commercial/Consumer Use, addressing a long-standing legal conflict.

Security Tokens: Some digital assets are considered securities, which are assets that represent interests in stocks, bonds, or security-based swaps. Security tokens are also digital assets that are offered and sold as part of an investment contract and are subject to the “Howey Test” and the Securities Act of 1933.

Commodity Tokens: Some digital assets are the underlying commodity for regulated derivatives transactions or represent a derivative product themselves, subject to the Commodity Exchange Act.

Tokens for Commercial and Consumer Uses: Tokens used for commercial or consumer purposes provide access to certain specific goods, services, or privileges and are subject to other federal and state laws applicable to commercial transactions.

The PWG report devotes a significant portion of its review to the framework for the division of authority between the SEC and CFTC in the context of the digital asset market structure bills being considered by Congress. The report argues that the CFTC should be given explicit regulatory authority over the spot market for non-securities digital assets — a core feature of the House’s proposed CLARITY Act. Previously, the CFTC had only direct jurisdiction over derivatives, not the spot market for the underlying commodity, except for enforcement powers related to fraud.

In the corresponding section of the report, the CLARITY Act is repeatedly mentioned as a viable and highly applicable model. PWG even devotes an entire subsection to analyzing the outstanding advantages of this bill. Although CLARITY is the central legal document used as a benchmark in the discussion of market structure, PWG also notes that the Senate draft of the Responsible Finance Innovation Act (RFIA) had not yet been released at the time the report was prepared. However, much of the report—which is based on CLARITY—is significantly aligned with the policy direction envisioned in the RFIA.

DeFi – A New Approach

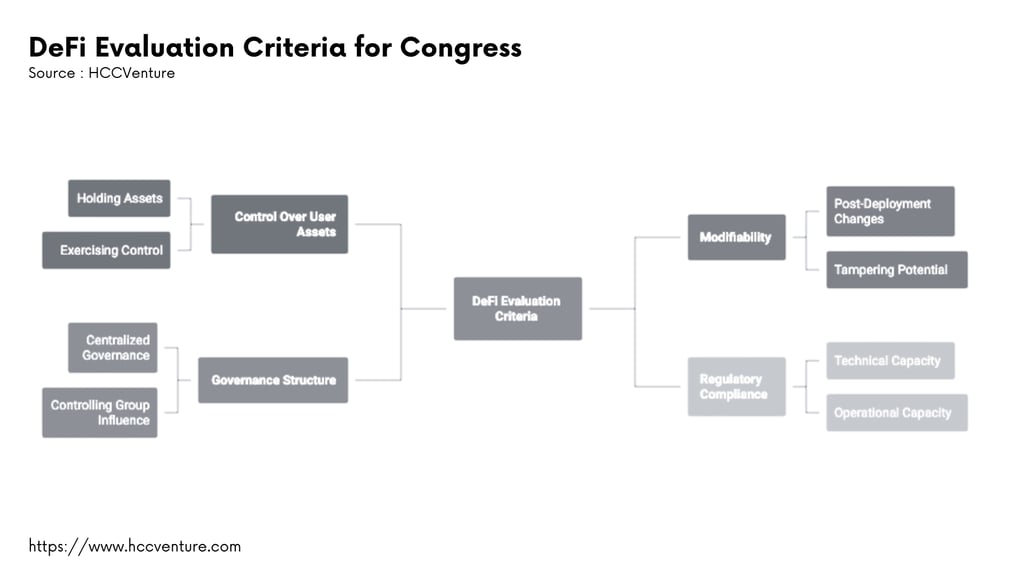

The final section of the market structure section outlines four practical criteria that Congress should consider when evaluating DeFi models. The report says these four criteria directly reflect the approach of the CLARITY Act. Specifically, the proposed factors include the extent to which:

(1) The software application holds or exercises any form of “ control ” over the user's assets.

(2) The Application may be modified or altered after it has been completed or deployed.

(3) The application operates under a centralized governance structure or is subject to the control of a specific control group.

(4) The application has the technical or operational capability to meet regulatory compliance requirements under the current legal framework.

PWG first recognized DeFi as a model with socio-economic value , rather than just a high-risk area:

Regulatory Sandbox and Safe Harbor allow experimentation within a limited regulatory framework, allowing DeFi projects to grow without immediate punishment.

Governance tokens and community governance mechanisms help legitimize decentralization, with standards to determine the true level of decentralization.

Build a DeFi KYC Framework standard, coordinate agencies to ensure AML, including integration with on-chain tracking tools.

The proactive adoption of the four-factor test to evaluate DeFi shows that the US government is moving to a more robust and consistent stance, acknowledging that DeFi possesses distinct characteristics that need to be regulated through an appropriate framework.

This view is further reinforced by the public report expressing support for the CLARITY Act as well as “the promise of decentralized finance and the ability of software to empower individuals to transact freely with each other.” The report also notes the “essential role” of decentralized governance mechanisms in coordinating and maintaining the operation of the entire blockchain network.

Money Laundering & Privacy (Illicit Finance)

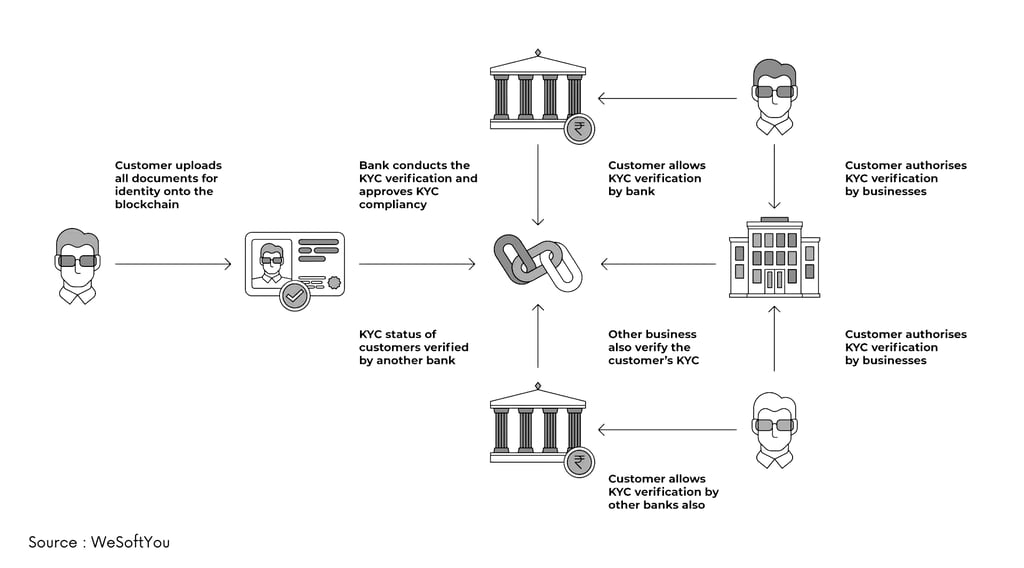

For anti-money laundering (AML) and counter-terrorism financing (CFT) policies, the working group report codifies existing regulations that may apply to digital assets, and proposes additional measures to strengthen the legal framework.

First, the report highlights the need for early implementation of the GENIUS Act, which would require regulated stablecoin issuers to be recognized as financial institutions under the Bank Secrecy Act (BSA). Next, the report recommends enacting a market structure law that would establish specialized types of financial institutions for the cryptocurrency sector within the BSA’s regulatory remit.

PWG updates the Bank Secrecy Act (BSA) to include new crypto institutions, applying AML/KYC to on-chain transactions and non-custodial services.

No ban on mixers but reporting required if there are signs of money laundering, with FinCEN building a new blockchain-compatible AML framework.

FinCEN builds new blockchain-compatible AML framework. Enhances international cooperation to track illicit money flows, while still recognizing legitimate privacy rights.

This is the first time the US has recognized the legal right to financial privacy, paving the way for a rewrite of the BSA in the spirit of Web3, while reducing the risk from illegal activities estimated to account for 0.15-0.34% of total crypto transactions.

Separate tax for digital assets (Taxation)

In its tax discussion, the PWG report recommends that Congress establish a new tax classification specifically for digital assets, and adjust existing tax rules that apply to commodities or securities to reflect the true nature of these assets.

Because the GENIUS Act does not provide guidance on the tax treatment of stablecoins, PWG recommends that future legislation clearly define how stablecoin payment transactions will be classified for federal income tax purposes.

Proposal to apply wash sale rule for crypto to prevent circumvention of the law, prevent selling at a loss and then buying back immediately.

Stablecoins are treated as cash equivalents in tax returns, simplifying reporting.

Tax timing for mining/staking is shifted to when selling, reducing the burden on users.

IRS develops wallet-integrated automated filing system, with new guidance for ETFs and staking funds.

Crypto is officially considered a legitimate asset with a transparent tax framework, which helps encourage innovation without stifling the market, especially after the IRS allowed profit-sharing staking ETFs.

Adjusting the taxation of mining and staking rewards is a significant policy change for the industry. Senator Lummis and Representative Drew Ferguson (R-GA-3) have proposed recognizing mining and staking rewards as taxable income until they are actually sold or liquidated, instead of the current practice of recognizing these rewards as soon as they are received.

The role of banks

The report recommends that banking regulators, including the Federal Reserve, the Office of the Comptroller of the Currency, and the Federal Deposit Insurance Corporation, develop a set of standard practices and detailed guidance related to custody operations, capital requirements, liquidity management, and risk controls when handling digital assets. The PWG highlights the role of banks and crypto services :

Federal Reserve, OCC, FDIC provide guidance on risk, liquidity, margin, including regulations on reserves and blockchain-based payments.

Encourage public-private partnerships in developing blockchain-based payment infrastructure, with a focus on integrating traditional banking with crypto.

The US wants to both "embrace" blockchain and protect the financial system, creating a safe environment for stablecoins and DeFi, especially through the GENIUS Act requiring safe reserves for stablecoins.

Stablecoins and the USD position

The PWG has become a policy reference for many countries, from how to regulate stablecoins, DeFi to self-custody, with countries like Canada and the UK following suit to create similar regulations. In fact, projects are also reflecting this guidance.

Crypto.com develops flexible DeFi staking, stablecoins, and AML/KYC compliance, in line with PWG recommendations. Decentralized platforms like MakerDAO and Uniswap with token governance, community governance, leading TVL, suggest a legitimate DeFi framework according to PWG.

Crypto.com: Flexible AML/KYC compliance, DeFi staking and stablecoin development, PWG guidelines compliant.

USDC (Circle): Transparent reserves and audit disclosure – typical stablecoin “soft USD weapon”.

MakerDAO, Uniswap: Token governance and decentralization suggest a legitimate DeFi framework according to PWG.

Below is a summary table of the top stablecoins by market capitalization in 2025:

The top stablecoins in 2025 illustrate the central role of stablecoins in the digital financial ecosystem. Coins such as USDT and USDC account for the majority of the market share, reflecting high centralization and global influence, consistent with PWG’s view of stablecoins as “USD soft weapons”.

The data also highlights the need for reserve transparency, AML/KYC compliance, and systemic risk management—core principles that PWG proposes to stabilize finance, support DeFi, and maintain the USD’s position.

Conclusion with an overview

The PWG marks a step forward in the maturation of Crypto policy in the US from fragmented to a comprehensive strategy that is both innovative and compliant.

The impact is spreading globally from the EU, Japan, Singapore learning from the US model, with countries like Brazil and Ghana drafting similar regulations.

Crypto is no longer an experiment but a pillar of 21st-century global finance, with stablecoins forecast to reach $500-750 billion in the next few years.

The PWG is the opening chapter of 21st-century digital asset law, defining how the US will lead the world in crypto, stablecoins, and DeFi. It combines financial freedom, USD stability, and innovation – creating a template for global policy and guiding actual project development. With bills like the CLARITY Act likely to be passed before the end of 2025, the future of crypto in the US is in sharp change, bringing opportunities but also challenges in compliance and competition.

Compiled and analyzed by HCCVenture

Disclaimer: The information presented in this article is the author's personal opinion in the cryptocurrency field. It is not intended to be financial or investment advice. Any investment decision should be based on careful consideration of your personal portfolio and risk tolerance. The views expressed in this article do not represent the official position of the platform. We recommend that readers conduct their own research and consult with a professional before making any investment decisions.

Explore HCCVenture group

HCCVenture © 2023. All rights reserved.

Connect with us

Popular content

Contact to us

E-mail : sp_contact@hccventure.com

Register : https://linktr.ee/holdcoincventure

Disclaimer: The information on this website is for informational purposes only and should not be considered investment advice. We are not responsible for any risks or losses arising from investment decisions based on the content here.

TERMS AND CONDITIONS • CUSTOMER PROTECTION POLICY

ANALYTICAL AND NEWS CONTENT IS COMPILED AND PROVIDED BY EXPERTS IN THE FIELD OF DIGITAL FINANCE AND BLOCKCHAIN BELONGING TO HCCVENTURE ORGANIZATION, INCLUDING OWNERSHIP OF THE CONTENT.

RESPONSIBLE FOR MANAGING ALL CONTENT AND ANALYSIS: HCCVENTURE FOUNDER - TRUONG MINH HUY

Read warnings about scams and phishing emails — REPORT A PROBLEM WITH OUR SITE.