On-Chain Metrics Analysis Week 32: Can DeFi Make a Comeback as Ethereum Booms?

Led by Blue-Chips assets such as UNI, AAVE, MKR, CRV, SNX, COMP, BAL, and SUSHI, the decentralized finance (DeFi) market is experiencing its strongest liquidity growth since 2021.

8/12/202512 min read

Market Summary

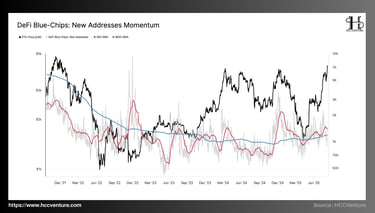

The New Addresses Momentum indicator has been growing steadily and has reached a 12-month high. The number of new addresses is increasing, especially as Layer 2 transaction fees decrease and access to DeFi protocols increases.

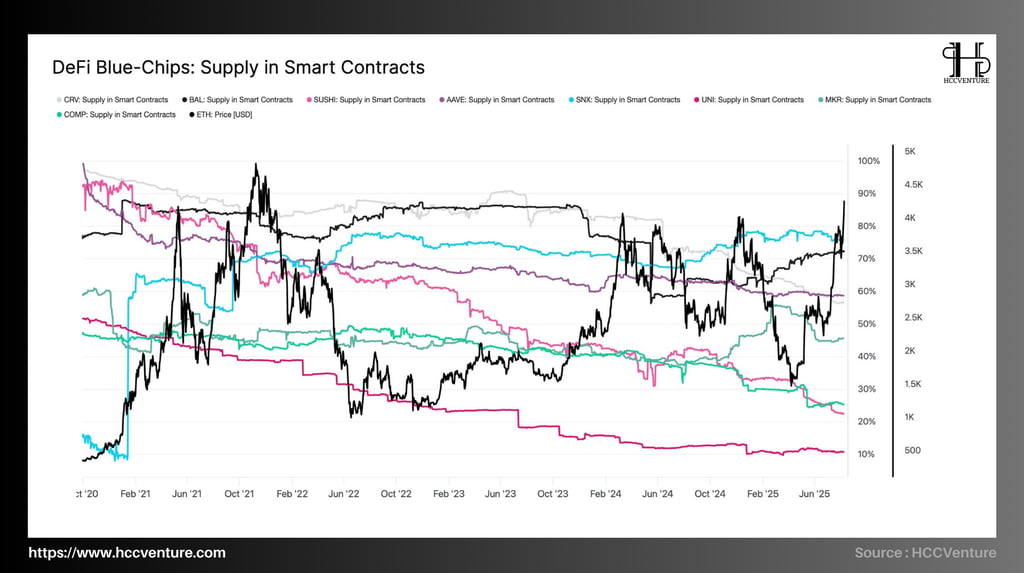

The amount of tokens locked in major protocols is increasing again, according to the Smart Protocol Supply Index. Some tokens, such as AAVE and SNX, still account for more than 70% of the total supply in smart protocols, indicating investor confidence and demand.

Across the board, Momentum transaction counts and transactions per active address have increased, indicating higher transaction volumes and higher transaction frequencies. This is a sign of a more active liquidity market than just short-term participation.

The circulation rate of the Blue-Chips DeFi group reached 0.14, a multi-year high. This shows that 14% of the total token supply is actively circulating, which is the most active period since the beginning of 2021. The free finance market could experience an extended growth cycle in the next six to twelve months with the possibility of setting new liquidity peaks if current indicators are maintained (transfer velocity above 0.12, supply in stable smart contracts.

On-chain metrics analysis

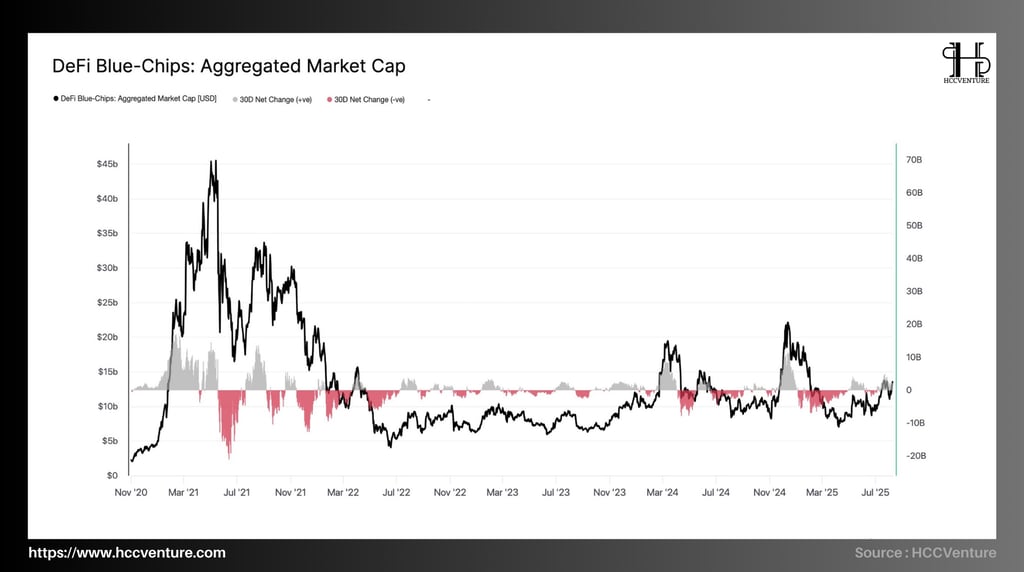

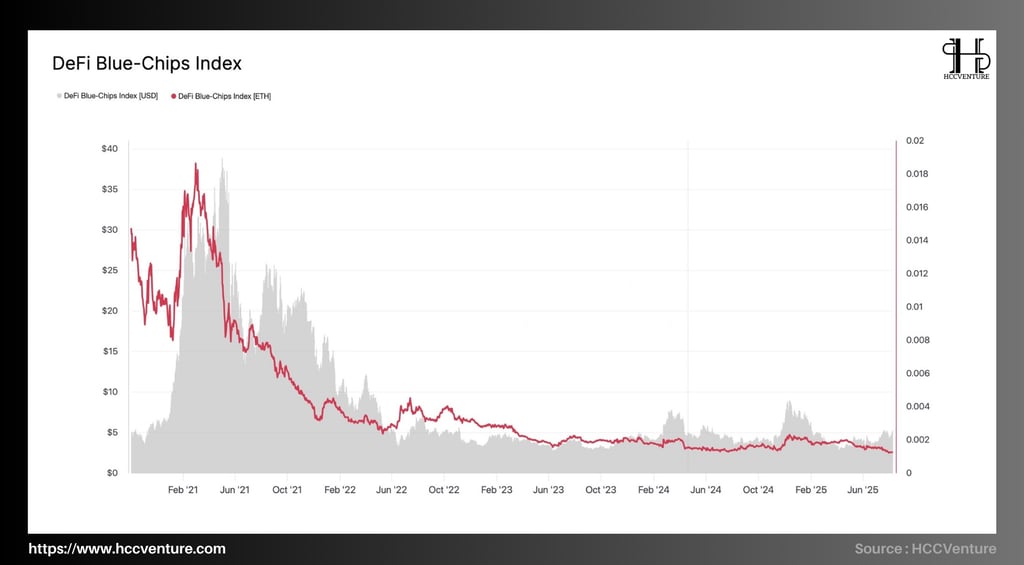

In mid-2021, the market capitalization peaked in the previous cycle, with DeFi Blue-Chips including Uniswap, Aave, and MarketDAO reaching around $45 billion.

The bottom was recorded at $5 billion, down more than 89% from the previous peak, possibly the result of the sell-off pressure caused by Bitcoin's sharp decline, or possibly the shock of Terra and FTX. The index is currently holding double the previous bottom and is between $10 billion and $11 billion, up more than 120 percent from 2022 but still down 75 percent from the 2021 peak.

A series of large negative value clusters appeared in the 2021–2022 period, reflecting capital flight. However, by mid-2023, the negative cash flow periods had decreased and several periods of positive cash flow had appeared, the most prominent of which were positive. Although cash flow is currently in a slight recovery zone, there is still no strong buying pressure.

The decentralized capitalization of Blue-Chips has recovered more than one hundred percent after bottoming at $5 billion in late 2022, but it is still quite far from the old peak in 2021, which is now more than 18 months away. The overall market momentum, mainly coming from large protocols such as MKR, AAVE or UNI, did not cause a significant increase in capitalization from 2024 to 2025. Moreover, some individuals believe that the source of this money can be found in the revenue or transparent tokenized governance of prominent projects in the crypto space.

At present, the decentralized capitalization of Blue-chips can be considered to have completed its long-term accumulation target, and in the coming period, there needs to be momentum to increase. This requires the development momentum of major projects such as UNI, AAVE, and MKR.

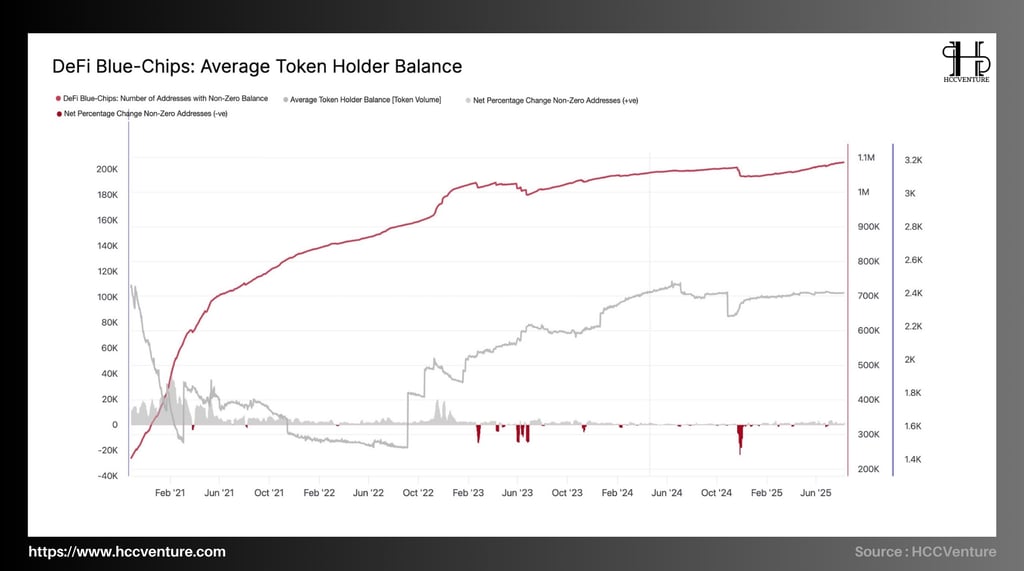

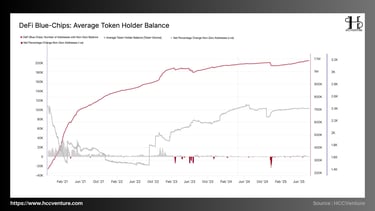

The number of wallet addresses with non-zero DeFi token balances (Non-Zero Addresses) in January 2021 stopped at 200,000 wallet addresses. However, by August 2025, it increased by more than 440% compared to the early stages, the current number of wallets reached more than 1 million wallets with non-$0 balances, the fastest growth rate in Q1/2021 lasted until Q3/2022 before the Terra and FTX events took place.

The average balance (Average Token Holder Balance) in early 2021 stopped at only ~3,000 tokens / wallet, by mid-2022 there was a slight decrease to ~1,600 tokens / wallet, due to the redistribution of supply from large wallets to small investors.

The period from 2023 to 2025 will remain around 1,500 to 1,700 tokens/wallet, with slight fluctuations and more stability, but this token holding level is relatively low and does not meet the minimum conditions needed for strong growth in the next period.

The net change in the number of wallets during the sharp declines appeared sporadically, mainly coinciding with deep market corrections. However, the magnitude of these declines was much smaller than the overall growth momentum, indicating that the selling force was not strong enough to reverse and break the long-term accumulation trend.

A deeper look could see that whales are dispersing assets to a large number of small investors, causing the number of Non-Zero wallet addresses to increase dramatically but the average wallet balance to decrease significantly. Or perhaps this is a factor of dispersion and accumulation in deeper price zones, creating the premise for a prolonged bottom cycle to accumulate more assets in more wallets.

Looking at it more generally, it is not entirely true that this is the decline of DeFi, these are small steps to accumulate large amounts of tokens by large investors. Instead of using wallet clusters to hold large amounts of tokens, they will disperse assets in many wallets with smaller amounts of assets, partly increasing liquidity, partly ensuring security risks.

The total value of the top DeFi projects including Uniswap, Aave, MakerDAO, Curve, Synthetix, Compound, Balancer, SushiSwap peaked at $37.2, coinciding with the DeFi capital explosion and the total industry TVL locked exceeding $110 billion.

From mid-2021 to late 2022, the index plummeted to $5.8, down more than 84% from its peak due to the combined impact of the crypto market crash and liquidity crunch, along with system-wide risk events like Terra Luna.

The index is currently in a narrow range between $1.6 and $4.8 with no significant upside breakout. The current level of around $1.85 represents a 95% drop from the previous ATH. The DeFi Blue-Chips Index has fallen further than ETH, indicating a relatively large weakening of the DeFi capitalization relative to the entire Ethereum ecosystem.

The prolonged capital withdrawal from the Blue-Chips group along with the continuous decline in trading volume, TVL and user activity has lost the growth momentum of the DeFi sector.

The current capital flow in DeFi is being heavily competed by newer sectors such as Liquid Staking, Real Worlds Assets RWA and DeFi2.0, which have overshadowed traditional Blue-Chips and gradually lost their initial dominance.

However, the determination of a prolonged downtrend shows that the DeFi market has not had a sudden correction phase and is continuously maintaining around the historical bottom. The risk of further decline still exists but will not be able to decrease too deeply. The valuation zone is attractive and ideal for long-term accumulation, although it still needs a sudden change from within and external economic factors for the uptrend to rebound strongly.

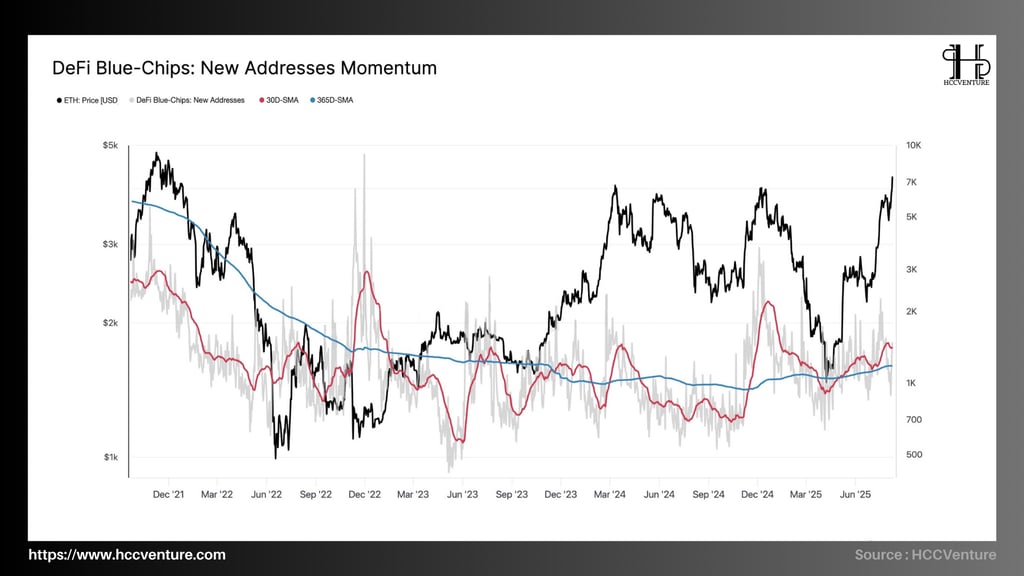

At the end of 2021, the number of new addresses peaked at around 9,200 wallets/day, coinciding with ETH being in the $4,000+ range and strong capital flows into DeFi. However, by the end of 2023, this number had dropped by more than 90% compared to the previous 2 years, stopping at around 700 to 1,000 wallets/day, a factor that measures the withdrawal of investor activity during the same period.

From Q1/2024 to present, the number of new addresses recorded a steady upward trend, currently fluctuating around 1,800 to 2,200 wallets/day, an increase of 130% compared to 2023. Confirming the “bullish crossover” status is the starting signal for a new growth cycle in the number of users.

The number of new addresses with positive signals compared to recent years shows that although the DeFi cycle has declined sharply, it has quickly stabilized. DeFi1.0 may be outdated, but other areas in the DeFi system will continue to develop strongly. As well as DeFi Blue-Chips are gradually regaining their appeal to users, especially in the context of Ethereum just returning to the price range above $4,000.

Although there are signs of recovery, it is still not clear, the average is still 75% lower than 2021, the market still has momentum to grow again, DeFi soon enters a phase of sudden growth.

The clear differentiation between token groups that maintain high lock-up ratios such as CRV, SNX or BAL compared to groups that decline sharply such as UNI, SUSHI or COMP reflects an uneven ecosystem. In which:

CRV has maintained a lockup ratio of more than 85% of its resources in smart contracts since 2021. Currently, CRV still maintains a lockup ratio of more than 90%, showing that most of the tokens are serving DeFi activities such as Curve Pools or Vote-escrow and limiting the amount of tokens circulating on the market.

SNX has a stable token lockup ratio of around 75% over the past 3 years, reflecting Synthetix's long-term staking model

BAL has a retention level of 70% and is mostly tied to the Blancer pools liquidity mechanism.

AAVE is hovering around 60% and is the most stable token with no fluctuations exceeding 5%, reflecting the tokenization used for both governance and staking insurance in the Aave Protocol.

MKR has been trending down slightly from ~45% (2021) to ~40% currently, indicating that some of the supply is being withdrawn from smart contracts, possibly related to the strategy of restructuring the DAO and reducing reliance on on-chain locking.

COMP has dropped sharply from ~40% (2021) to ~28% today, reflecting the trend of capital withdrawal from lending protocol Compound after liquidity reduction and competition from other platforms.

UNI has dropped from over 55% in 2021 to just ~15% now, a historic low, indicating a large amount of tokens have exited smart contracts, likely related to LP incentive reduction and sell-offs from long-term holders.

SUSHI has dropped from ~100% (2020–2021) to just ~10–12% today, reflecting a sharp decline in DeFi activity on SushiSwap and liquidity leaving the platform.

Tokens with high lock-up ratios (CRV, SNX, and BAL) limit selling pressure on the market and demonstrate ecosystem stability and holder commitment. Tokens with decreasing lock-up ratios (UNI, SUSHI, and COMP) clearly reflect the trend of capital withdrawal and reduced platform appeal. This increases circulating supply and may lead to downward price pressure. Although the lock-up ratio is lower than the leading group, the stability of AAVE and MKR shows that the market still believes in these platforms. Data shows that the lock-up ratios of some tokens (UNI, COMP, and SUSHI) have decreased as ETH prices have recovered strongly (2024–2025). This shows that capital is moving to opportunities other than traditional DeFi platforms.

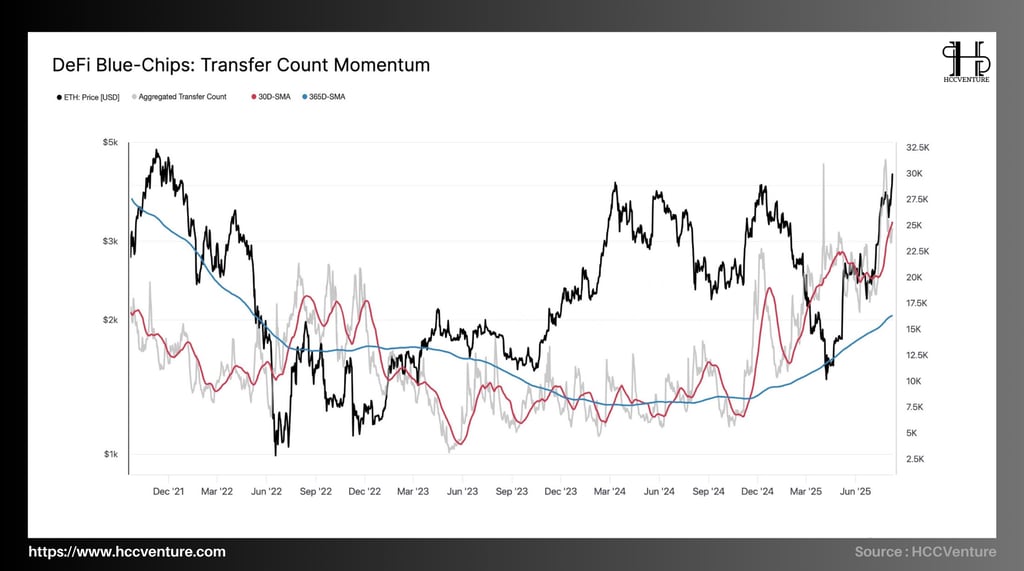

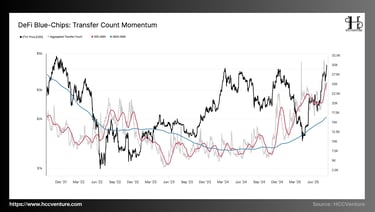

As of August 2025, the aggregate transaction volume of Blue-Chips DeFi tokens reached 30,000 transactions per day—the highest since early 2022—and increased by more than twenty percent from the low of 9,500 transactions per day in Q1 2024.

The 365-day moving average (365D-SMA) has 16,500 trades per day, but the 30-day moving average has 25,000 trades per day. The short-term trading velocity is significantly higher than the long-term average, indicating a clear increase in momentum.

The influx of money into the Ethereum ecosystem and the rise in decentralized exchange (DeFi) activity are closely linked to the strong recovery phase that began in Q2 2025, when ETH prices recovered from around $1,600 to nearly $4,000. Current trading volumes are only about 6% below the historical peak of 32,000 trades/day in early 2021, suggesting that the market is close to regaining its cyclical peak activity.

Breaking above the 30D-SMA and staying above the 365D-SMA for the past 5 months suggests that the on-chain activity growth trend is a sustainable recovery rather than a short-term fluctuation. The increase in market capitalization suggests that derivatives trading, staking, and yield farming in DeFi are being fueled by the ETH price increase.

The trading growth includes most of the major members (UNI, AAVE, CRV, SNX, and BAL), not just one token. This indicates a comprehensive recovery of the segment. The increase in trading volume increases market depth and reduces slippage costs. The sustainable finance market will enter a period of sustainable capitalization and liquidity expansion if the 30D-SMA exceeds the 365D-SMA in the coming months along with the ETH price uptrend.

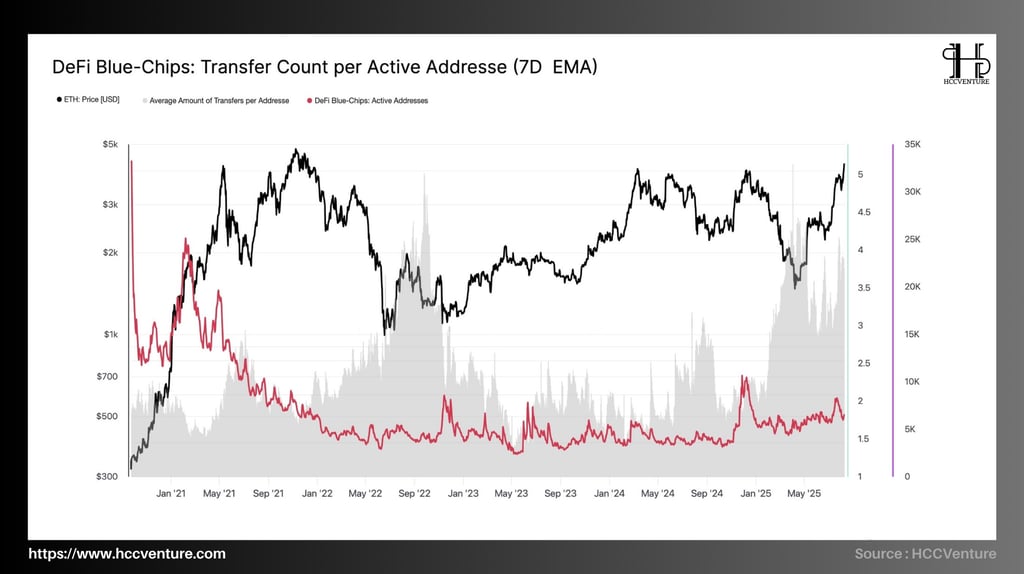

The average number of transactions per active address is ~2 transactions per day in early August 2025, 33% higher than the bottom of ~1.5 transactions per day recorded in Q1 2024.

The metric peaked at 5 transactions per day during the crypto boom of 2021. This coincided with ETH’s peak price of around $4,800. It is still around 60% below that peak, suggesting there is still plenty of room to grow. Active addresses have also been rising sharply; they peaked at 35,000 per day in early 2022. This is nearly three times the low of 12,000 per day in mid-2023.

During each period of strong ETH growth, the chart shows a strong relationship between ETH price and the transfer rate per active address. The increase in this rate is accompanied by an increase in the number of active users and transaction frequency.

The fact that the average number of transactions per address increased in tandem with the total number of active addresses shows that DeFi’s growth is not only based on new user acquisition but also on existing user usage. An average of two transactions per day per address shows a clear increase in capital inflows and activities such as farming, staking, and trading, especially as market liquidity recovers.

Demand for DeFi protocols, especially Layer 2 protocols like Arbitrum and Optimism, has increased as ETH prices have risen from the $1,600 region to $4,000.

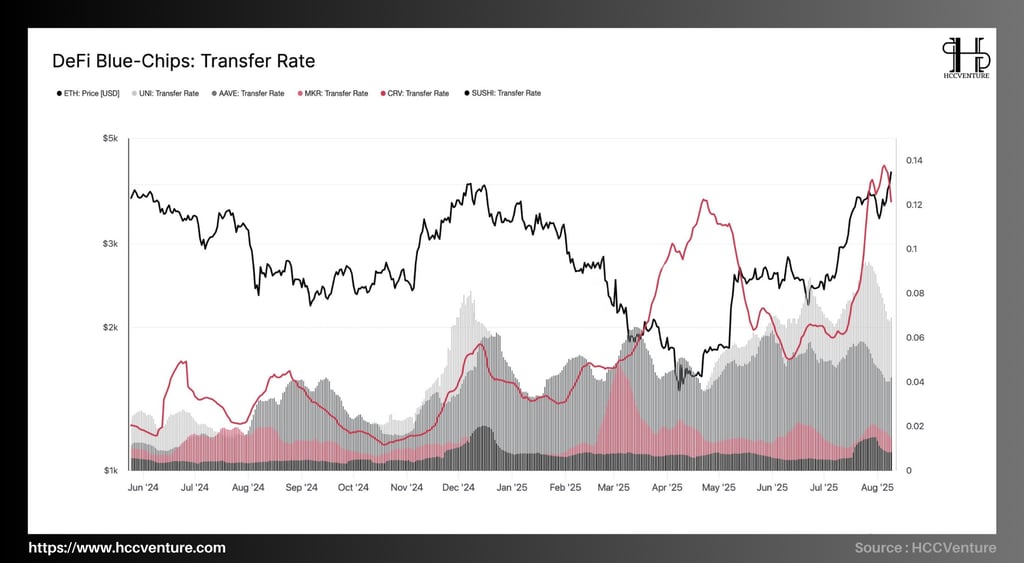

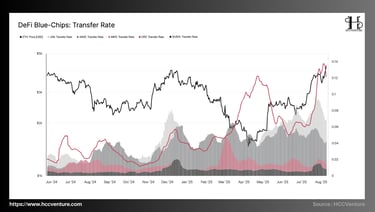

The DeFi Blue Chips group has a transfer rate of 0.14, accounting for about 14% of the total supply being traded during the measurement period. This is the highest level since Q1/2021. The index has nearly tripled since early February 2002, when it was just 0.05. This shows a sharp increase in circulation and trading activity.

The index has undergone two distinct accelerations in the past twelve months:

April to May 2025: Rapid increase from 0.07 to 0.12, while ETH price recovers from $2,200 to $3,200.

June to August 2025: Continues to increase from 0.09 to 0.14, while ETH surpasses $4,000, leading to capital reallocation.

The high transfer rate shows that the volume of capital circulating in the Blue Chips free financial system is vibrant. This reflects a strong demand for trading, farming and transferring assets. This also means that the market is highly liquid, promoting decentralized financial activities. ETH price movements have a clear correlation with the performance of the index. ETH's role as a foundational asset that drives liquidity in the ecosystem is demonstrated by the significant increase in ETH price along with sharp increases in the transfer rate.

The current Transfer Rate is improved by the diversity of Layer 2 and new protocols, which helps maintain a more stable transaction speed and reduce volatility compared to the hot 2021 surge, although it has reached a four-year high. The synchronous increase between Transfer Rate and other metrics, such as Transfer Count Momentum and New Addresses Momentum, shows that this is a continuous growth trend of on-chain activity.

Evaluation and Conclusion

Liquidity circulating in the free financial system has reached its highest level since the 2021 growth cycle, according to remittance data. Rather than relying solely on short-term cash flow shocks, liquidity is being driven by both new capital inflows and actual use, suggesting the market has returned to organic growth.

The high stability of supply in smart contracts (SNX ~80%, AAVE >70%, CRV maintained above 60%) shows that capital is not only flowing in for speculative purposes but also anchored long-term in smart contracts for lending, staking and yield harvesting. This reduces the risk of sudden capital withdrawals and at the same time strengthens the sustainable liquidity system.

The sharp increase in New Addresses Momentum amid the ETH price recovery proves that freelance finance is benefiting from a dual network effect. The increase in the value of the underlying asset (ETH) leads to the expansion of the network of users. History has shown that the most sustainable freelance crypto platform growth cycles always come with ETH-led phases. Therefore, this is especially important.

One notable thing is that all the key metrics—such as new locations, transfers, supply in creative contracts, and transfer rates—are increasing in unison, forming a structure known as “convergence.” This synchronicity is often a strong indicator of a prolonged growth phase in on-chain analysis.

With on-chain indicators at their highest levels in over two years, DeFi Blue-Chips are entering a new growth phase where network growth, liquidity, and market confidence combine to create the foundation for a breakout in scale and market cap in the coming period.

Disclaimer: The information presented in this article is the author's personal opinion on the cryptocurrency field. It is not intended to be financial or investment advice. Any investment decision should be based on careful consideration of your personal portfolio and risk tolerance. The views expressed in the article do not represent the official position of the platform. We recommend that readers conduct their own research and consult with a professional before making any investment decisions.

API & Data : Glassnode

Compiled and analyzed by HCCVenture

Join HCCVenture here: https://linktr.ee/holdcoincventure

Explore HCCVenture group

HCCVenture © 2023. All rights reserved.

Connect with us

Popular content

Contact to us

E-mail : sp_contact@hccventure.com

Register : https://linktr.ee/holdcoincventure

Disclaimer: The information on this website is for informational purposes only and should not be considered investment advice. We are not responsible for any risks or losses arising from investment decisions based on the content here.

TERMS AND CONDITIONS • CUSTOMER PROTECTION POLICY

ANALYTICAL AND NEWS CONTENT IS COMPILED AND PROVIDED BY EXPERTS IN THE FIELD OF DIGITAL FINANCE AND BLOCKCHAIN BELONGING TO HCCVENTURE ORGANIZATION, INCLUDING OWNERSHIP OF THE CONTENT.

RESPONSIBLE FOR MANAGING ALL CONTENT AND ANALYSIS: HCCVENTURE FOUNDER - TRUONG MINH HUY

Read warnings about scams and phishing emails — REPORT A PROBLEM WITH OUR SITE.