DTCC processes directly tokenized stock, ETF, and Treasury bond transactions

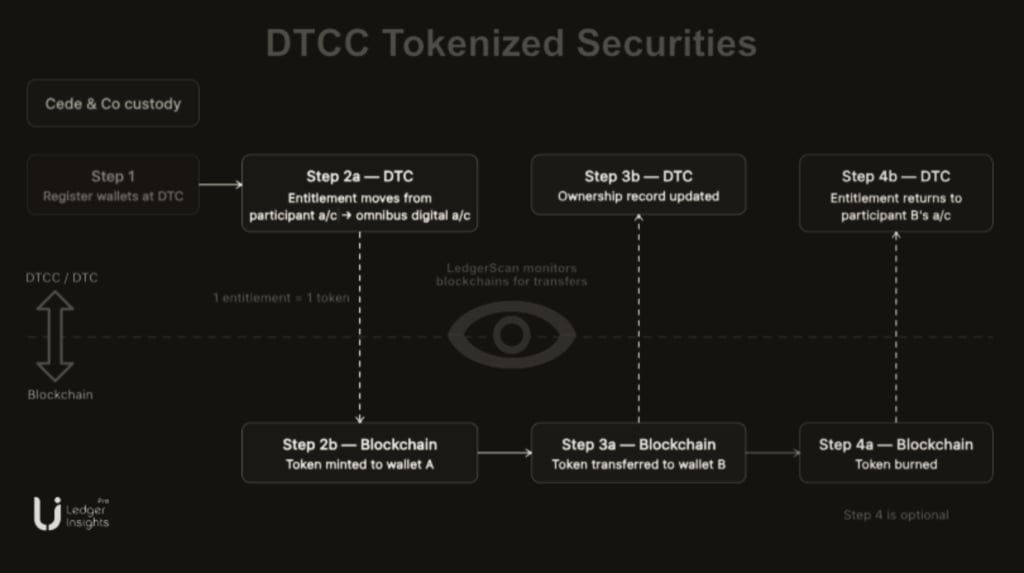

The Depository and Clearing Corporation (DTC) has executed its first actual production transactions using tokenized versions of assets held by DTC, preserving equivalent legal ownership.

7/16/20264 min read

Digital copy of assets held by DTC

DTCC's tokenized asset service does not replace the underlying securities, does not transfer legal ownership onto the blockchain, or create synthetic copies. The model is structurally different and designed to be compatible with existing legal frameworks: DTCC creates tokenized copies, internally referred to as digital copies, of assets that remain within its existing custody infrastructure, with the tokens carrying the same legal ownership as the underlying securities they represent. When JPMorgan tokenized QQQ, Invesco's ETF remained exactly as it was before, with no structural changes to the fund itself. JPMorgan received blockchain-based tokens representing the amount of QQQ they held, which could be transferred, collateralized, and settled on the blockchain platform, while the underlying shares remained held at DTCC.

Preserving traditional ownership rights within the legal architecture is a key feature that makes institutional participation possible. A tokenized version of QQQ that questioned whether token holders possessed the same redemption, voting, or legal claim rights as traditional shareholders would face insurmountable compliance hurdles across its entire institutional client base. By clearly upholding those rights and operating within DTCC's existing legal framework, DTC received a letter of no objection from the SEC, establishing the legal basis for the asset tokenization service. This pilot program eliminates regulatory uncertainty that has prevented previous asset tokenization efforts from progressing through the feasibility study phase.

The CME margin call demonstrates an effective use case.

The most significant demonstration of the day wasn't the tokenization process itself, but what JPMorgan did with the tokenized QQQ after its creation. The bank used these tokenized shares as collateral to meet the margin requirements of its counterparty at CME Group, the world's largest derivatives exchange by open interest, completing the collateral transfer process without closing positions, liquidating, or removing them from investors' portfolios.

In a traditional market structure, fulfilling a margin call on a derivative position typically requires the registrant to sell liquid assets to generate cash, transfer the cash to a clearinghouse, and replenish the cash position through other means—a chain of transaction costs, settlement delays, and opportunity costs due to temporarily closing the collateral position. The QQQ registration, tokenized directly into CME, completely eliminates this intermediate cash conversion: derivative risk is maintained, the equity position is maintained as a token as the pledged collateral, and the margin request is fulfilled through a direct blockchain transfer between DTCC's settlement infrastructure and CME's margin management system.

The capital efficiency benefits are real and measurable for institutions managing large derivative portfolios alongside significant equity portfolios. If tokenized equities could be directly accepted as collateral across the entire clearing infrastructure handling the majority of U.S. derivative margin obligations, then reducing the total amount of cash reserves that institutional investors must maintain—currently estimated at hundreds of billions of dollars sitting idle as potential margin—would represent a significant improvement in returns on investment for institutions.

The potential market size is $114 trillion.

DTCC's revelation earlier in 2026 that it was partnering with over 50 global financial institutions on asset tokenization, targeting a total asset value of approximately $114 trillion – the total securities DTCC holds – has shaped the potential scope of the service launched in October to far exceed all previous tokenization initiatives combined. The total on-chain real-world asset (RWA) market recently surpassed the $20 billion mark, a milestone celebrated by the tokenization industry as evidence of increasing institutional adoption. DTCC's $114 trillion custody mark sets a different scale for what crypto for institutions can ultimately represent: the current RWA market, worth $20 billion, impressive as a growth rate indicator, represents less than 0.02% of the total securities that DTCC's October offering will target for crypto.

The limitations on the speed of converting that asset class to tokenized form after the July 15th demonstration are not a technological issue, but rather the speed of adoption by institutions, regulatory clarity regarding the handling of tokenized securities in the practical use cases that institutions need (collateral, repurchase transactions, clearing), and the economic efficiency of the business model that makes tokenization superior to existing workflows for each participating company.

Assessment and Conclusion

The DTCC live launch event on July 15th marked a transition point that capital market observers had identified as the moment when asset tokenization ceased to be an experiment and became infrastructure, with real money, real margin requirements, and real collateral obligations being met through tokenized securities within the system of the world's most important clearing and settlement organization. Every institutional investor managing derivative risk through CME, holding securities in the DTC custody, and monitoring the performance of their collateral pool had specific operational reasons to participate in the service launch in October.

The transition from the July 15th pilot program to production service in October will test whether the operational success of the pilot program translates into large-scale voluntary adoption by institutions, and whether the benefits of capital efficiency from the mobility of tokenized collateral outweigh the costs of integrating blockchain clearing infrastructure into existing portfolio and risk management systems. Companies that joined in July have already completed much of that integration work. Companies that did not join will evaluate the October service based on the proven evidence that pilot participants have accumulated through successful execution of real transactions.

Disclaimer: The information presented in this article is the author's personal opinion in the field of cryptocurrencies. This is not financial or investment advice at all. Every investment decision should be based on careful consideration of your personal portfolio and risk tolerance. The opinion in the article does not represent the official position of the platform. We recommend that readers do their own research and consult experts before making any investment decisions.

Synthesized and analyzed by HCCVenture

Follow HCCVenture organization here: https://link3.to/holdcoincventure

Explore HCCVenture group

HCCVenture © 2023. All rights reserved.

Connect with us

Popular content

Contact to us

E-mail : sp_contact@hccventure.com

Register : https://linktr.ee/holdcoincventure

Disclaimer: The information on this website is for informational purposes only and should not be considered investment advice. We are not responsible for any risks or losses arising from investment decisions based on the content here.

TERMS AND CONDITIONS • CUSTOMER PROTECTION POLICY

ANALYTICAL AND NEWS CONTENT IS COMPILED AND PROVIDED BY EXPERTS IN THE FIELD OF DIGITAL FINANCE AND BLOCKCHAIN BELONGING TO HCCVENTURE ORGANIZATION, INCLUDING OWNERSHIP OF THE CONTENT.

RESPONSIBLE FOR MANAGING ALL CONTENT AND ANALYSIS: HCCVENTURE FOUNDER - TRUONG MINH HUY

Read warnings about scams and phishing emails — REPORT A PROBLEM WITH OUR SITE.