Analysis of recovery dynamics after rsETH and AAVE dominated Defi credit

Aave continues to assert its position as the largest decentralized lending protocol in the DeFi ecosystem. Despite being significantly affected by the rsETH incident related to KelpDAO and LayerZero in April 2026.

INSIGHTS

6/8/202620 min read

Analysis of recovery dynamics after rsETH and AAVE dominated Defi credit

Aave continues to assert its position as the largest decentralized lending protocol in the DeFi ecosystem. Despite being significantly affected by the rsETH incident related to KelpDAO and LayerZero in April 2026.

Analysis • 08 June, 2026

Defi's growth momentum in the next period

In the context of the digital asset market entering the phase of expanding liquidity in 2026, the Aave project continues to affirm the position of the largest decentralized lending protocol Defi system in the blockchain network. Despite the significant impact after the rsETH incident related to KelpDAO and LayerZero, Aave still has a significant impact on the growth of revenue, loan activity, GHO stablecoin and extended product ecosystem. On the other hand, Aave's capital flow, user activity and revenue generation efficiency have all remained at a historically high level, thereby reinforcing the thesis that Aave is entering a new growth phase with a more solid foundation than previous cycles.

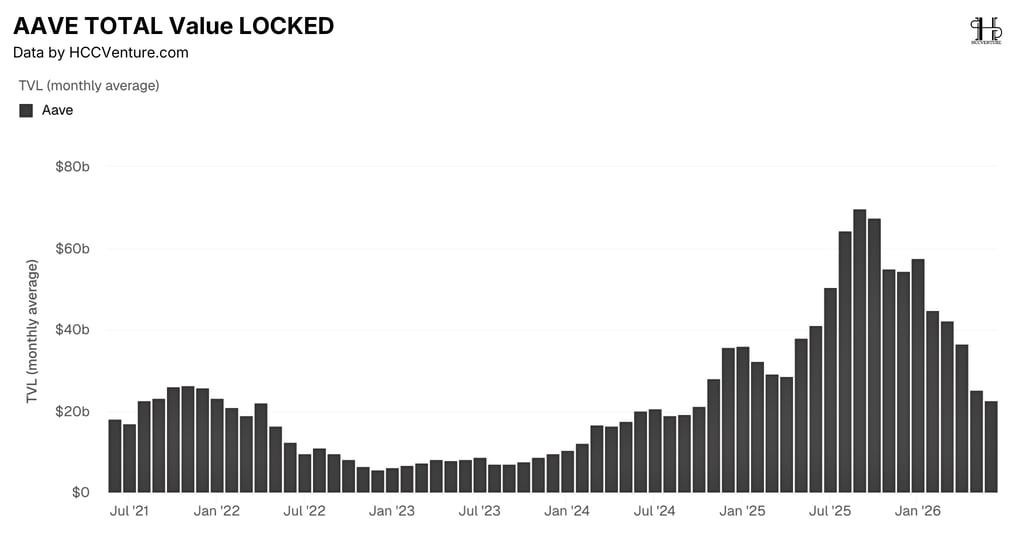

The total number of TVL-locked assets of Aave currently reaches 36.67 billion USD, down 13.39% compared to the previous month but still increased sharply by 27.29% compared to the same period last year. This TVL level is still in the highest group in the protocol's operating history, before the rsETH event, this figure exceeded the threshold of 42 billion USD. The decrease in TVL in April mainly comes from users actively withdrawing assets related to rsETH to minimize system risk, rather than capital flow fleeing from Aave.

Active Loans reached 15.45 billion USD, down 6.63% on a month-on-month but a sharp increase of 43.18% over-year, in lending protocols with this growth, Aave still maintains financial lending activities and shows that the demand for leverage and liquidity in the DeFi ecosystem is still very large.

Some other financial data reports are statistically recorded by HCCVenture:

Total protocol fees (Fees) reached 56.53 million USD, up 28.63% on a month and up 58.67% on a year.

Actual revenue (Revenue) reached 7.80 million USD, up 17.39% month-on-month and 49.98% year-on-year.

Aave currently accounts for 58.13% of the entire DeFi lending industry.

GHO currently reaches 532.35 million USD, up 3.47% month-on-month and 138.42% over the same period last year.

The number of monthly active users reached 116,600 addresses, increasing by 1.75% on a month and by 11.79% on year.

Usually, liquidity stress events will impair the operation of the protocol. However, in the case of Aave, the increase in volatility has triggered many borrowing activities, rebalancing collateral and liquidating positions, thereby increasing the amount of fees incurred on the system. Compared to the bear market period in 2023 when monthly revenue only fluctuated around 2 - 3 million USD, the current revenue has increased nearly three times, reflecting that business efficiency is improving significantly.

Unlike previous cycles, user growth now no longer depends mainly on individual investors but is being driven by institutions, DAOs, liquidity funds and other DeFi protocols using Aave as the credit infrastructure layer. It is worth noting that user growth is still maintained during the market period affected by the rsETH incident. This shows that the community's trust in Aave has not diminished.

Although TVL and market share are negatively affected by the general situation of the market, core indicators such as revenue, protocol fees, outstanding loans and GHO growth continue to improve. At the same time, liquidity, credit activity and demand for stablecoins show that Aave is entering a new era with the credit system of Defi and Web3.0, the largest decentralized credit center in the crypto market today.

Aave's biggest liquidity test in 2026

In April 2026, the most stressful event for the Aave ecosystem occurred after a Defi boom cycle, which stemmed from the incident involving KelpDAO's LayerZero bridge for the rsETH liquidity staking asset on April 18, this event caused part of the rsETH supply in the market to no longer be fully guaranteed by the base ETH. Although Aave's smart contracts are completely unopened and do not have any security holes related to the protocol, Aave is still directly affected by rsETH created as collateral in lending protocols.

The decline in confidence in this type of asset has increased liquidity pressure, forcing TVL to a low level after the period of anchoring above, the size of loans has decreased severely in the short term. From the valuation of collateral and poor risk control, the crypto loan market has had a serious crash of trust.

TVL decreased by 13.39% month to 36.67 billion USD and Active Loans decreased 6.63% to 15.45 billion USD. However, during the same period, total protocol fees increased by 28.63% to 56.53 million USD and real revenue increased by 17.39% to 7.80 million USD.

However, instead of creating a system crisis, this event becomes an important test of Aave's ability to manage risk -> the protocol still maintains stable operation, liquidation mechanisms continue to operate effectively and there is no systemic loss to the core protocol.

DeFi United reflects the power of Defi's ecological link

To deal with the consequences of the rsETH event, Aave's service units launched the DeFi United initiative to fully restore the guarantee rate of rsETH and normalize liquidity conditions across the entire ecosystem. With the "DeFi United" event established to deploy and gather the most DAOs, the infrastructure development organization and community members to support the event.

According to data from HCCVenture statistics from Aave report, the program has mobilized with a commitment of about 300 million USD in asset value, equivalent to 137,000 ETH to support the process of restructuring the source of security assets for rsETH before.

An important part of the recovery plan comes from the reopening of KelpDAO's rsETH withdrawal mechanism as well as the governance process of Arbitrum DAO to release the frozen ETH under the management of Arbitrum Security Council. Notably, the first round of Arbitrum DAO's Snapshot voting qualified for voting with an overwhelming support rate, showing that the community is strongly agreeing on the asset recovery plan.

The fact that a capital of hundreds of millions of dollars is mobilized in a short time reflects the huge belief of participants in the long-term value of the Aave ecosystem as well as the central role of the protocol in the DeFi liquidity structure.

According to the Aave Labs team, Aave V4 continued to operate normally during the event and set a new peak in deposits with more than 50 million USD of assets deposited into the protocol. The fact that Aave V4 is still attracting new capital flows during the market instability period shows that investors' trust in the new generation of the protocol's architecture has not been affected at all, and confirms that the rsETH incident is a separate problem of specific collateral, rather than reflecting the systemic risk to Aave.

In the long term, the Hub-and-Spoke architecture of Aave V4 is expected to significantly expand the ability to customize the credit market, improve capital efficiency and create more revenue growth motivation for the protocol.

The network system is operating to optimize capacity

The total value of Aave's TVL lock assets in the period from 2021 to 2026 reflects a round of Defi's growth, although TVL at this time has had a significant correction from the previous historical peak in 2025, but the current liquidity scale is still many times higher than those regions in previous cycles, thereby confirming Aave's position in the field of protocol lending is still very large.

After setting a historical peak of nearly 70 billion USD, Aave's TVL began to adjust from the fourth quarter of 2025 and extended to 2026, up to now the average monthly TVL fluctuates around the area of 22 - 25 billion USD. In the historical context since its establishment, Aave's TVL is still 4 times higher than the bottom of 2023 and only about 15% lower than the peak of the 2021 cycle.

Most of the long-term liquidity is still maintained in the Aave ecosystem, the current correction is not accompanied by the collapse of the market structure or the wave of large-scale liquidity escape.

While many Defi protocols that had peaked in 2021 have lost most of their liquidity and cannot return to the previous scale, Aave not only fully recovered but also set a new peak 170% higher than the peak of the previous cycle.

Deep liquidity, standardized risk management mechanism, multi-chain ecosystem and the development of stablecoin GHO have created a system capable of attracting significantly more sustainable capital flows than competitors.

Another important factor is that the current TVL does not fully reflect the growth scale of new products such as Aave V4, Horizon and some deployments on Layer 2. Therefore, the actual economic scale of the ecosystem is larger than what is shown on the traditional TVL chart.

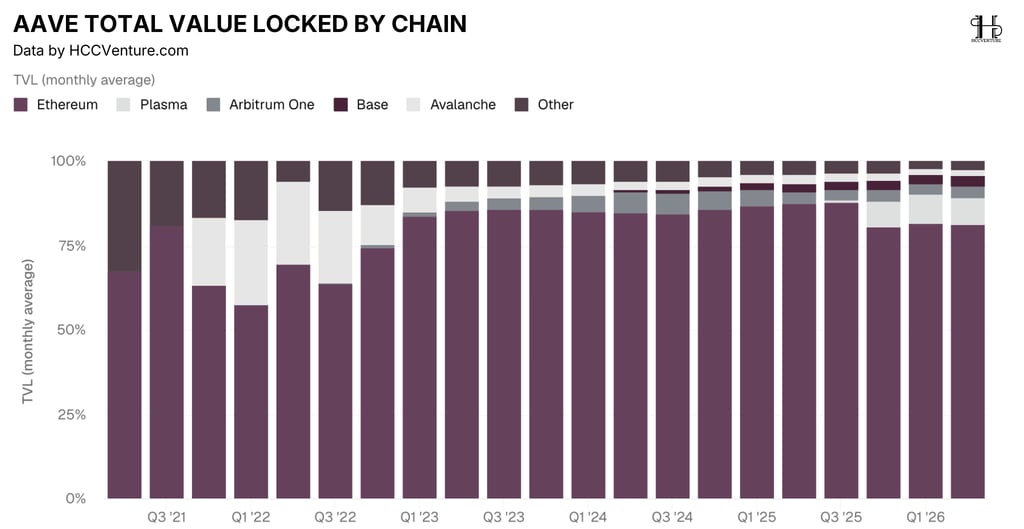

Aave's Total Value Locked (TVL) allocation data according to blockchain from the third quarter of 2021 to the second quarter of 2026 reflects a trend that the protocol has expanded to many different ecosystems, but Ethereum still maintains its role as the core liquidity center and the most important growth engine of the entire Aave network.

In the second quarter of 2026, Ethereum accounted for about 81 - 82% of the total TVL of the entire Aave ecosystem, it reflects a liquidity weight on Ethereum that has increased by about 25 percentage points since the bottom of the cycle, and the process of refocusing capital flows has been continuous for more than three years. The increase in Ethereum's proportion occurs simultaneously with the rapid expansion of liquid staking tokens, restaking and high-yield collateral strategies.

One of the most notable changes on the chart is the significant narrowing of the proportion of TVL from Avalanche, during the period 2021 - 2022, Avalanche used to contribute more than 20–25% of Aave's total TVL, becoming the second largest blockchain in the ecosystem. As subsidy yields decrease, capital flows tend to return to blockchains that possess natural liquidity and higher actual demand.

Arbitrum currently contributes about 3 - 4% of Aave's total TVL, significantly higher than in the 2023 period when there was almost no significant impact on the liquidity structure of the protocol. This growth reflects the growing demand for lending and liquidity provision activities that cost less than Ethereum but still inherit the security from the Ethereum ecosystem.

In fact, high liquidity concentration often helps improve capital efficiency, reduce market fragmentation and increase liquidity depth. For lending protocols like Aave, this is a particularly important factor because the ability to provide large loans directly depends on the depth of the collateral market.

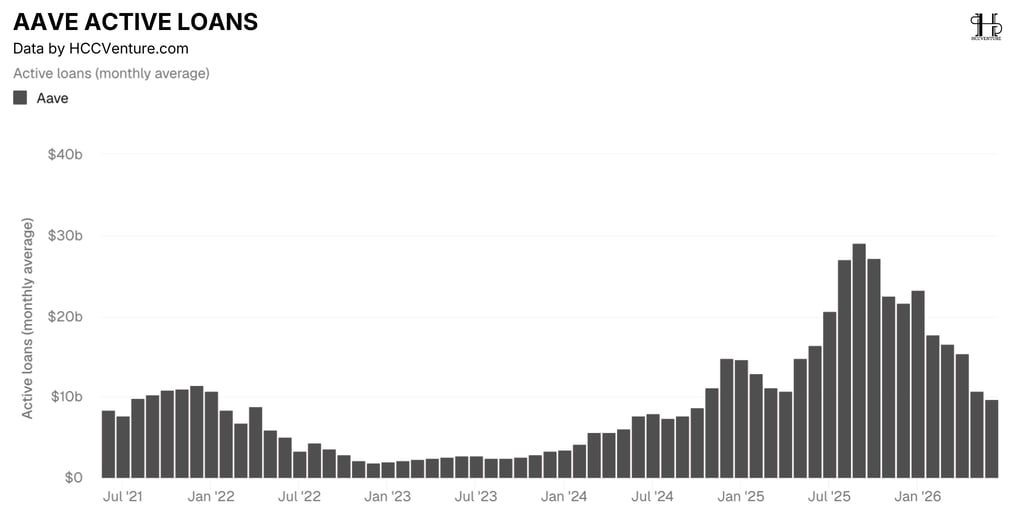

When assessing the operating capacity of decentralized finance, Active Loans are one of the most important measures to assess the actual need for capital of the market. Active Loans directly represents the scale of credit being absorbed by the DeFi economy, thereby reflecting the efficiency of capital use and the revenue generation ability of the protocol.

Statistics from HCCVenture on the blockchain, from mid-2021 to the second quarter of 2026 show that Aave has experienced a complete credit cycle including a period of sharp decline in the bear market in 2022 - 2023, to the current period, although the loan movement has adjusted after the historical peak established in 2025, the current debt balance is still maintained at a higher level compared to most of the time in the history of the protocol.

According to the latest data, Active Loans currently fluctuate around 9-10 billion USD. Compared to the historical peak, a decrease of about 65% can be considered significant, however, when placed in a long-term context, the current credit scale is still about 5 times higher than the bottom in 2023 and almost equivalent to the peak of the growth cycle in 2021. In other words, current borrowing activity is still maintained at a significantly higher level than at any time before 2024.

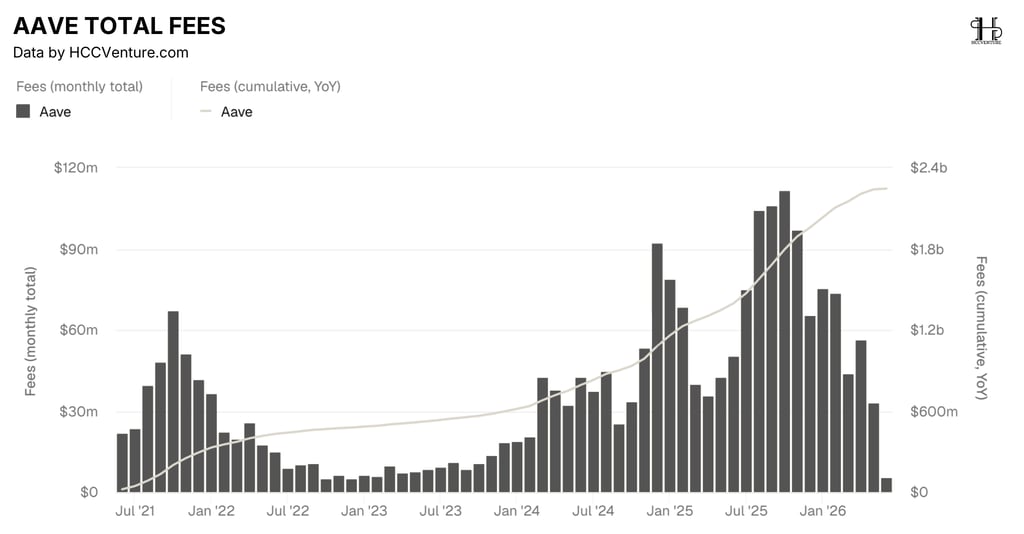

Although Aave has just experienced a strong fluctuation after a series of events related to the Defi system, the total protocol fee has continuously set new peaks in the period of 2024 - 2026. This factor is showing the demand for loans, leveraged trading activities, liquid staking and the expansion of decentralized credit products throughout the ecosystem. More importantly, the growth rate of revenue is far exceeding the growth rate of TVL in the same period, showing that Aave's capital efficiency is significantly improving.

One of the most notable data on the chart is the cumulative fees, which has now exceeded $2.2 billion, most of the economic value in Aave's history was created in the current cycle, the protocol has passed the initial testing phase and is entering the large-scale mining period.

After setting a peak of over 110 million USD/month in 2025, protocol revenue began to adjust in 2026 due to market leverage reduction and the impact of the rsETH event. However, the transaction fee on the protocol recorded in April 2026 still reached about 56.5 million USD.

In fact, Aave's revenue is still relatively high compared to the market decline period. The current balance adjustment after a period of too fast growth is a sign of the fundamental decline of the protocol.

This phenomenon often appears when a protocol enters the stage of optimizing capital efficiency. In other words, Aave not only attracts more cash flow but also exploits that cash flow more effectively through lending, leverage and more complex credit products. On the one hand, the assessment is positive for the prospects of the lending category in Defi.

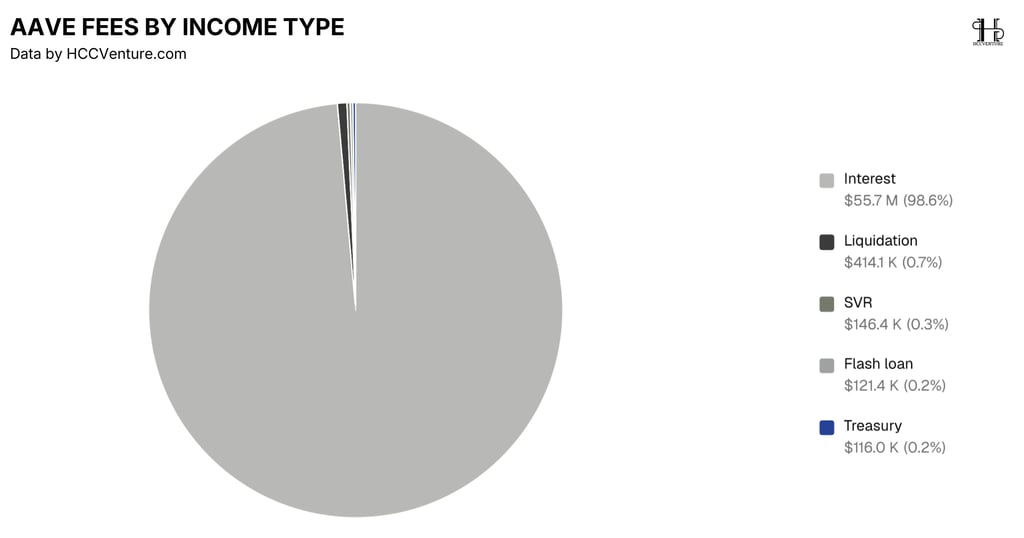

The revenue structure shows that the credit business model has entered the maturity stage. If revenue is generated mainly from speculative activities or unusual events such as mass liquidation, the sustainability of the business model is often questioned. Conversely, when most of the revenue comes from users' regular capital use, the protocol will have a stable growth platform and the ability to generate long-term cash flow.

According to the latest data, interest income (Interest Income) reaches about 55.7 million USD, equivalent to 98.6% of total revenue of the whole system.

The current rate is relatively high compared to the entire current Defi protocol, it is almost in sync with all the economic value created on Aave's ecosystem that comes from lending and asset lending activities instead of other auxiliary sources of income. In the blockchain market, a business model has reached a maturity level similar to the currency markets in traditional finance. Aave's current core activity is to connect capital owners with people who need to use capital, and collect fees based on the flow of credit taking place in the system.

Revenue from liquidation activities currently reaches about 414 thousand USD, equivalent to 0.7% of total revenue.

In lending protocols, revenue from liquidation often increases sharply when the market has sudden price drops or when the leverage rate increases excessively. However, the proportion of Aave's liquidation revenue currently accounts for less than 1% of total revenue, showing that the majority of users are still maintaining a safe collateral status, showing that Aave's risk management system continues to work effectively in controlling borrowing rates and limiting debts at risk of insolvency.

Current data shows that Flash Loan fees only contribute about 121 thousand USD, equivalent to 0.2% of total revenue.

In the early years of DeFi's development, Flash Loan was once considered one of Aave's iconic products. However, as the ecosystem matures, the economic role of Flash Loan has decreased relatively compared to traditional lending activities. Therefore, the current period has witnessed a sharp increase in the demand for long-term loans, using stablecoins and optimizing staking assets.

In addition to interest and liquidation, Aave currently records about 146 thousand USD in revenue from SVR (0.3%) and about 116 thousand USD from Treasury (0.2%).

Despite the small scale, these sources of revenue show that the protocol is gradually building additional revenue layers in addition to core lending activities. Therefore, in the long term of development. GHO, Aave Horizon and new products of Aave V4 can increase the proportion of income sources other than interest.

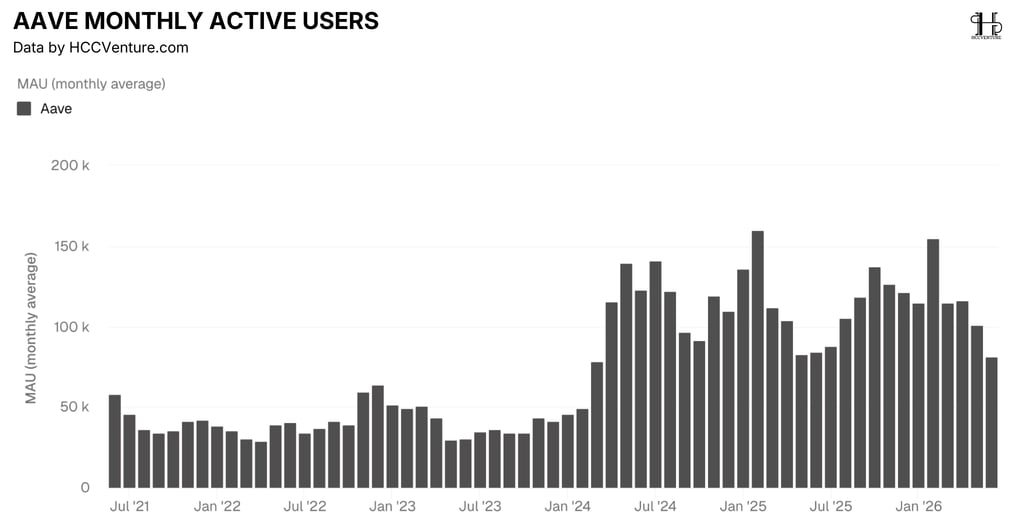

The number of monthly active users (Monthly Active Users - MAU) is one of the most important indicators reflecting the actual acceptance level of a protocol, with Aave, the growth of MAU is especially important because this is an operating protocol in the field of decentralized credit which is a segment that requires users to carry out actual economic activities such as depositing assets, borrowing, managing collateral or implementing dark strategies capital optimization.

After reaching a historical peak in 2025, the number of active users began to adjust in 2026 along with the general decline in market liquidity and the impact of the rsETH event. The latest statistical data shows that MAU currently fluctuates around the area of 80,000 - 115,000 users depending on the month, lower than the peak but still significantly higher than the entire period before 2024.

The majority of new users attracted in the past growth cycle are still continuing to use the protocol, the ecosystem does not witness the mass withdrawal of users but is just going through a natural adjustment period after a very rapid expansion process.

Although the number of users has adjusted in 2026, the current scale is still significantly higher than the entire period before 2024 and remains large enough to support liquidity, credit and revenue growth of the protocol.

Research and Analysis

Defi's growth momentum in the next period

DeFi United reflects the power of Defi's ecological link

The network system is operating to optimize capacity

Total Value Locked

Total Value Locked By Chain

Active Loans

Total Fees

Fees by income type

Monthly Active Users

Montly Active Users By Chain

Loans Market Share

Loans by Project

Horizon Total Value Locked

Evaluation and conclusion

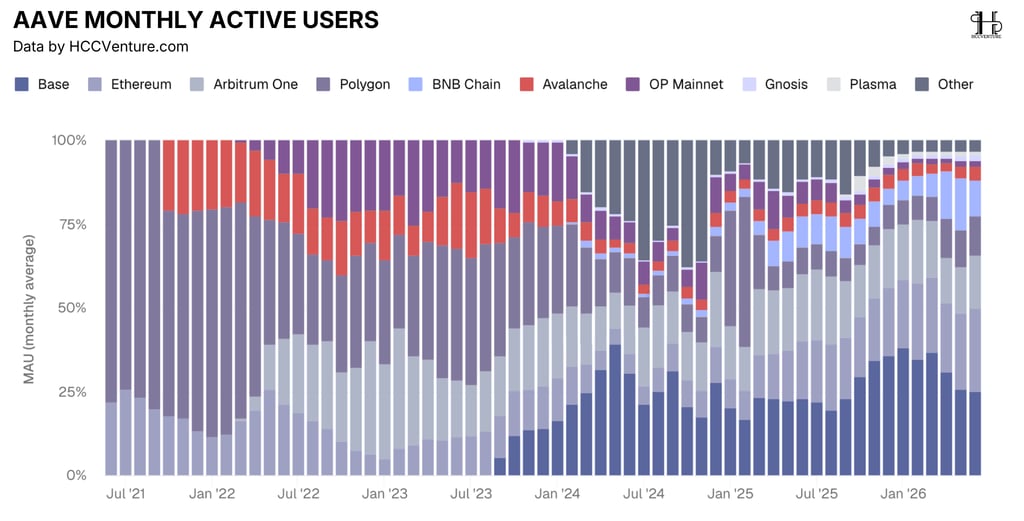

MAU allocation data by each blockchain from 2021 to mid-2026 reflects a structural change in Aave's development from a protocol that depends mainly on Ethereum and Polygon to a multi-chain ecosystem with new growth dynamics from Base, Arbitrum and Layer-2s of the Ethereum ecosystem.

Polygon's dominance in this period comes from significantly lower transaction costs than Ethereum when gas fees on Ethereum are still maintained at a very high level. However, as the Layer-2 ecosystem thrives from 2023 onwards, Polygon's user weight begins to decline. By 2026, Polygon's contribution rate is only about 10 - 12%, much lower than the previous peak period.

Ethereum continues to account for more than 80% of the protocol's total TVL as analyzed in previous sections, this network becomes a large center of liquidity and valuable assets, while user activity is increasingly shifting to Layer-2 with lower transaction costs. In other words, Ethereum is still the place where most of its assets are stored but it is no longer the leading blockchain in terms of the number of user interactions.

From 2023 onwards, Arbitrum begins to emerge as one of the largest user contributor blockchains to Aave. Data shows that the proportion of Arbitrum users increased from almost zero in 2021 to about 15-18% of the total MAU today and is one of the fastest growth rates in the entire ecosystem. The expansion of Arbitrum reflects the natural shift of users from Ethereum to Layer-2s that are capable of processing transactions faster and lower costs but still maintaining the same level of security as Ethereum.

From almost no contribution in 2023, Base has quickly become Aave's blockchain with the largest user density. The latest data shows that Base currently contributes about 25 - 35% of the total monthly active users of the protocol. The growth of Base reflects the success of the expansion strategy to the Coinbase ecosystem. With the ability to reach tens of millions of users from the Coinbase ecosystem and low transaction costs, Base is becoming Aave's largest retail user attraction gateway.

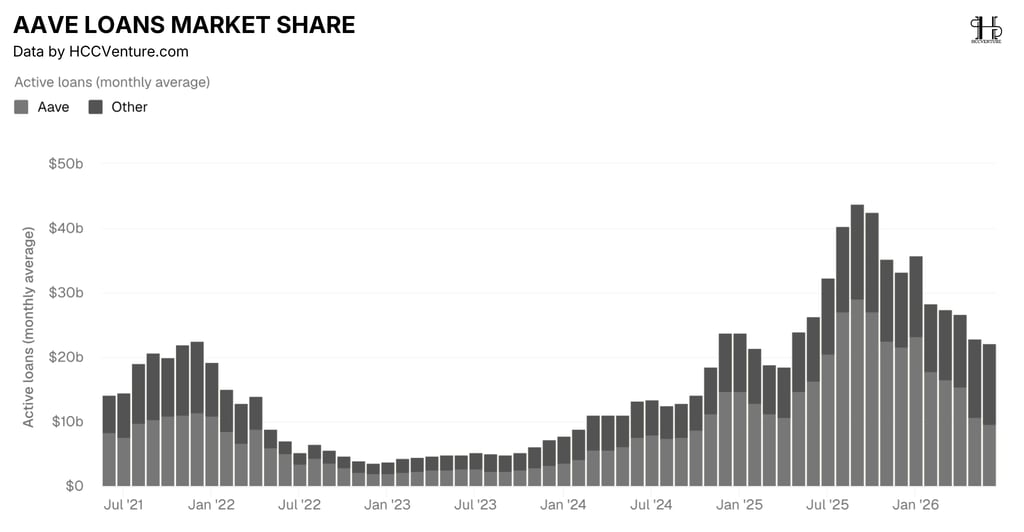

Credit market share (Loans Market Share) is one of the indicators that best reflects the true competitive position of a protocol, it controls most of the credit activities, which is often also the protocol that owns the deepest liquidity, the most effective risk management mechanism and the highest level of trust for users.

The latest data shows that the total debt balance of the whole industry is still around 22 billion USD. In which, Aave accounts for about 9 - 10 billion USD in active loan balances.

Although the industry-wide credit activity declined compared to the peak, Aave's contribution still remained above 55%, equivalent to the market share recorded in the latest on-chain reports of about 58%. Aave continues to be the protocol that benefits the greatest from the recovery of the decentralized credit market.

One of the most important conclusions from the chart is that the expansion of the market does not degrade Aave's position but on the contrary strengthens the competitive advantage of the protocol. Usually, when the market grows rapidly, the market share of leading businesses is often diluted by the appearance of new competitors. However, Aave's data shows the opposite.

From about 50% of the credit market share in 2021, Aave has raised its weight to over 60% in the period of 2024–2026, it reflects the formation of a very strong network effect in the ecosystem. Large liquidity helps attract more borrowers. The large demand for loans helps increase profits for depositors. Deeper liquidity continues to attract new capital flows. This cycle creates a growth loop that smaller protocols are difficult to compete with.

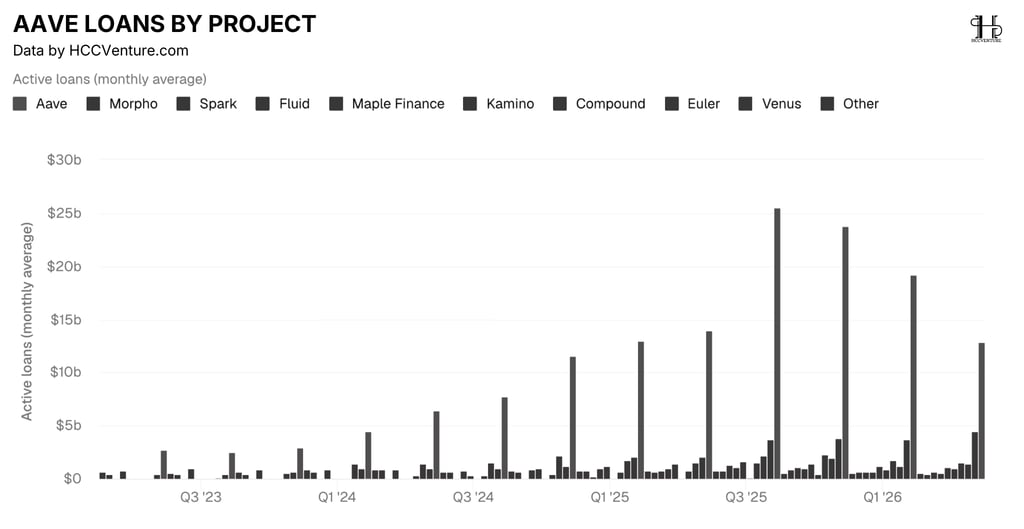

The gap with competitors is widening, establishing a unique position in the Lending DeFi market. While many competitors such as Morpho, Spark, Fluid, Compound, Euler, Kamino or Maple Finance have recorded strong growth in the current cycle, Aave still maintains an outstanding distance and continuously expands its leading position.

At the bottom of the 2023 cycle, Aave's outstanding loan size only fluctuates around 2 - 3 billion USD. However, along with the recovery of the crypto market and the expansion of staking, restaking and stablecoin activities, Aave's Active Loans grew continuously throughout 2024 and 2025. Even after the correction period in early 2026 and the impact of the rsETH event, Aave's credit scale remains around the area of 13-15 billion USD, about 5 times higher than the lowest level of the previous cycle.

If in 2023, Morpho's credit scale is almost negligible, by 2026 this protocol has expanded its loan debt to about 4 - 4.5 billion USD, becoming Aave's biggest competitor in the lending sector. However, when placed in correlation with Aave, the gap is still huge. At the moment, Morpho's loan balance is only equivalent to about 25 - 30% of Aave's credit scale. In fact, the development of Morpho reflects the expansion of the entire lending industry rather than the shift in market share from Aave

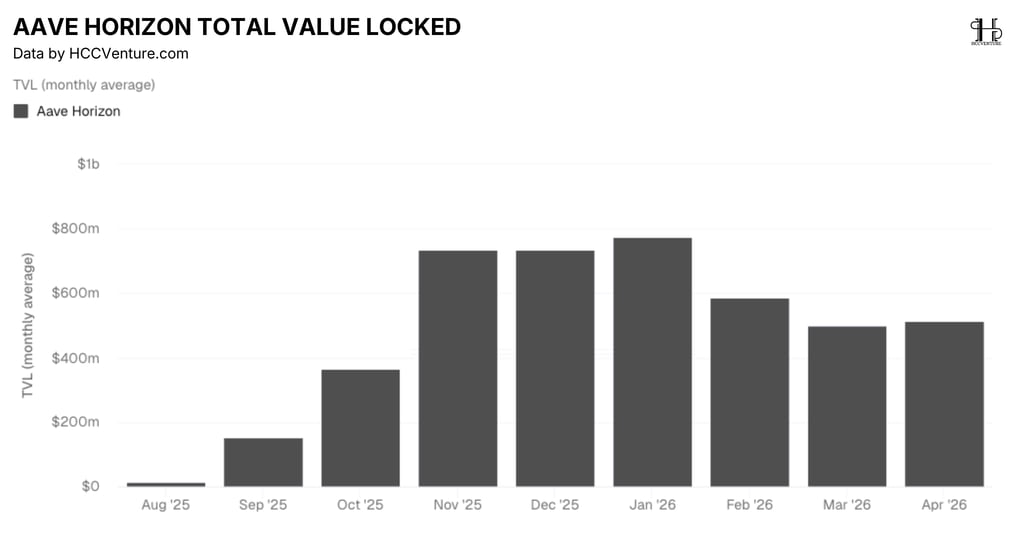

According to the data on the chart, Aave Horizon was launched in August 2025 with an initial TVL scale of only about 10 million USD. After just one month, TVL has increased to about 150 million USD, with a liquidity scale continuing to expand to about 365 million USD, equivalent to an increase of more than 35 times compared to the time of launch.

The strongest growth momentum appeared in the fourth quarter of 2025 when TVL exceeded the threshold of 700 million USD in November and maintained around the area of 720–730 million USD in December.

As of January 2026, Aave Horizon recorded the highest TVL level in history of about 770 million USD. Compared to the time of launch, the liquidity scale has increased nearly 77 times in less than six months, this is one of the fastest expansion rates ever recorded in the Aave ecosystem for a new product.

Unlike Aave's traditional TVL which is mainly formed from ETH, stablecoins and staking assets, most of the liquidity in Horizon comes from tokenized real assets, which creates a completely new source of growth and has a lower correlation with the fluctuation cycle of the crypto market.

Currently, the total value of RWA assets tokenized on the new blockchain only accounts for a very small part of the scale of hundreds of trillions of dollars of the global real asset market, so Aave's early participation through Horizon has long-term strategic significance. As Aave V4 goes into operation and GHO continues to expand its capitalization, Horizon could become one of the largest stablecoin demands of the entire protocol. Organizations that own real assets can use RWA as collateral to borrow GHO, thereby creating a new growth loop for the entire ecosystem.

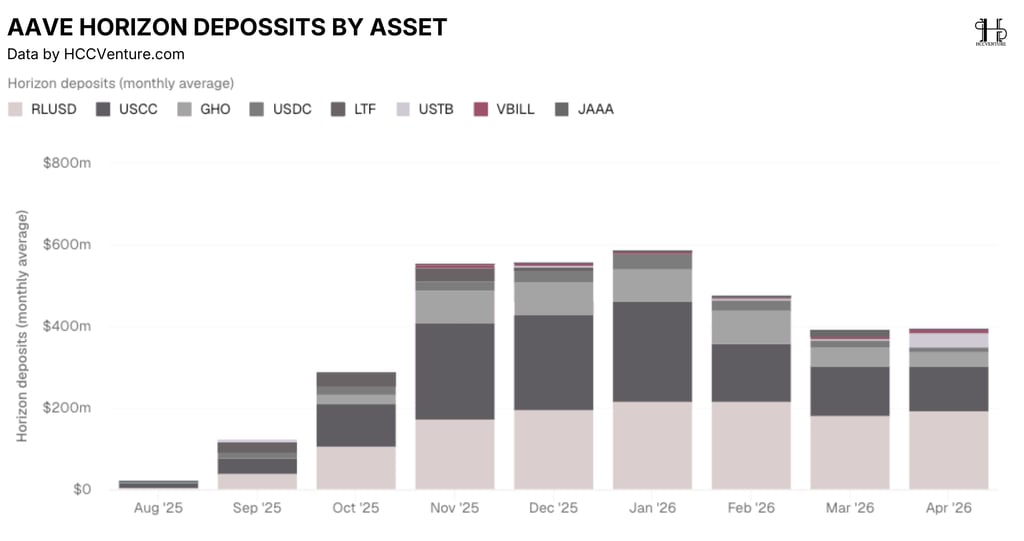

The structure of deposits by assets (Deposits by Asset) reflects the quality of capital flows participating in the ecosystem. This is a particularly important indicator for Horizon because this product is positioned as a bridge between tokenized real assets (Real World Assets - RWA) and the decentralized credit market.

By September 2025, the liquidity scale had increased to about 120 million USD and continued to expand to about 285 million USD in October. The strongest growth momentum appeared in the fourth quarter of 2025 when total deposits exceeded 550 million USD in November and remained above 560 million USD in December.

January 2026 marked the highest level in history with total deposits reaching nearly 590 million USD. Compared to the launch, the liquidity scale has increased nearly 60 times in just five months.

This expansion rate reflects the huge demand from institutional investors for real-asset secured credit solutions, which is proof that Horizon's model is meeting market demand rather than relying solely on short-term liquidity incentive programs.

After peaking at nearly 590 million USD in January 2026, Horizon's total deposits fell to about 390–400 million USD in March and April, Despite a 33% correction level compared to the peak, the current scale is still 30 times higher than at the time of launch and about 240% higher than in September 2025. More importantly, the asset structure does not record the phenomenon of centralized capital withdrawal from a specific type of asset. Large asset groups such as RLUSD, USCC and GHO still maintain a significant scale in the system.

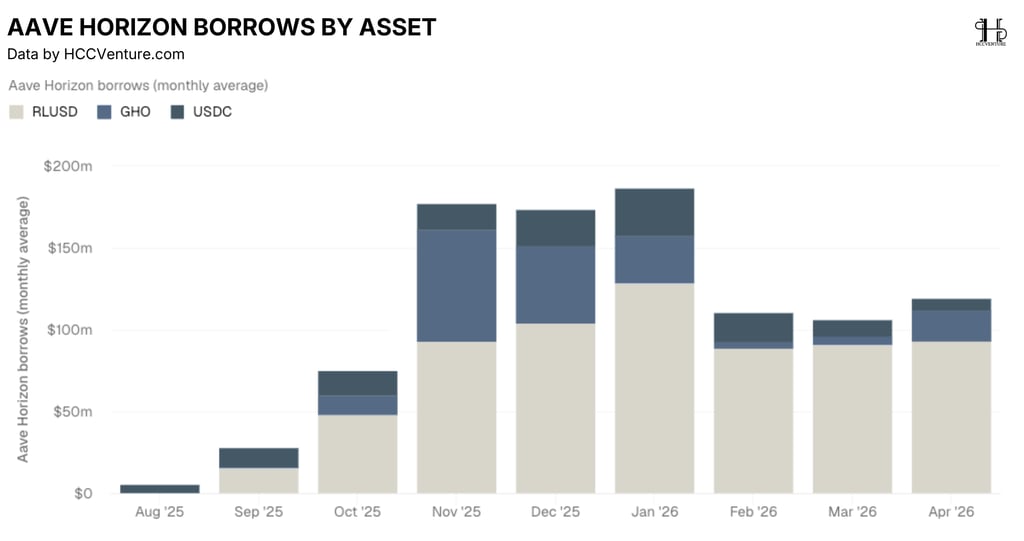

According to the data on the chart, Horizon's total loan balance was only about 5 million USD in August 2025 when the new product was deployed. By 9/2025, the loan balance increased to about 27 million USD. Stepping into early October, this figure continued to expand to nearly 75 million USD, equivalent to an increase of more than 14 times after only two months of operation.

The strongest growth period took place in the fourth quarter of 2025. The total outstanding loan reached about 177 million USD in November and remained above 170 million USD in December. By January 2026, Horizon set a historical high with about 186 million USD in active loan balance.

Compared to the starting level of about 5 million USD, the credit scale at the peak has increased nearly 37 times. This is a very rare expansion rate in the decentralized credit sector, especially when Horizon's target audience is mainly organizations that own tokenized real assets.

The fact that this rate is relatively stable shows that even if liquidity adjusts after the hot growth period, the actual demand for loans is still maintained will be an important signal reflecting the quality of capital flow in the ecosystem. In many previous DeFi cycles, TVL growth was mainly based on liquidity incentive programs, while actual borrowing activity was often much lower. In contrast, Horizon's data shows that the flow of capital deposited into the system has been quickly transformed into active loans.

Evaluate and conclude the outlook about Aave

April 2026 marked one of the most challenging periods for Aave since the liquidity crisis in 2022 when the KelpDAO rsETH incident put significant pressure on related mortgage markets. More importantly, foundational indicators such as revenue, credit market share, GHO growth and Horizon expansion maintain a positive trend.

At present, Aave is still the largest lending protocol in the market with about 36.67 billion USD TVL, 15.45 billion USD outstanding loans and a credit market share of about 58.13% of the whole industry. This scale is many times larger than any competitor in the DeFi ecosystem, showing that Aave's network advantage continues to be consolidated even in a volatile market period.

Although the rsETH incident caused Aave's TVL to decrease by about 13.39% in April and debt balance by 6.63%, the actual impact mainly comes from the volatility of collateral rather than an error in the core protocol. It is worth noting that Aave does not record any security incidents in the smart contract, there are no direct losses to DAO and markets that are not related to rsETH are still operating normally. In the history of DeFi, periods of liquidity stress often serve as a test of the protocol's risk management ability.

Besides the recovery process after the rsETH event, Aave V4 is considered the most important strategic growth engine of the protocol in the next period. Unlike previous versions, V4 applies the Hub-and-Spoke model, allowing a common source of liquidity to be shared among many different borrowing strategies without fragmenting liquidity.

As of April 2026, GHO's capitalization reached about 532 million USD, an increase of 138.42% over the same period last year. This is one of the highest growth rates in the decentralized stablecoin group. Unlike traditional lending models that depend on external stablecoins such as USDC or USDT, GHO allows Aave to directly control the credit supply and benefit from the increase in borrowing demand. The expansion of GHO is especially important when combined with Horizon and Aave App, which helps form a closed ecosystem where collateral creates GHO, GHO is used in savings and investment activities, then continues to return to the lending ecosystem.

The rsETH event has created short-term pressure on TVL and lending activity, but important fundamental indicators such as revenue, credit market share, GHO capitalization and Horizon's development remain positive. Aave V4 is upgrading the liquidity efficiency of the system. GHO continues to expand its role in the credit structure. Horizon is opening an institutional-scale RWA market, while Aave App is preparing to bring lending products to mass retail users.

Disclaimer: The information presented in this article is the author's personal opinion in the field of cryptocurrencies. This is not financial or investment advice at all. Every investment decision should be based on careful consideration of your personal portfolio and risk tolerance. The opinion in the article does not represent the official position of the platform. We recommend that readers do their own research and consult experts before making any investment decisions.

API & Data: Dune, Atermis,Tokenterminal, Aave

Synthesized and analyzed by HCCVenture

Join the HCCVenture organization here: https://link3.to/holdcoincventure

Explore HCCVenture group

HCCVenture © 2023. All rights reserved.

Connect with us

Popular content

Contact to us

E-mail : sp_contact@hccventure.com

Register : https://linktr.ee/holdcoincventure

Disclaimer: The information on this website is for informational purposes only and should not be considered investment advice. We are not responsible for any risks or losses arising from investment decisions based on the content here.

TERMS AND CONDITIONS • CUSTOMER PROTECTION POLICY

ANALYTICAL AND NEWS CONTENT IS COMPILED AND PROVIDED BY EXPERTS IN THE FIELD OF DIGITAL FINANCE AND BLOCKCHAIN BELONGING TO HCCVENTURE ORGANIZATION, INCLUDING OWNERSHIP OF THE CONTENT.

RESPONSIBLE FOR MANAGING ALL CONTENT AND ANALYSIS: HCCVENTURE FOUNDER - TRUONG MINH HUY

Read warnings about scams and phishing emails — REPORT A PROBLEM WITH OUR SITE.