Bitcoin L2s: The process of forming Layer2 on the Bitcoin blockchain

Since 2021, the number of Layer 2 (L2) projects built on Bitcoin has increased more than sevenfold, from 10 to 75. More than 36% of all venture capital invested in Bitcoin L2 has been allocated in 2024.

12/3/202410 min read

I. Summary

Since 2021, the number of Layer 2 (L2) projects built on Bitcoin has increased more than sevenfold, from 10 to 75. More than 36% of all venture capital invested in Bitcoin L2 has been allocated in 2024. Since 2018, crypto venture capital firms have poured a total of $447 million into Bitcoin L2 projects.

Bitcoin L2 will use this capital to develop powerful applications and new use cases for BTC, attracting significant liquidity from both native BTC holders and the existing wrapped BTC market. The report estimates that over $47 billion in BTC could be bridged into Bitcoin L2s by 2030.

Our total addressable market (TAM) analysis for Bitcoin L2 looks at the current market share of all wrapped versions of BTC used in DeFi, native BTC held on Bitcoin L2s, and BTC locked in staking protocols.

As of November 20, 2024, these segments account for 0.8% of total circulating BTC. By 2030, we estimate that 2.3% of circulating BTC supply will be bridged into L2 Bitcoins to interact with new Bitcoin DeFi ecosystems, fungible tokens, payment applications, and more.

II. Some overview of Bitcoin and Layer 2

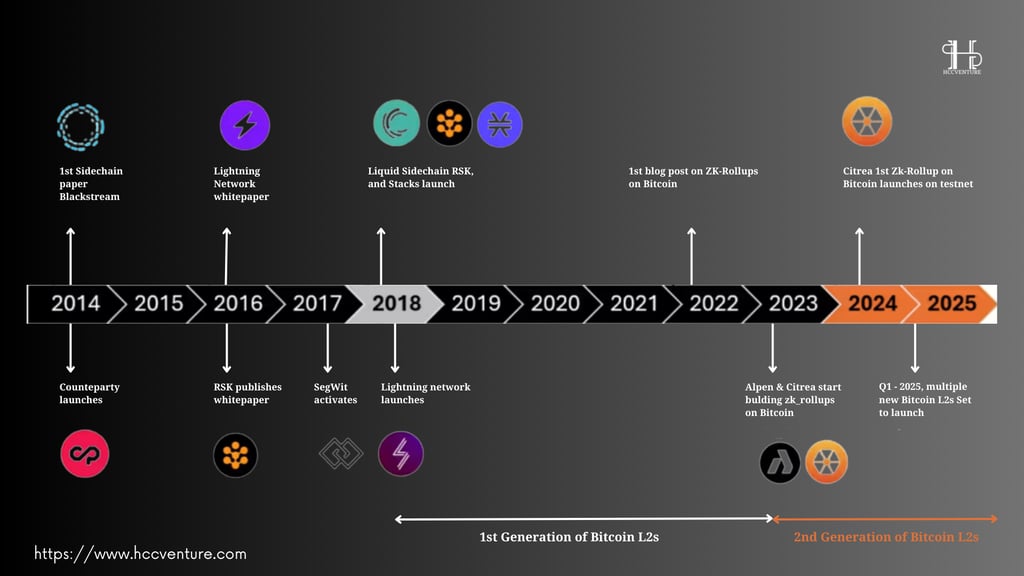

Tether launched on the Omni Network, one of the first Layer 2s, in 2014, an initiative that has been described as “Bitcoin 2.0”. Disputes over whether Bitcoin should scale its base layer in lieu of high-performance L2s culminated in the “Blocksize War”, which was largely resolved in August 2017 with the activation of SegWit on Bitcoin and the launch of Bitcoin Cash.

The rise of Ordinals brought cryptography back to Bitcoin’s base layer in 2023 and helped reignite interest in building applications on Bitcoin. That renewed interest, coupled with advances in Rollup development within the Ethereum development community, has led to a new wave of Layer 2 Bitcoins, largely using Rollup technology (both optimistic and ignorant).

A large part of the difficulty is due to Bitcoin’s inability to support general-purpose smart contract applications. Bitcoin’s base layer is not Turing-complete and therefore cannot execute the smart contract logic required for most DeFi applications. However, future upgrades could enable features that improve multi-party custody, enable more robust bridging, and enable Layer 2 schemes.

Wrapped Bitcoin (WBTC) on Ethereum has the largest market share (62%) of all wrapped versions of BTC. Wrapped versions of BTC used in Ethereum DeFi represent a significant demographic of BTC holders looking for more productive use cases for BTC.

Over $9 billion worth of wrapped BTC on Ethereum (WBTC, tBTC, cbBTC) may indicate user demand for BTC in DeFi applications. WBTC, tBTC, and other bridge BTC holders are more likely to move and use BTC on new Bitcoin L2s than other groups because they are familiar with operating wrapped BTC assets on other chains.

This report defines the key features of Bitcoin L2 and provides a high-level overview of different types of Bitcoin scaling solutions. The report also analyzes the $447 million in crypto VC investment in Bitcoin L2 since 2018 and provides a TAM analysis for the emerging Bitcoin L2. Finally, the report shares key insights into the future prospects of Bitcoin’s modularity.

III. What is Bitcoin Layer 2?

Bitcoin L2 provides higher transaction throughput than Bitcoin L1 by implementing larger and faster blocks. Bitcoin L2 operates as its own execution environment and thus can avoid the technical limitations that exist on Bitcoin L1, such as the lack of Turing completeness. By operating as a standalone execution environment, Bitcoin L2 can use its own consensus mechanism, security framework, and virtual machine.

Bitcoin L2 Highlights:

Higher transaction throughput: Bitcoin L2 achieves this by implementing larger and faster blocks.

Independent execution environment: L2 operates separately, avoiding the technical limitations of Bitcoin L1 (e.g. lack of Turing completeness).

Customization: L2 can use its own consensus, security, and virtual machine. Many Bitcoin L2s are EVM compatible, allowing for integration of applications from other EVM blockchains.

Bridge mechanism:

Function: Allows users to move BTC from base layer (L1) to L2.

Method:

Use a multi-signature wallet (Multisig) or a multi-party custody (MPC) mechanism.

Some L2s use BitVM , a Bitcoin-compatible off-chain Turing-complete virtual machine, with a 1-in-n trust mechanism.

Multi-signature/MPC bridges require more than 50% of signers to be honest to ensure withdrawal.

Comparison with Ethereum L2:

L2 Ethereum Bridge: Based on smart contract accounts.

Bitcoin L2 Bridge: Uses public key addresses, usually does not support unilateral exit.

Ethereum Rollups allow for forced withdrawals in case the arranger fails, while Bitcoin L2 (except Lightning Network) requires a trusted intermediary.

Trustless Exit:

Lightning Network: The only L2 Bitcoin that supports trustless withdrawals, as long as the user has the most recent balance state.

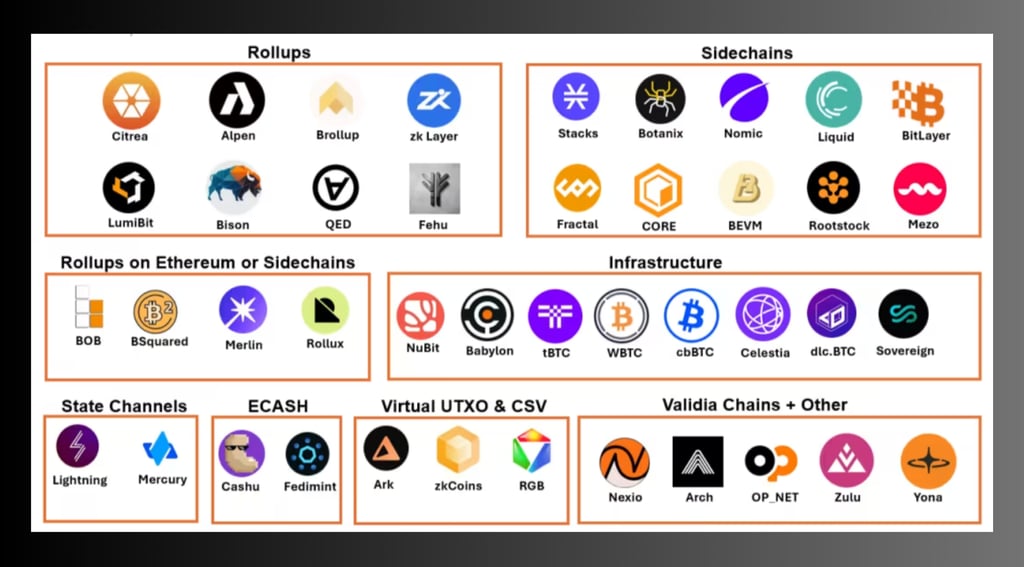

IV. Bitcoin Rollups và Sidechains

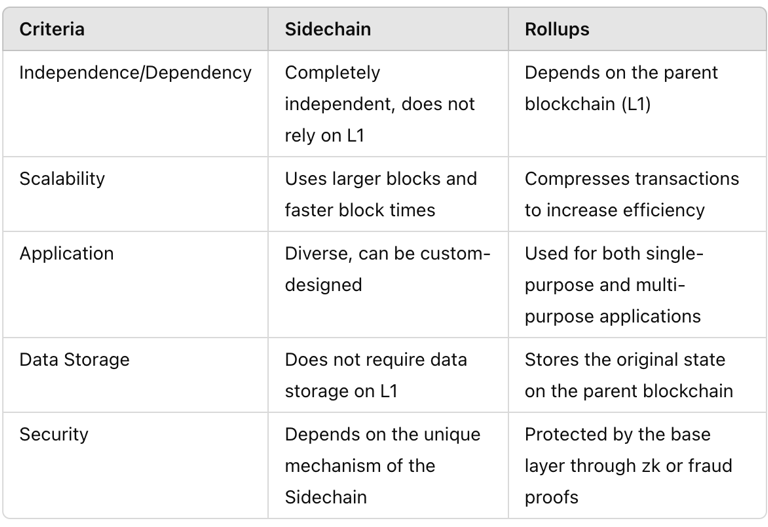

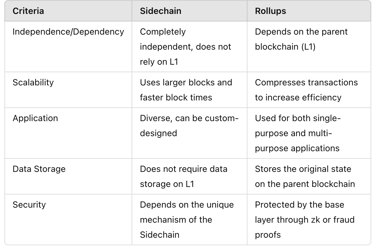

There are two types of Bitcoin L2 solutions that can support general-purpose application development: Rollup and Sidechain. State Channels are another L2 solution being developed on Bitcoin, most notably the Lightning Network, but the technology is primarily used to enable faster and cheaper peer-to-peer transactions on Bitcoin and cannot currently support Turing-complete smart contracts.

1. Sidechain:

Definition: A standalone blockchain that runs parallel to the Bitcoin base layer via embedded connections.

Main features:

Scalability: Increase the number of transactions processed thanks to larger blocks and faster block times.

Independent Consensus Model: Independent of the Bitcoin base layer, acts as an independent execution environment.

Integration with L1: Can post hash of block header or other data to L1 to “checkpoint” state.

Controversy: Sometimes not considered a true L2 solution because it does not depend on a base layer like Rollup (Example: Polygon is Ethereum's Sidechain).

Applications: Flexible design for different purposes, from blockchain compatible to bespoke solutions.

2. Rollups:

Definition: A secondary blockchain that executes transactions from the base layer on a secondary layer, providing faster and cheaper transactions.

Main features:

Transaction efficiency: 10-100 times faster than Sidechain thanks to data compression algorithm.

Depends on parent layer data: The parent blockchain stores the original state and allows any full node to reconstruct the most recent state.

Flexibility: Supports a single application or multi-purpose functionality with multiple applications.

Rollups Classification:

Zk-Rollups: Create short, instantly verifiable cryptographic proofs on L1, ensuring transaction correctness.

Optimistic Rollups: Update the root state optimistically on L1, providing time to verify or challenge.

The above market map classification follows the following main characteristics:

Bitcoin Rollups: The execution layer posts proof data and state or transaction data into Bitcoin blocks.

Rollups are not available on Bitcoin: The execution layer posts proofs and diffs of state or transaction data on Ethereum or an alternative DA layer.

Side chain: Independent execution layer compatible with Bitcoin base layer and does not need DA from main chain.

Infrastructure: Data availability protocol and any BTC provider bundled.

State Channel : Off-chain execution environment has no global state but only commits to the initial and final state of account balances.

ECASH: State Custody Channel solution based on David Chaumian's Ecash proposal.

Virtual UTXO & CSV: New versions of State Channels and execution layers using client-side verification.

Validia Chain: BTC compatible execution layers and uses off-chain DA or alternative DA.

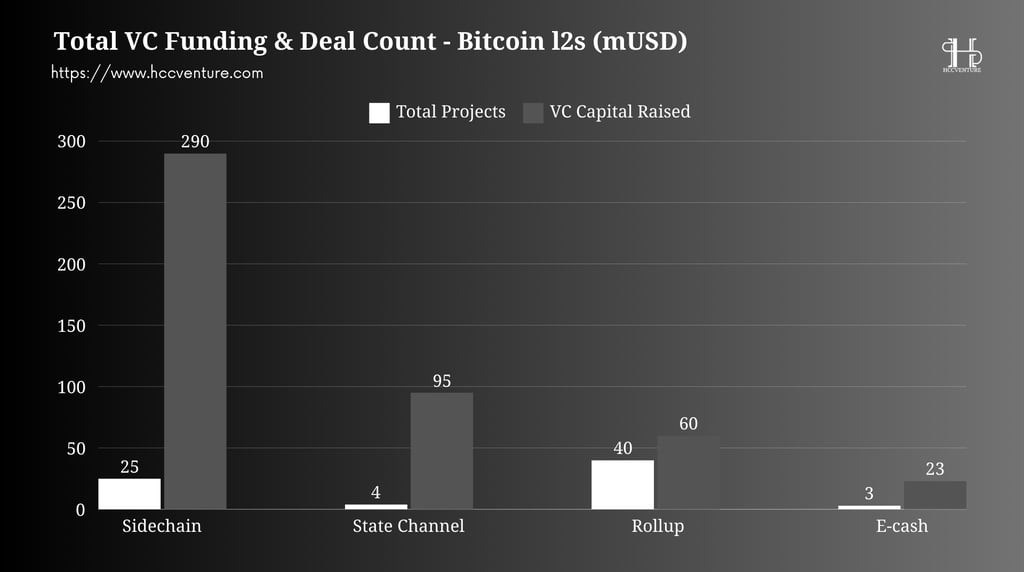

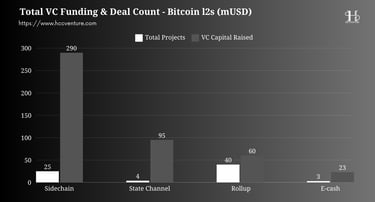

The market map does not include all projects in each category and serves as a reference for the different types of projects building in the Bitcoin L2 ecosystem. As of November 20, 2024, the Bitcoin L2 market consists of 40 Rollups and 25 Sidechains. This report does not cover State Channels, CSV, Drivechain, or ECash protocols, which represent a total of 10 projects.

V. VCs investing in Bitcoin L2s

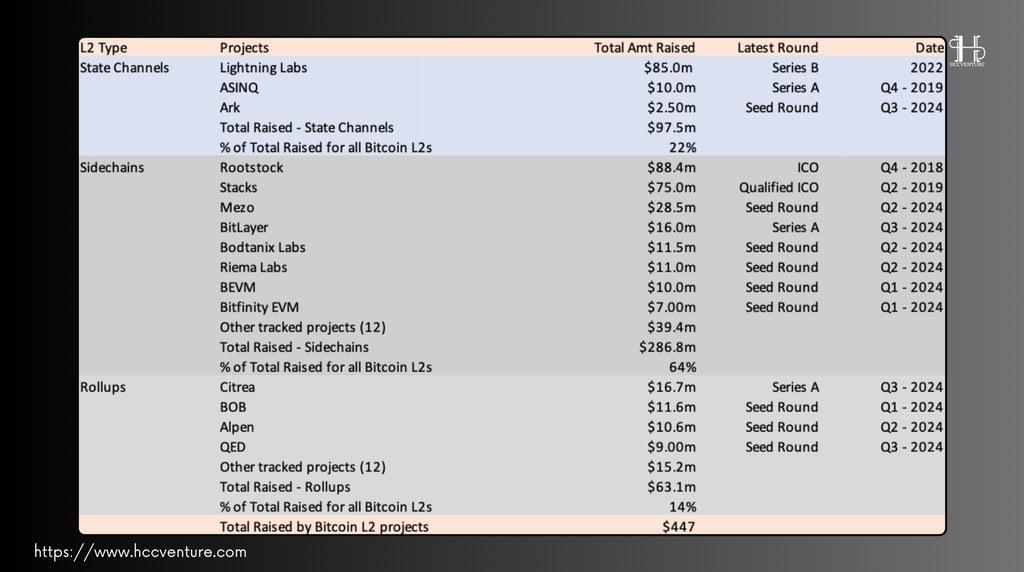

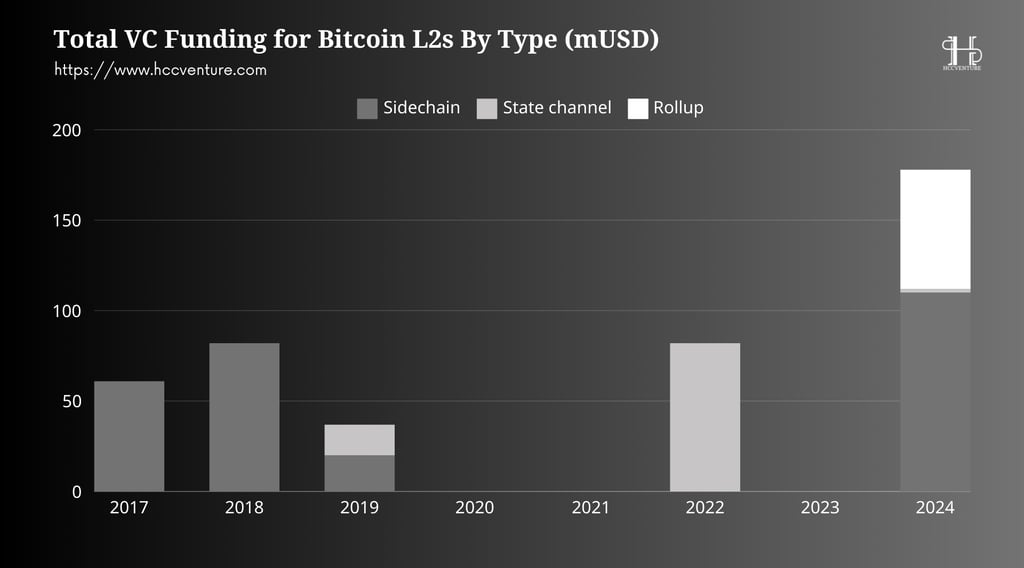

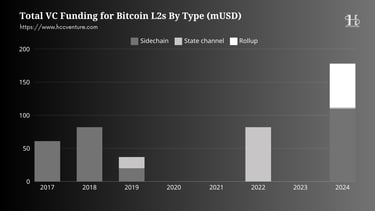

As of September 2024, Bitcoin L2 has raised $174 million in funding from crypto VCs. Of this total, Sidechains received the largest allocation at $105 million, followed by Rollups at $63 million.

Notably, 39% of all historical VC investment into Bitcoin L2s occurred in 2024 alone. Q2 2024 saw a significant shift, with Bitcoin L2s accounting for 44% of all crypto VC invested in L2 solutions across the industry—a staggering 159% increase quarter-on-quarter.

The surge in crypto VC investment in Bitcoin L2s in 2024 shows that traditional crypto VCs, excluding Bitcoin-focused funds, had virtually no exposure to the Bitcoin ecosystem before 2024.

Since 2018, Bitcoin Layer 2 has attracted significant investment, with Sidechains leading the way. Of the total $447 million invested in Bitcoin L2:

Sidechains received the largest share at 64%.

State Channels follows with 22% of the capital.

Guaranteed rollups 14%.

It should be noted that ECASH-based protocols such as Cashu and Fedimint were excluded from the above table and received a total of $27.2 million in VC funding. E-Cash projects do not fit our definition of Bitcoin L2, but are worth including as potential infrastructure in the Bitcoin L2 space.

VI. Total Addressable Market for Bitcoin L2

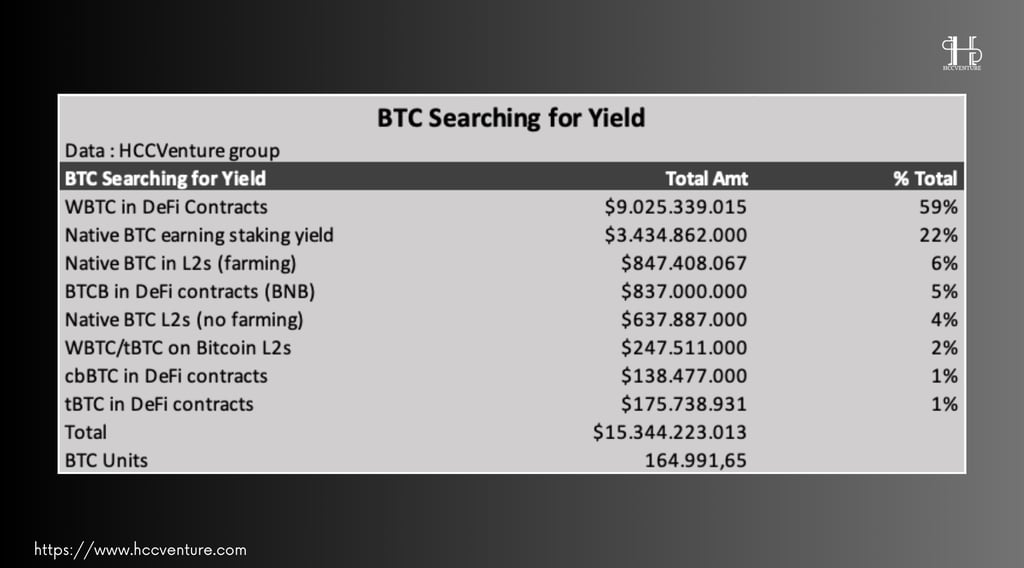

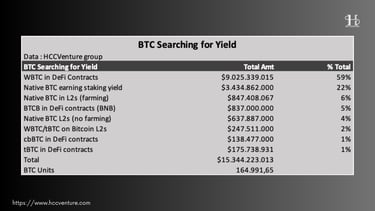

We view the potential market for Bitcoin L2 as consisting of BTC wrapped in DeFi, native BTC on L2, and BTC in staking protocols. This is the “active” BTC supply pool, focused on holders willing to connect BTC to L2 to optimize returns.

About 0.8% of BTC's circulating supply, 164,992 BTC, is actively using DeFi as of November 20, 2024. 59% of this BTC is locked on Ethereum, 22% is locked on new Bitcoin staking protocols, and 10% is on Bitcoin L2.

For the wrapped BTC market, $10 billion is locked in DeFi smart contracts and $247 million is on Bitcoin L2. For the original bitcoin, $3.4 billion is locked in staking protocols (Babylon, Bouncebit) and $1.5 billion is locked on Bitcoin L2.

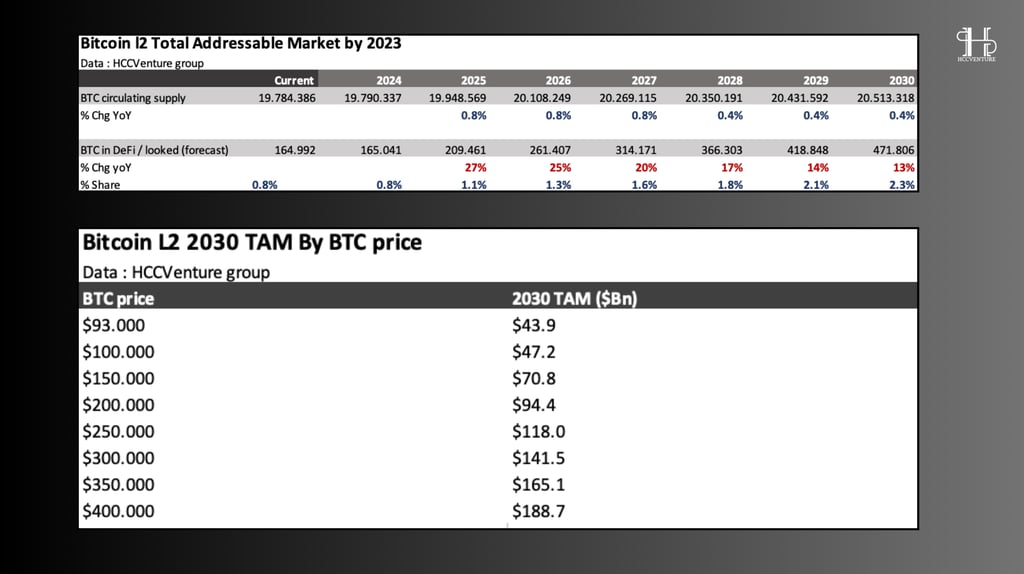

If we assume that the share of circulating BTC supply used for DeFi, L2, and Staking increases by 0.25% annually over 6 years, we estimate that the “active BTC supply” could increase to 471,806 BTC by the end of 2030 (a ~3x increase).

This consistent conservative growth rate will result in 2.3% of BTC supply active in DeFi, Staking, and Bitcoin L2 by 2030. For comparison, 2.3% of Ethereum's circulating supply (ETH, WETH, stETH, wstETH) is locked in DeFi smart contracts excluding staking protocols.

At current prices as of November 20, 2024, the model predicts a TAM for Bitcoin L2 of $44 billion by 2030. If BTC hits $100,000 by 2030, the TAM for Bitcoin L2 could then reach $47 billion, assuming that 2.3% of the total BTC supply is locked in Bitcoin L2 by 2030.

This analysis provides a rough estimate of how much BTC could flow into Bitcoin L2 in search of yield, based on the assumption that the BTC supply locked on L2 increases by 0.25% per year and the BTC price reaches $100,000 by 2030. The forecast depends on the growth of the DeFi and staking ecosystem on Bitcoin L2, as well as the ability to compete in yield with DeFi applications on Ethereum, where wrapped BTC currently dominates.

VII. Extracting Market Share from BTC DeFi on Ethereum

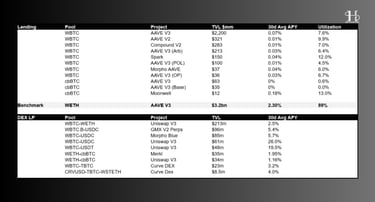

While there are new versions of wrapped BTC being used in DeFi, this section will focus solely on WBTC as this token accounts for 62% of the wrapped BTC market.

To extract significant market share from WBTC, lending protocols on Bitcoin L2 must

1) provide higher supply yield from increased BTC usage (users borrow BTC)

2) provide abundant stablecoin liquidity for borrowing.

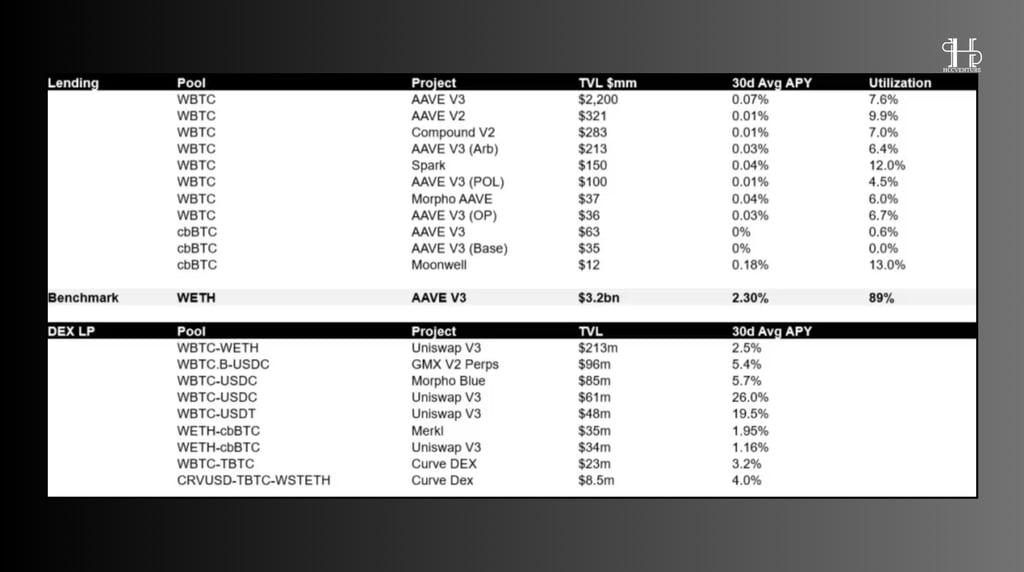

Approximately 72% of all DeFi contracts with WBTC locked are deposited into lending protocols. The large proportion of WBTC in lending protocols suggests that this group of BTC holders is only interested in lending applications. Furthermore, for every $100 of WBTC deposited into Ethereum's top two lending protocols, Aave and MakerDAO, ~$50 of the stablecoin is borrowed.

The large amount of stablecoins being borrowed against WBTC on AAVE and Maker is evident when looking at the average utilization rates for these deposit pools. On AAVE, the average utilization rate for WBTC is 7.7%, implying that 92.3% of deposited WBTC is used as collateral for stablecoin loans. As of November 2024, WBTC deposits on AAVE only receive an average of 0.04% APY. For reference, the utilization rate for WETH on AAVE is 89%, yielding 2.3% APY for WETH deposits.

The usage rate for WETH is much higher than WBTC because there is more utility for ETH/WETH than WBTC on Ethereum. Use cases for WETH include DeFi, perp trading, staking, and NFTs. Lending applications on Bitcoin L2 are positioned to provide higher returns from the increased utility of BTC by building specialized ecosystems for the asset. Some examples include Ordinals and fungible token protocols built on Bitcoin L2

While depositing WBTC into DEX pools offers higher returns than lending pools, the risk of impermanent loss and yield volatility make DEX pools an unreliable source of returns.

Evaluation and Conclusion

To take market share from Bitcoin DeFi solutions on Ethereum such as WBTC, tBTC, and cbBTC, DeFi applications on Bitcoin L2 need to offer more attractive yields. The ability to provide high yields will be the deciding factor in attracting users from the Ethereum ecosystem to Bitcoin L2.

A vibrant DeFi ecosystem is a prerequisite for the long-term growth of Bitcoin L2. Lending, DEX, and derivatives platforms, similar to high TVL applications on Ethereum L2 (such as Arbitrum, Optimism, and Base), will play a core role in driving Bitcoin L2 adoption.

With $174 million in VC funding by 2024, Bitcoin L2 projects have the resources to execute go-to-market strategies, build ecosystem funds, and integrate EVM applications. Continued investment in Bitcoin L2 will be a key driver of industry growth over the next 6 years, laying the foundation for L2 projects to achieve sustainable success.

The introduction of Ordinals and BRC-20 in 2023 opens up new investment opportunities in Bitcoin beyond its traditional role as digital gold. Crypto VC funds will continue to invest in the Bitcoin ecosystem as L2 Bitcoins mature and expand their user base.

Of the current 75 L2 Bitcoins, only about 3-5 platforms are likely to dominate the market. Limited users, liquidity, and attention will make it difficult for most other projects to maintain long-term competition.

Join the HCCVenture community to get the latest market information. Once again we give our opinion on potential projects in the crypto market. This is not investment advice, consider your investment portfolio

Data from: data by HCCVenture

Join our telegram community: HCCVenture

Explore HCCVenture group

HCCVenture © 2023. All rights reserved.

Connect with us

Popular content

Contact to us

E-mail : sp_contact@hccventure.com

Register : https://linktr.ee/holdcoincventure

Disclaimer: The information on this website is for informational purposes only and should not be considered investment advice. We are not responsible for any risks or losses arising from investment decisions based on the content here.

TERMS AND CONDITIONS • CUSTOMER PROTECTION POLICY

ANALYTICAL AND NEWS CONTENT IS COMPILED AND PROVIDED BY EXPERTS IN THE FIELD OF DIGITAL FINANCE AND BLOCKCHAIN BELONGING TO HCCVENTURE ORGANIZATION, INCLUDING OWNERSHIP OF THE CONTENT.

RESPONSIBLE FOR MANAGING ALL CONTENT AND ANALYSIS: HCCVENTURE FOUNDER - TRUONG MINH HUY

Read warnings about scams and phishing emails — REPORT A PROBLEM WITH OUR SITE.