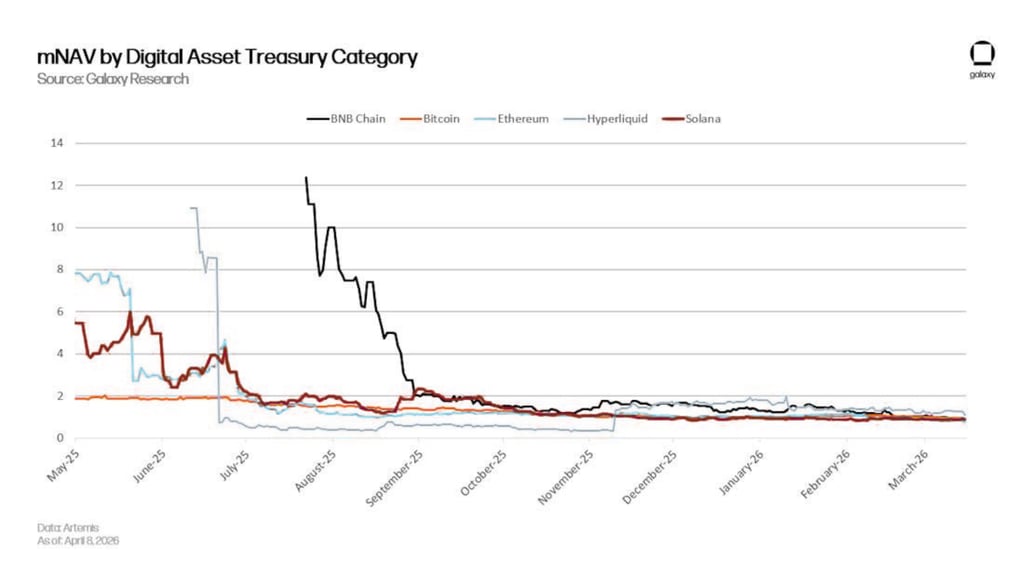

Inflows into DAT cryptocurrency treasury funds have fallen sharply, the biggest drop since 2024

Monthly capital inflows into cryptocurrency treasury management firms fell sharply in May 2026, marking the weakest monthly capital deployment to asset treasury management firms.

6/5/20263 min read

Monthly cash flow decline

The $180 million inflow in May represents a dramatic drop from previous months, when March and April each saw inflows of between $4.2 billion and $4.4 billion, setting a two-month peak just before the collapse in May.

The 95% drop from April to May sets the sharpest monthly decline pattern since the cryptocurrency treasury model gained institutional interest during the late 2024 bull market following favorable signals from regulators and victories for cryptocurrency-linked political candidates in major elections.

The May figure was 93% lower than the five-month average from January to May 2026, suggesting that the April $4.4 billion inflow may represent the last major capital deployment before institutional interest in DAT vehicles collapses completely.

The significant difference between April's $4.4 billion and May's $180 million in just one month suggests a pattern inconsistent with typical capital cyclical volatility or seasonal fluctuations, instead indicating a fundamental revaluation of the DAT asset class, where institutional investors are withdrawing from confidence and redirecting capital allocation to alternative bitcoin exposure mechanisms.

Bitcoin-linked treasury management firms dominated inflows in May with $177 million, leaving only $3 million allocated to alternative blockchain networks including ZCash, Story Protocol, and Sui, while Litecoin recorded a monthly outflow of $1.89 million, indicating a net institutional divestment from non-bitcoin treasury management positions.

The concentration of remaining capital flows entirely in bitcoin treasury management companies, while Ethereum and Proof-of-Stake treasury management companies have seen virtually no additional institutional investment, suggests that investors are maintaining limited exposure to treasuries, confining positions to bitcoin holdings they trust the most, rather than diversifying across multiple digital assets.

ETF competition and valuation pressure

Industry analysts believe the collapse of DAT was primarily due to the emergence of cryptocurrency ETF products, which offer institutional investors a simpler alternative capital deployment mechanism, eliminating the need for specialized treasury management firms as intermediaries.

Arthur Firstov of the financial services firm Mercuryo outlined the core competitive dynamics explaining the capital turnover of institutions, describing ETFs as low-cost, high-liquidity mechanisms for institutions to directly access cryptocurrencies without having to accept the low liquidity or capital structure complexities inherent in publicly listed treasury management companies.

The advantages of ETFs focus on operational simplicity, where institutions deploy capital into standard investment vehicles managed according to established fund protocols, eliminating the need to assess the management quality of each treasury firm, its capital allocation capacity, or its corporate governance structure, which would otherwise differentiate the performance of the treasury firm.

The launch of spot Bitcoin ETFs in 2024, and subsequent expansion to include Ethereum and alternative asset classes in 2025, created competitive products requiring minimal analytical effort from investors while delivering superior after-fee returns compared to treasury management companies that charge operating fees through their corporate structure and balance sheet maintenance costs.

Limitations on revenue from Proof-of-Stake staking.

Industry analysts argue that holding Proof-of-Stake cryptocurrencies allows for the generation of staking revenue, theoretically justifying the valuation of asset management companies and operating costs, with companies holding Ethereum, Cardano, or other PoS assets potentially generating annual staking yields of three to five percent, supplementing operating cash flow.

However, Firstov argues that staking revenue is insufficient to address the fundamental challenges of the business, preventing asset management companies from achieving a sustainable competitive position against ETF alternatives.

This limitation centers on fundamental mathematics, where annual staking yields of three to five percent cannot offset management costs, operational inefficiencies, management salaries, investor relations expenses, and the capital allocation dilution characteristic of many asset management firms. Companies maintaining high fixed operating costs require cryptocurrency price appreciation far exceeding staking yields just to keep the business running, creating a situation where even successful asset management firms face constant capital depletion without superior asset price performance.

Assessment and Conclusion

The collapse of the DAT sector raises important questions about the sustainability of the corporate structure as the primary mechanism for organizations to access cryptocurrencies during the maturation phase of the cryptocurrency market.

This model suggests that institutional capital tends to gravitate toward the simplest, lowest-cost, and least-barrier mechanisms for accessing cryptocurrencies once product diversification is sufficient to allow mainstream investors to access them through traditional channels.

Institutional preference for ETFs over corporate governance structures contradicts previous assumptions that professional management and proactive capital deployment strategies would justify high management costs and corporate valuations.

Instead, market judgment revealed that most institutional investors value simplicity and liquidity more than theoretical value management, readily accepting passive index-tracking investing at significantly lower costs than required by corporate structure.

Disclaimer: The information presented in this article is the author's personal opinion in the field of cryptocurrencies. This is not financial or investment advice at all. Every investment decision should be based on careful consideration of your personal portfolio and risk tolerance. The opinion in the article does not represent the official position of the platform. We recommend that readers do their own research and consult experts before making any investment decisions.

Synthesized and analyzed by HCCVenture

Follow HCCVenture organization here: https://link3.to/holdcoincventure

Explore HCCVenture group

HCCVenture © 2023. All rights reserved.

Connect with us

Popular content

Contact to us

E-mail : sp_contact@hccventure.com

Register : https://linktr.ee/holdcoincventure

Disclaimer: The information on this website is for informational purposes only and should not be considered investment advice. We are not responsible for any risks or losses arising from investment decisions based on the content here.

TERMS AND CONDITIONS • CUSTOMER PROTECTION POLICY

ANALYTICAL AND NEWS CONTENT IS COMPILED AND PROVIDED BY EXPERTS IN THE FIELD OF DIGITAL FINANCE AND BLOCKCHAIN BELONGING TO HCCVENTURE ORGANIZATION, INCLUDING OWNERSHIP OF THE CONTENT.

RESPONSIBLE FOR MANAGING ALL CONTENT AND ANALYSIS: HCCVENTURE FOUNDER - TRUONG MINH HUY

Read warnings about scams and phishing emails — REPORT A PROBLEM WITH OUR SITE.