Crypto Asset Management Companies - DATCO

DATCOs, which are businesses pursuing digital asset management, initially mostly Bitcoin, Ethereum and now also including Solana, XRP,... were formed right after the US digital asset reserve strategy was issued.

INSIGHTS

9/10/202512 min read

Overview of the DATCO model

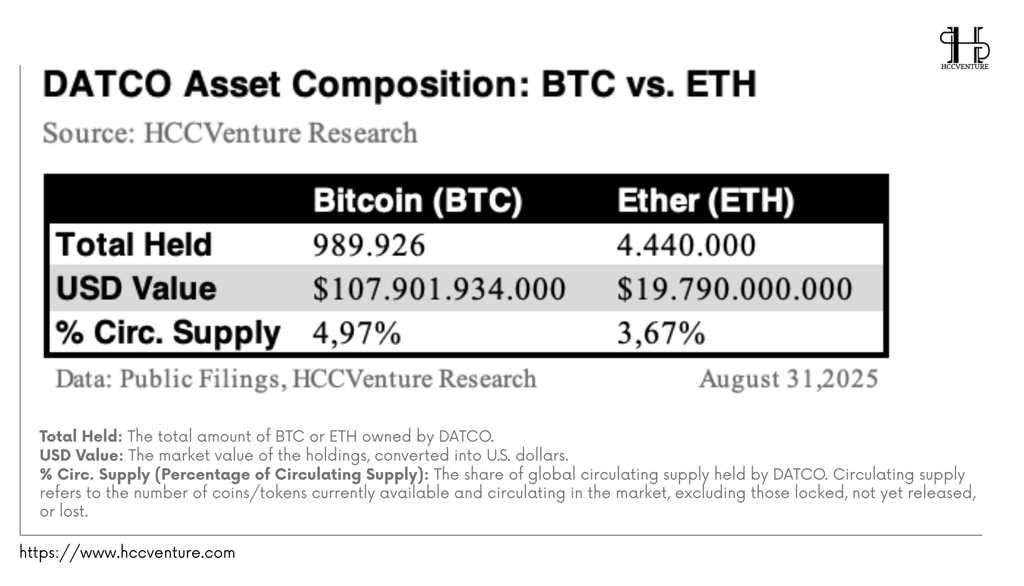

DATCO companies currently hold over $126 billion in crypto assets (at current market value), led by publicly listed companies Strategy MSTR, Metaplanet 3350.T, and SharpLink Gaming SBET. Currently, the key holdings are over 90% Bitcoin and Ethereum.

Bitcoin fund managers dominate the category with over $107 billion in Bitcoin holdings, while recent entrants to the DATCO group have been focused on Ethereum, bringing the total ETH holdings to nearly $20 billion. These firms hold 989,926 BTC and 4,440,000 ETH, representing 4.97% of the BTC circulating supply and 3.67% of the ETH circulating supply.

Strategy alone has over $22 billion in unrealized gains on its Bitcoin holdings worth ~$69 billion at current market prices. Smaller companies also show a low BTC cost base and significant growth potential. Some of the companies participating in this DATCO model have expanded and diversified their portfolios and reserve strategies beyond BTC and ETH. There are currently many applications for licenses to manage other assets such as SOL, BNB, HYPE, XRP, etc.

In addition to digital asset management, companies within the DATCO group can leverage expansion into strategies such as Staking and other DeFi yields, providing additional passive and potentially non-dilutive sources of return for management capital other than BTC assets.

DATCOs differ from traditional ETFs in that they can raise capital to deploy strategically and benefit from positive investment flows. However, this model is susceptible to premium collapse, regulatory changes, and capital market disruptions. DATCOs are most dependent on PIPEs or excessive leverage, which can lead to significant downside in unfavorable market conditions.

Currently, DATCO companies are creating a positive feedback loop for digital asset value, but this always creates potential risks such as simultaneous profit taking that can easily lead to a depletion of demand and a significant market correction. However, if Strategy is not counted, the other companies under DATCO are relatively small, holding only 1/3 of Strategy’s value, and only about 0.83% of the total cryptocurrency market capitalization (the most recent figure is 3.8 trillion USD).

Academic Definitions of DATCO

Digital Asset Treasury Company (DATCO): are public companies with a core capital mobilization strategy to store and manage crypto assets related to Bitcoin, Ethereum and some other crypto assets. DATCO actively pursues a long-term accumulation strategy, continuously increasing the amount of reserves in their treasury. Investors consider investing in these companies as a leveraged tool, with a high beta coefficient to represent the level of risk of the assets they are holding.

Premium to equity over NAV : is a measure of how much equity trades at a premium to its net asset value per share (NAV). In the report, we present a simplified formula :

Insurance premium = ((Stock price / (NAV/share)) -1) *100 (%)

This figure best captures how rich or cheap the public stock market is in valuing a company’s digital assets, but it differs from the cost of capital (including debt or diluted share count) that is often used to describe one of these companies.

mNAV - Net Asset Value Multiple and represents the same concept as premium, but as a multiple rather than a percentage. For example, a stock trading at 1.85x mNAV has a premium of 85%.

ATM - At-the-Market Offerings allow companies to issue shares in batches at current prices. When a company trades at a premium to its NAV, each dollar raised through an ATM buys more cryptocurrency per share than is diluted. ATMs are often the preferred means of raising capital for DATCOs because they allow them to scale their investment strategy and scale easily, avoiding high discounts or large issuance events that require more capital.

PIPE - Private Investment in Public Equity is a negotiated form of capital raising in which large investors purchase newly issued shares, often illiquid or with a low float, at an agreed upon price. While PIPEs allow for rapid capital raising, they often come with significant dilution and short-term risk.

Bitcoin Yield is a metric that tracks the growth performance of BTC per diluted share of a Bitcoin fund management company over time, reflecting the efficiency of the company's capital utilization, i.e. the ability to raise capital and convert capital into BTC without excessive dilution of shareholders. In simple terms, when Bitcoin Yield is high, the equity premium is higher.

Digital Asset Management

DATCO companies currently hold 989,926 BTC with an estimated market value of ~$108 billion , representing 4.97% of the total circulating supply , and 4,440,000 ETH with a value of ~$19.8 billion , representing 3.67% of the circulating supply .

Compared to July 2025, DATCOs including (Strategy, Metaplanet, SharpLink, BitMine, GameSquare, etc.) only held about 791,000 BTC and 1.3 million ETH, it can be seen that the number of BTC held increased rapidly by ~25% in just 4 weeks, attracting a large amount of cash flow from DATCOs. In other developments, the ETH treasury increased more than 3 times and 4 times in value, showing a clear strategic shift in investment structure.

However, Bitcoin still holds the role of a core treasury asset , acting as “digital gold” on the balance sheets of DATCOs. Among them, Strategy (MSTR) continues to be the leader, holding over 600,000 BTC , equivalent to >70% of the total BTC held by public companies. This reinforces MSTR’s position as the “representative” of organizations in the Bitcoin market.

ETH treasury from DATCOs has a big jump bringing the total treasury from 1.3 million ETH tokens to 4.44 million ETH tokens reflecting strong interest in the yield and staking story. DATCOs businesses are moving closer to the DeFi, NFT and Layer2 ecosystem.

The main factors driving this development are:

ASB 2023: New accounting standards allow accounting for digital assets at fair value, reducing “mark-to-market” risks and opening the door for more listed companies to participate.

Spot BTC ETF (2024): Validates Bitcoin's legitimacy, bringing liquidity and institutionalization to the market.

Geopolitical Instability & Weakening Fiat Currencies: Rising Demand for Safe Havens, BTC Outshines Gold Due to Transparency and Global Liquidity.

The rise of altcoin treasury (2025): New companies looking to diversify, prioritizing assets with cash flow from staking , especially with ETH and L1/L2s.

A new model has been established and transformed from fund management combined with yield enhancement pioneered by SharpLink, BitMine and GameSquare, transforming ETH from a storage asset to a yield-generating asset, completely different from the nature of traditional storage assets. ETH treasury is increasingly becoming a parallel story with BTC, implying that: Bitcoin is a "Precious Reserve Metal" and ETH is a "yielding asset" in the new investment management strategy.

For the next trend, BTC will continue to be the strategic foundation in treasuries. ETH and staking assets will explode thanks to companies looking for superior yields, expanding from “store of value” to “yield-generating treasury”. This combination turns DATCO into a new strategic middle layer between TradFi and Crypto , where BTC acts as a “pedestal” and ETH as a “growth engine”.

Who is leading in DATCOs?

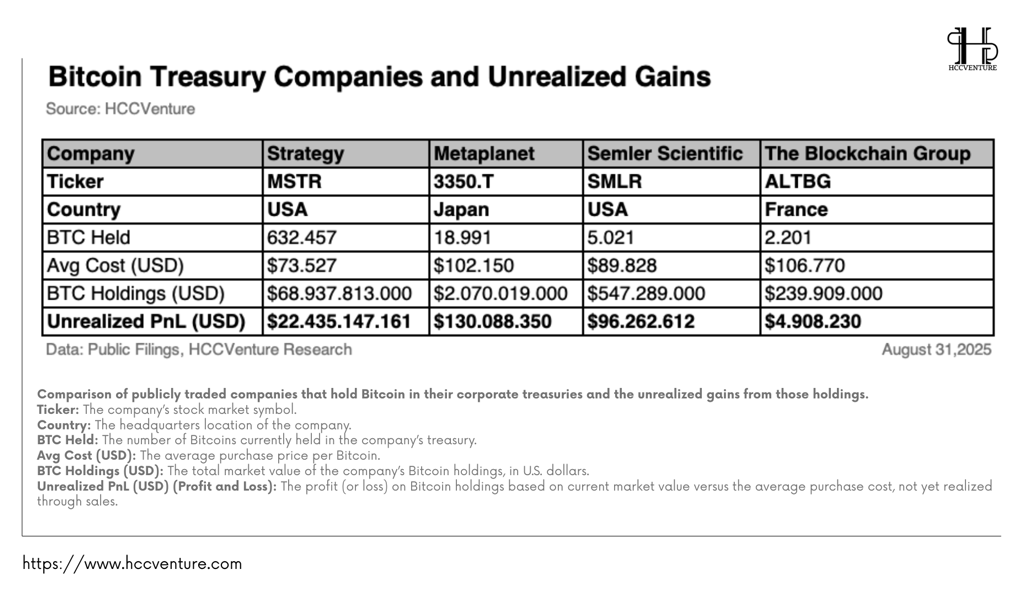

With 632,457 BTC in holdings, Strategy (MSTR) is now the largest listed company in terms of Bitcoin, accounting for the majority of all BTC in public company treasuries. MSTR’s average cost of capital is $73,527/BTC , significantly lower than its assumed market price of $118,000/BTC . This gives MSTR an unrealized profit of $22.4 billion – the highest in the industry.

The strategy of continuous buying despite market volatility has turned MSTR into a “proxy” for Bitcoin in the US stock market , attracting both institutional and individual investors who want indirect exposure to BTC.

Coming in at number 2 is “Japan’s MicroStrategy” Metaplanet (3350.T), whose current BTC treasury holdings are 18,991 BTC with an average cost of capital higher than MSTR by about $102,150/BTC, but still generating unrealized profits of more than $130 million, a typical example of the global trend of Bitcoin treasury strategies , no longer limited to US companies.

Unrealized gains are a testament to Bitcoin being a good capital growth asset . Companies not only preserve their value but also record significant increases in value on their books. However, unlike operating profits, this is still entirely dependent on market prices and can be reversed quickly if BTC falls sharply.

In addition to BTC, companies like SharpLink Gaming (SBET), Bit Digital (BTBT), and Tron Inc. (TRON) are now shifting to accumulating ETH, TRX, or yield-yielding tokens through staking. Compared to Bitcoin, which only provides capital gains, assets like ETH can generate passive cash flow from staking , adding a yield element to treasury strategies. The rise of altcoin treasury signals a new phase where companies are not only treating crypto as “digital gold” but also as yield-generating financial assets , especially ETH and staking tokens.

Portfolio expansion trend

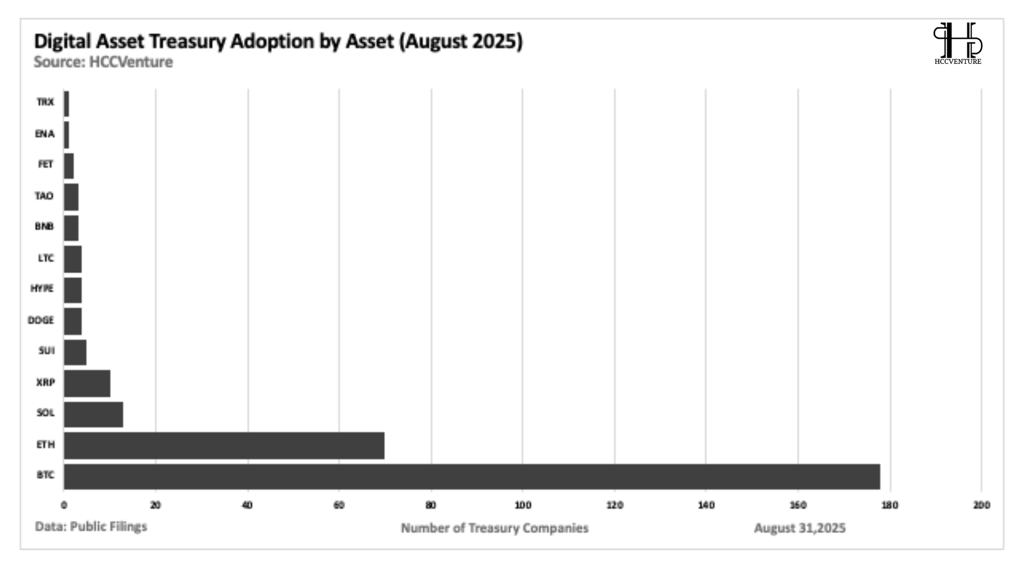

Data shows that Bitcoin BTC continues to be the absolute dominant asset in the portfolios of digital treasury companies. Nearly 200 companies have publicly held BTC on their balance sheets, far exceeding any other asset. Thanks to its high status and liquidity, increasingly transparent regulatory framework, and its role as “digital gold” .

Data shows that Bitcoin BTC continues to be the absolute dominant asset in the portfolios of digital treasury companies. Nearly 200 companies have publicly held BTC on their balance sheets, far exceeding any other asset. Thanks to its high status and liquidity, increasingly transparent regulatory framework, and its role as “digital gold” .

After BTC, Ethereum ETH is the second most popular asset, with over 70 DATCO companies accumulating in corporate treasuries. This is because staking creates passive cash flow, making ETH more attractive in the context of moving closer to DeFi. The adoption of yield-enhanced treasury strategies by companies like SharpLink, BitMine, and GameSquare has pushed ETH to become the second pillar in this DAT structure. In addition to the reserve asset, ETH also represents the DeFi, NFT, and Layer 2 ecosystems , providing a wider level of “exposure” for companies looking for diversification.

Solana has recently been chosen by many ATCOs due to its high performance and rapidly growing DeFi/NFT ecosystem. The increased interest reflects a trend of looking for fast, low-cost technology . In addition, BNB is considered an infrastructure asset, attractive to companies that want to get exposure to the massive Web3 ecosystem that Binance is leading.

The diversity is further expanded as more companies join DATCO with assets such as HYPE, SUI, DOGE, LTC, FET, TAO, ENA, TRX. Holding these assets is not only based on financial performance, but also strategic experimentation or narrative-driven .

Global Macro Perspective

DATCOs (Digital Asset Treasury Companies) have become a global phenomenon. However, their distribution is uneven, reflecting differences in regulatory frameworks, financial cultures, digital asset adoption, and the presence of pioneering companies .

The US is currently the largest hub for DATCO, led by Strategy (MSTR) and several smaller listed companies such as Semler Scientific. The US role is reinforced by FASB 2023 (accounting standards that allow for fair value accounting) and a Bitcoin spot ETF in 2024 , bringing crypto to mainstream assets.

Japan follows suit with Metaplant's representative face, its huge BTC holdings putting Japan in the highly concentrated group. Putting Japan in 2nd place with its globally successful DATCO strategy.

Several European countries have a significant number of listed DATCOs, mainly focusing on fintech and blockchain-native companies. Crypto-friendly policies in Switzerland and the UK have encouraged many companies to add Bitcoin and Ethereum to their coffers.

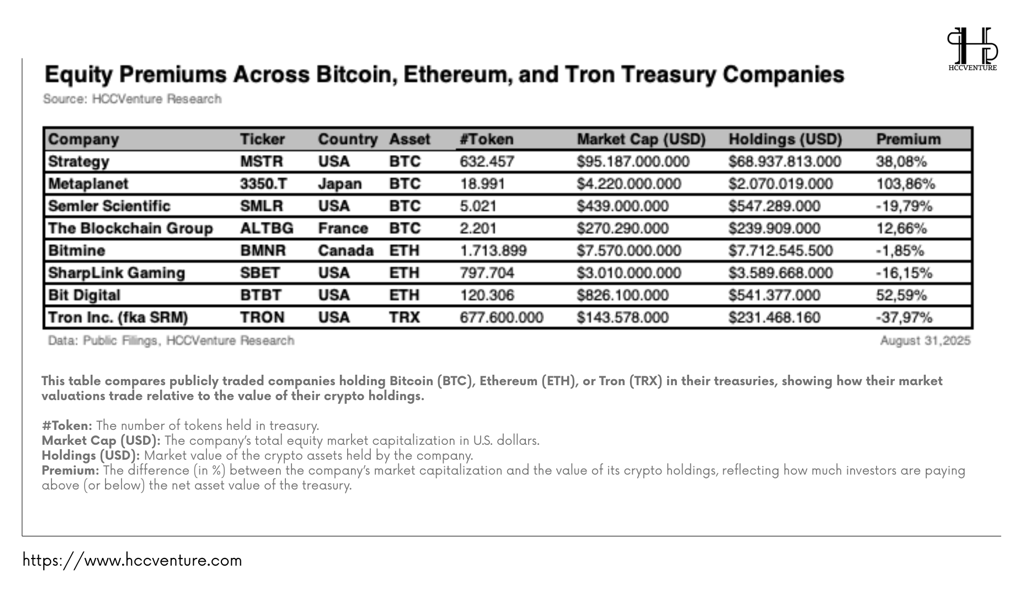

Valuation dispersion and equity premiums

The data shows that although DATCO companies all pursue a digital asset accumulation strategy, the stock market applies very different equity premiums to each company's net asset value (NAV).

Despite being the leading Bitcoin treasury, MSTR only trades at a 38% premium, a modest amount given the massive 632,457 BTC in the treasury. Reflecting that investors see MSTR as a “mature” proxy for Bitcoin , with relatively little speculative interest.

In contrast, Metaplanet is trading at a 103.86% premium , double the value of the digital asset. This is largely due to Metaplanet’s “growth at all costs” strategy, which has led the market to price in a narrative of capital growth and a BTC scarcity in Asia .

In addition, other companies are currently holding premiums of 12% to 20%, typically Semler Scientific (SMLR) trading at a discount of -19.79% , meaning the market is not ready to pay a premium for the small-scale DATCO model. The Blockchain Group (France) has a premium of 12.66% , reflecting the modest scale but also showing that Europe is pricing DATCOs more cautiously.

For Ethereum, the dispersion is more pronounced in groups such as: BitMine (BMNR, Canada) is priced close to NAV ( -1.85% ), indicating that the market is still skeptical about the long-term effectiveness of the ETH holding strategy. SharpLink Gaming (SBET, US) is discounted -16.15% , reflecting that investors are valuing the business based more on sports betting data than ETH treasury. Bit Digital (BTBT, US) has a premium of 52.59% , indicating that ETH is being valued by the market for its potential yield from staking and ecosystem expansion . This is a sign that investors are willing to pay more for ETH treasury when there is an expectation of active returns.

There is however a rather unique case like Tron Inc (TRON) with 677.6 million TRX held, with the majority staked (365 million TRX). However, the company trades at a discount of -37.97% , contrary to the narrative data in the previous report (which suggested that TRON was trading at a premium). Fragmentation in altcoin valuations, brand treasury and narrative can push premiums up in the short term, but volatility and lack of liquidity drag valuations down.

Premiums in DATCO not only reflect the value of digital assets but also serve as an indicator of market sentiment . BTC DATCO is suitable for investors seeking stability; ETH DATCO attracts investors pursuing yield and capital growth ; while altcoin DATCO is highly speculative and depends on the narrative . High premiums (such as Metaplanet, BTBT) can bring superior returns if the narrative continues to be maintained, but also pose the risk of a sharp correction if expectations do not materialize.

Capital Strategy from DATCOs

At the heart of the Digital Asset Treasury Company (DATCO) model is a reflexive loop:

(1) Issue shares at a premium (market price higher than NAV).

(2) Use mobilized capital to buy crypto.

(3) NAV per share increases , further reinforcing the premium.

This self-reinforcing loop—sometimes called “accretive dilution” —makes DATCOs both powerful crypto accumulation machines and structurally vulnerable to changing market conditions. Metaplanet , for example, has been nimble in its At-the-Market (ATM) program to raise capital when premiums are high, rapidly expanding its BTC holdings.

They have used one of two ways to raise capital:

ATMs (At-the-Market Offerings)

Companies issue new shares in small batches at market prices, raising capital when sentiment is positive.

Avoid deep discounts like block releases.

Flexible timing, can be suspended when the market is bad.

When the stock is trading at a premium, each USD raised buys more crypto than it dilutes → creating a loop of increasing NAV .

PIPEs (Private Investments in Public Equity)

Transactions negotiated with institutional investors, often priced at a fixed discount to the market.

Advantages: Fast, large volume, suitable for small or new DATCO.

Typical examples: Nakamoto raised $51.5 million via PIPE to buy BTC (June 2025). BitMine and SharpLink Gaming also used PIPE to increase ETH treasury.

Rapidly increase the number of shares, causing supply pressure in the future when the lockup shares are released.

The DATCO model relies entirely on a maintenance premium relative to NAV . If the premium shrinks or even turns into a discount, the loop will break. Some DATCOs have begun trading close to or below NAV. In this case, they can choose to buy back shares to exploit the difference (arbitrage). BitMine has asked the board of directors for permission to buy back up to $1 billion in shares.

If buybacks and unwinds become widespread, reverse selling pressure could occur, wiping out accumulated cash flows and negatively impacting crypto prices. History has it that there was the investment trust mania of the 1920s . As premiums collapsed, the ability to raise capital ceased, leading to a chain of failures that contributed to the 1929 crash.

Evaluation and Conclusion

DATCO continues to expand, exploiting a variety of tokens (especially PoS to take advantage of yield), hybridizing with a real cash flow generating business model. The reflexive relationship between the stock market (DATCO shares) and crypto prices makes BTC increasingly influenced by risk-on/risk-off capital flows , instead of maintaining a non-correlated characteristic. Large companies (like Strategy) can buy back small DATCOs that are trading below NAV, turning premiums into treasury expansion tools.

DATCO has evolved from a capitalization experiment into a structured cash flow engine for the crypto market . When digital asset prices are rising, premiums are high, and capital markets are liquid, DATCO becomes the biggest driver of Bitcoin and Ethereum accumulation. But if those three variables reverse, the cycle could become a drag on both crypto and capital markets, creating systemic risk for both crypto and capital markets. DATCO is the bridge between crypto financialization and crypto finance : transparent, compliant, but also fraught with reflexive risk.

Disclaimer: The information presented in this article is the author's personal opinion on the cryptocurrency field. It is not intended to be financial or investment advice. Any investment decision should be based on careful consideration of your personal portfolio and risk tolerance. The views expressed in the article do not represent the official position of the platform. We recommend that readers conduct their own research and consult with a professional before making any investment decisions.

Compiled and analyzed by HCCVenture

Follow HCCVenture here: https://linktr.ee/holdcoincventure

Explore HCCVenture group

HCCVenture © 2023. All rights reserved.

Connect with us

Popular content

Contact to us

E-mail : sp_contact@hccventure.com

Register : https://linktr.ee/holdcoincventure

Disclaimer: The information on this website is for informational purposes only and should not be considered investment advice. We are not responsible for any risks or losses arising from investment decisions based on the content here.

TERMS AND CONDITIONS • CUSTOMER PROTECTION POLICY

ANALYTICAL AND NEWS CONTENT IS COMPILED AND PROVIDED BY EXPERTS IN THE FIELD OF DIGITAL FINANCE AND BLOCKCHAIN BELONGING TO HCCVENTURE ORGANIZATION, INCLUDING OWNERSHIP OF THE CONTENT.

RESPONSIBLE FOR MANAGING ALL CONTENT AND ANALYSIS: HCCVENTURE FOUNDER - TRUONG MINH HUY

Read warnings about scams and phishing emails — REPORT A PROBLEM WITH OUR SITE.