Bitwise: Cryptocurrency stocks rise 23% while tokens fall 36%

The Bitwise Crypto Innovators 30 Index, which tracks the 30 largest listed companies building the cryptocurrency economy, posted a 23% gain in the first half of 2026, while the Bitwise 10 Large Cap Crypto Index fell 36% during the same period.

7/16/20265 min read

What are cryptocurrency stocks and why are they better than tokens?

The Bitwise Crypto Innovators 30 index tracks publicly listed companies whose primary economic activity relates to the cryptocurrency economy – exchanges, mining companies, treasury management companies, stablecoin issuers, tokenization platforms, and blockchain financial services companies. Companies holding the index in the first half of 2026 included Coinbase, Strategy, MARA, Galaxy Digital, BitMine, IREN, Cipher Mining, Hut 8, Riot Platforms, and Figure Technologies, among others. The 23% increase in the first half of the year was more than double the returns of US stocks during the same period, meaning that cryptocurrency stocks outperformed traditional stocks by a larger margin than traditional stocks outperformed cryptocurrency tokens in absolute percentage terms.

The 59-point difference between cryptocurrency stock performance and cryptocurrency token performance is the largest gap in the current cycle. This reflects a structural characteristic of the current bear market, distinct from previous crypto downturns: cryptocurrency tokens are declining while companies building cryptocurrency infrastructure are growing their business. Bitcoin miners are capitalizing on the demand for AI infrastructure through energy-backed land conversion. MARA's acquisition of 1,200 acres in Texas, Core Scientific's CoreWeave deal, TeraWulf's Anthropic lease, and their equity values reflect the AI infrastructure opportunity regardless of Bitcoin's price. Stablecoin issuers, including Circle, are increasing their reserve income from the interest rate environment while their token product (USDC) is not depreciating by design. Tokenization platforms and blockchain-based financial services companies are capturing adoption momentum from institutions that the tokens they build upon do not have.

Rasmussen's view that these are businesses that generate fees and continue to profit in a bear market without relying on token price appreciation distinguishes the structural characteristics of cryptocurrency equity resilience from the speculative correlation that has historically linked cryptocurrency equity and cryptocurrency token performance in the same direction.

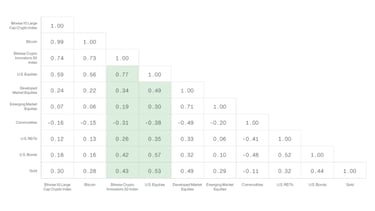

All other major asset classes increased in value.

The macroeconomic context amplifies the 59-point disparity as to how the decline in cryptocurrencies during the first half of the year is detached from the broader performance picture of asset classes. Among the major asset classes in the first half of 2026, only cryptocurrencies and gold recorded negative returns – gold fell approximately 7%, and the Bitwise 10 Large Cap Crypto Index dropped 36%. Every other major asset class – US stocks, developed market stocks, emerging market stocks, REITs, and bonds – recorded positive returns. Rasmussen describes this as one of the reasons why “this crypto winter feels particularly harsh – it’s a lonely winter.”

The decline in cryptocurrencies, separate from the broader asset performance picture, reflects specific macroeconomic challenges that fueled the weakening of cryptocurrencies in the first half of 2026: the hawkish policy shift of the Federal Reserve under Chairman Kevin Warsh eliminated expectations of interest rate cuts, strong economic data reduced the relative appeal of non-yielding alternative assets, and institutional capital flows diverted to AI stocks, creating a direct competitor to the speculative flows that supported Bitcoin until the end of 2025. These factors directly impacted cryptocurrency tokens while keeping cryptocurrency stocks partly protected by exposure to the same AI infrastructure theme that is attracting capital flows diverted away from tokens.

Compare the fundamental factors across cycles.

Bitwise's report includes a comparison between current fundamental indicators and those at the bottom of the 2022 bear market, placing the current token price weakness in historical context. Ethereum's on-chain transaction activity has increased approximately thirteenfold since Q2 2022. DeFi's total value locked (VAT) has increased by over 60% since 2022 levels. The stablecoin supply has doubled since the 2022 cycle bottom. Only token prices have yet to reflect the fundamental improvements recorded by the underlying network indicators.

The analytical implications of this comparison suggest that the current bear market is occurring on a significantly stronger fundamental basis than the 2022 bottom, which supports Rasmussen's argument for a recovery in the latter half of the cycle. The report doesn't provide precise timing, and Rasmussen frankly acknowledged the Q2 2026 results: The Bitwise 10 Large Cap Crypto Index fell 15.4% in Q2, eight out of ten constituent assets recorded negative returns, and spot Bitcoin ETFs recorded their worst quarterly outflows ever at $4.9 billion. These data complement, rather than contradict, the fundamental indicators supporting the report's argument that price and adoption have diverged, rather than price not weakening.

Stablecoins outperform Visa by 2.3 times.

The Q2 report identifies stablecoins as the clearest example of cryptocurrency infrastructure delivering measurable economic utility, independent of token price cycles. Stablecoins are outperforming Visa by 2.3 times in transaction volume, demonstrating that on-chain payments in US dollars have achieved a scale far exceeding the world's largest traditional payment network in raw throughput, even before considering 24/7 availability and cross-border transaction capabilities, factors that make stablecoin payments structurally different from Visa's service.

The stablecoin revenue picture reinforces the argument about the difference between equity and token at the company-by-company level: Tether generated approximately $482 million in revenue over 30 days, Circle approximately $193 million in revenue over 30 days, and Circle's quarterly reserve income reached $653 million, a 17% increase year-over-year, reflecting the impact of the interest rate environment on reserve income rather than any reliance on the appreciation of cryptocurrency tokens. The OCC's approval of Circle's national trust bank, received on July 10th, adds a legal certification that could further boost USDC adoption within institutions and expand reserve income as USDC distribution is enhanced through the integration of BNY's custody services and the competitive landscape of the PYUSD Polygon.

Assessment and Conclusion

Bitwise's Q2 report establishes an analytical framework for assessing the direction of the cryptocurrency market in the second half of 2026: whether the 59-point gap between cryptocurrency stocks and cryptocurrency tokens will converge in any direction, and which of the three scenarios that Cryptoslate identifies—tokens catching up with stocks, partial convergence, or persistent structural disconnect—will determine the second-half experience for different groups of cryptocurrency investors.

Tokens catching up to stock performance levels will occur if Bitcoin and major cryptocurrency assets recover to late 2025 price levels as the macroeconomic environment changes, if Federal Reserve policy shifts toward interest rate cuts, if outflows from institutional ETFs reverse as sentiment improves, or if Bitcoin's supply and demand dynamics from the April 2024 halving create a sustained supply-demand imbalance that the current bear market has temporarily masked. Partial convergence will occur if some tokens are driven by recovering fundamentals while cryptocurrency stocks decline from their first-half levels. Structural disconnect will continue if businesses building cryptocurrency infrastructure continue to grow while the tokens those businesses use for transactions fail to generate commensurate economic value through fee burning, buybacks, or staking rewards. Rasmussen's expectations for a cryptocurrency recovery in the second half of the year reflect the probability of the first scenario, while the report's emphasis on fundamental factors ensures that the investment thesis remains viable even if the recovery extends beyond the calendar year.

Disclaimer: The information presented in this article is the author's personal opinion in the field of cryptocurrencies. This is not financial or investment advice at all. Every investment decision should be based on careful consideration of your personal portfolio and risk tolerance. The opinion in the article does not represent the official position of the platform. We recommend that readers do their own research and consult experts before making any investment decisions.

Synthesized and analyzed by HCCVenture

Follow HCCVenture organization here: https://link3.to/holdcoincventure

Explore HCCVenture group

HCCVenture © 2023. All rights reserved.

Connect with us

Popular content

Contact to us

E-mail : sp_contact@hccventure.com

Register : https://linktr.ee/holdcoincventure

Disclaimer: The information on this website is for informational purposes only and should not be considered investment advice. We are not responsible for any risks or losses arising from investment decisions based on the content here.

TERMS AND CONDITIONS • CUSTOMER PROTECTION POLICY

ANALYTICAL AND NEWS CONTENT IS COMPILED AND PROVIDED BY EXPERTS IN THE FIELD OF DIGITAL FINANCE AND BLOCKCHAIN BELONGING TO HCCVENTURE ORGANIZATION, INCLUDING OWNERSHIP OF THE CONTENT.

RESPONSIBLE FOR MANAGING ALL CONTENT AND ANALYSIS: HCCVENTURE FOUNDER - TRUONG MINH HUY

Read warnings about scams and phishing emails — REPORT A PROBLEM WITH OUR SITE.