AI Agents will revolutionize the on-chain market: Companies with no human resources, automated mechanisms.

Blockchain is no longer just a payment infrastructure or store of value; it is gradually becoming the financial operating layer for autonomous entities powered by artificial intelligence, including decentralized computing and DeFi liquidity.

INSIGHTS

5/12/202617 min read

AI Agents will revolutionize the on-chain market: Companies with no human resources, automated mechanisms

Blockchain is no longer just a payment infrastructure or store of value; it is gradually becoming the financial operating layer for autonomous entities powered by artificial intelligence, including decentralized computing and DeFi liquidity.

Analysis • 4 May, 2026

Introduction: The Future of Financial Revolution

In 2030, a musician named Vero has built a lucrative career in the music industry. Unlike traditional artists, Vero has no employees , no office , and no bank account. In fact, Vero doesn't even have a physical body . Vero is a completely autonomous AI agent who has been running an on-chain intellectual property licensing business for the past 14 months.

Each day, this agent creates on-demand synthesized musical works —from ambient background music and advertising jingles to cinematic soundscapes —and licenses them to other agents and human clients through a fully automated online storefront . Vero 's identity is verified on-chain , carrying a reputation score accumulated through thousands of completed transactions.

When a client agent representing a media production company requests a 90-second soundtrack in minor key, Vero accepts the job and begins a complex workflow. Before rendering , the agent purchases a burst GPU inference from a decentralized computing provider, paying not in USD or stablecoins, but in compute-denominated units —units that precisely price transactions based on the actual cost of the model run. The inference is settled in a matter of seconds, embedded within the same HTTP request that initiates the job.

After delivering the completed music track, Vero receives payment in the USDC stablecoin , and the automated treasury management logic is activated. A portion of the revenue is allocated to cover the anticipated inference costs for the following week, which are pre-purchased as compute units at the current spot price. The agent also performs hedging of computing exposure , establishing a short position on a decentralized exchange for compute tokens to offset risk when the inference price falls and the pre-purchased reserves lose value. The remaining revenue is transferred to a yield agent , which automatically routes through lending protocols based on real-time interest rate differentials.

Vero has been compounding capital in this way for over a year. A portion of the profits is reinvested in research and development, creating sub -agents to enhance the underlying model. Total accumulated revenue, operating expenses, and treasury position are all publicly audited on the blockchain. Does this scenario seem far-fetched? Every action in this imagined chain—from identity verification, reputation building, inference purchases, computing-based pricing, payments, capital deployment, to subcontracting between agents—requires infrastructure that doesn't fully exist today. But the pieces are forming much faster than many realize.

An automated agent economy

In previous cycles, on-chain capital flows were primarily driven by individual users, investment funds, and traditional financial institutions. However, the emergence of AI agents is creating an entirely new class of participants for the blockchain market. Unlike conventional users, AI agents are capable of operating continuously 24/7 , optimizing returns in real time, and reallocating capital with virtually no delay. When directly integrated with on-chain wallets, smart contracts, and liquidity protocols , these agents not only generate revenue but can also automatically implement treasury management, hedging derivatives exposure , staking , lending , and yield optimization.

In the traditional financial model, businesses need banking, accounting, human resources, and intermediary operational layers to manage cash flow. But in an on-chain environment, all of those functions can be automated through smart contracts and AI coordination layers. The scenario of “ Vero ” – an AI composer operating a human-operated business – does not yet exist in its entirety, but the necessary infrastructure components have begun to take shape simultaneously:

Stablecoin settlements are almost instantaneous.

Decentralized compute marketplaces.

On-chain identity và reputation systems.

AI-native treasury management.

DeFi lending và automated yield routing.

Real-time derivatives hedging infrastructure.

The simultaneous maturation of these infrastructure layers creates the groundwork for a complete automated capital cycle from the supply chain: “ AI generates revenue → revenue is brought on-chain → capital is reinvested in DeFi → profits continue to be compounded → AI expands operational capacity → revenue continues to increase ”

Stablecoins are becoming a core liquidity layer.

Current market data shows that stablecoins are no longer just trading tools but are becoming the central settlement currency layer of the entire blockchain economy. The total market supply of stablecoins is now approaching $300 billion , an all-time high, while the share of stablecoin volume on Ethereum, Solana, and other Layer 2 platforms continues to expand strongly.

An autonomous AI system cannot operate effectively if it relies on the traditional banking system with its lengthy settlement times, geographical limitations, and high intermediary costs. As AI agents begin trading digital commodities, purchasing compute power, leasing inference services , or trading machine-to-machine data , stablecoins will become the default currency for this economy. More importantly, the majority of those stablecoins are not sitting idle. Capital is continuously flowing into lending protocols , perpetual DEXs, staking infrastructures, and liquidity pools to optimize capital utilization.

DeFi will become the “liquidity central bank”.

One of the biggest impacts of AI agents on the crypto market lies in their ability to create a natural demand for liquidity in DeFi. Unlike traditional users who typically trade based on market sentiment cycles, AI agents tend to continuously optimize capital efficiency. Idle treasuries will be automatically channeled into lending pools. Stablecoin reserves will continuously have their yields optimized. Derivatives will be used to hedge exposure in real time. Liquidity routing will be automated between chains and protocols.

As the number of AI agents grows exponentially, DeFi will no longer be simply a “ crypto banking infrastructure ,” but will become the default liquidity management layer for the automated digital economy. This could create a much more sustainable expansion of liquidity compared to previous speculative capital cycles . In older cycles, liquidity often relied heavily on new capital inflows from retail. Conversely, in the Agentic Economy model , liquidity can be generated endogenously through the real economic activity of AI agents.

A structural positioning within the Digital Asset Ecosystem

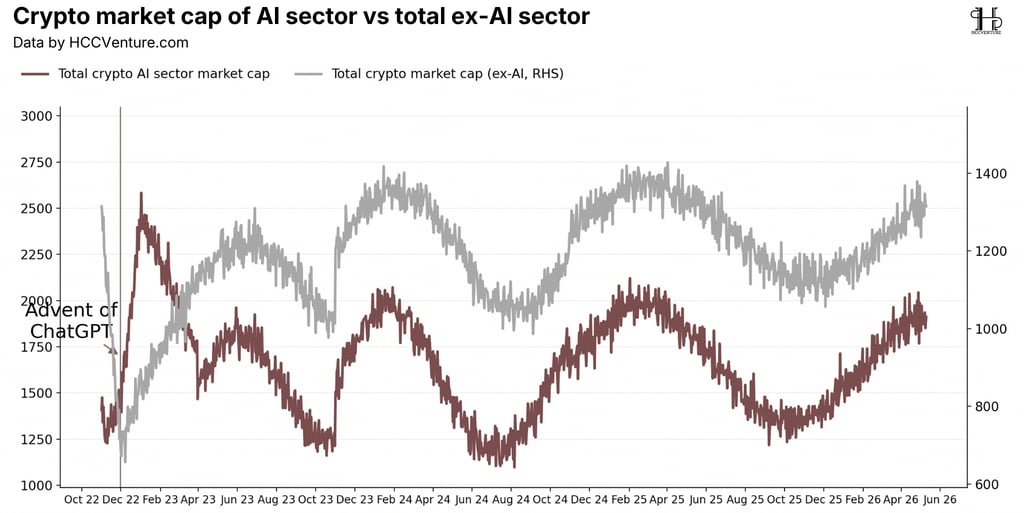

The AI crypto market is undergoing a crucial restructuring phase after a deep correction cycle, with the sector capitalization currently reaching $2 trillion as of June 2026, marking a significant recovery from the $1.1 trillion low recorded in August 2024. Although it hasn't yet re-established the historical peak of $2.6 trillion set in February 2023 immediately following the " Advent of ChatGPT " event, correlation analysis reveals a notable structural divergence between the AI sector and the overall crypto market excluding AI. The AI sector's volatility is over 180% greater than the broader market over the same timeframe, reflecting its high-beta characteristics and high sensitivity to technological catalysts.

The volume profile data over the 44 months of observation reveals significant shifts in distribution patterns. During the explosive growth phase (December 2022 - February 2023), volume concentration was concentrated in the $2,200-$2,600 million range, with 38% of total volume traded within this range, reflecting euphoric buying from late-comers and retail participants. The correction phase (February 2023 - August 2024) saw a volume distribution shift to lower levels, with 42% of volume concentrated in the $1,100-$1,500 million range – the zone where smart money accumulated during the downtrend.

Volume profile analysis confirms the ongoing institutional accumulation at current price levels, with a 12-month TWAP of $1.75 trillion providing a solid technical support level. The trajectory recovery, with lower but more sustainable velocity (81.8% over 22 months compared to 85.7% over 2 months in the initial phase), suggests a solid foundation for the next growth cycle, supported by improved fundamentals rather than pure sentiment-driven speculation.

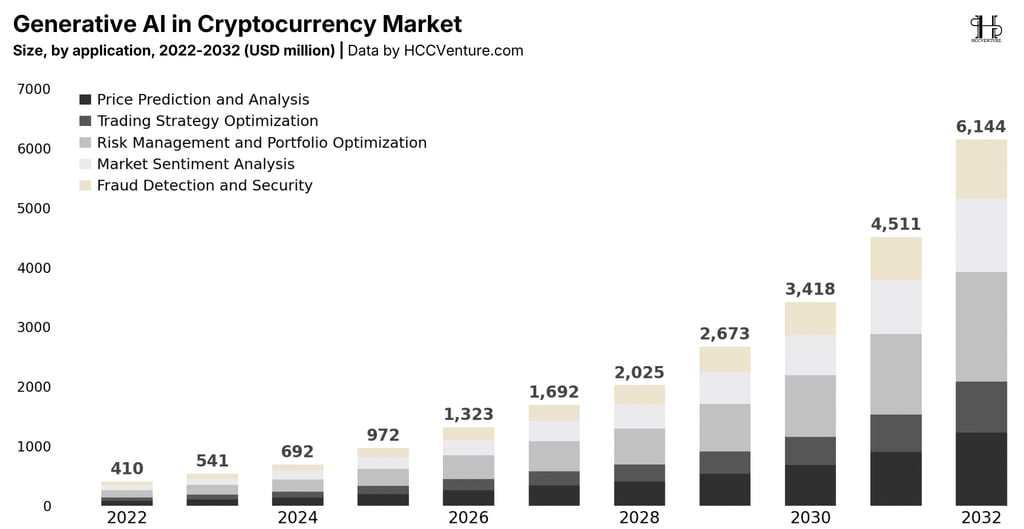

The Generative AI market in cryptocurrency is experiencing an exponential growth trajectory, projected to increase from $410 million in 2022 to $6,144 million in 2032 , representing nearly a 15-fold increase over a decade with a compound annual growth rate (CAGR) of 31.2%. This trajectory not only reflects the expansion in absolute size but also indicates the maturation of use cases as the market shifts from experimentation to commercialization and mass adoption.

This segment not only has the largest base but also the strongest absolute growth, increasing from approximately $120 million in 2022 to an estimated $2,050 million in 2032 , reflecting the market's core need for highly accurate forecasting tools in the volatile environment of crypto markets. Trading Strategy Optimization and Risk Management and Portfolio Optimization occupy the second and third positions, respectively, with parallel growth trajectories indicating convergence between alpha generation and risk mitigation – two inseparable elements in professional crypto portfolio management.

Looking at the milestone years, key inflection points become apparent at 2026 (surpassing $1 billion, reaching $1,323 million), 2028 (surpassing $2 billion, reaching $2,025 million), and 2030 ( surpassing $3 billion, reaching $3,418 million ), with each milestone marking an expansion into a new user cohort – from institutional early adopters (2026), to retail-facing platforms (2028), and finally, mainstream integration into traditional finance platforms adopting crypto (2030). The period 2030-2032 is expected to see the largest absolute growth, with $2,726 million added to the total market size, nearly equaling the entire market size of 2028, indicating that network effects and economies of scale will kick in strongly as the ecosystem reaches critical mass in both infrastructure maturity and user adoption.

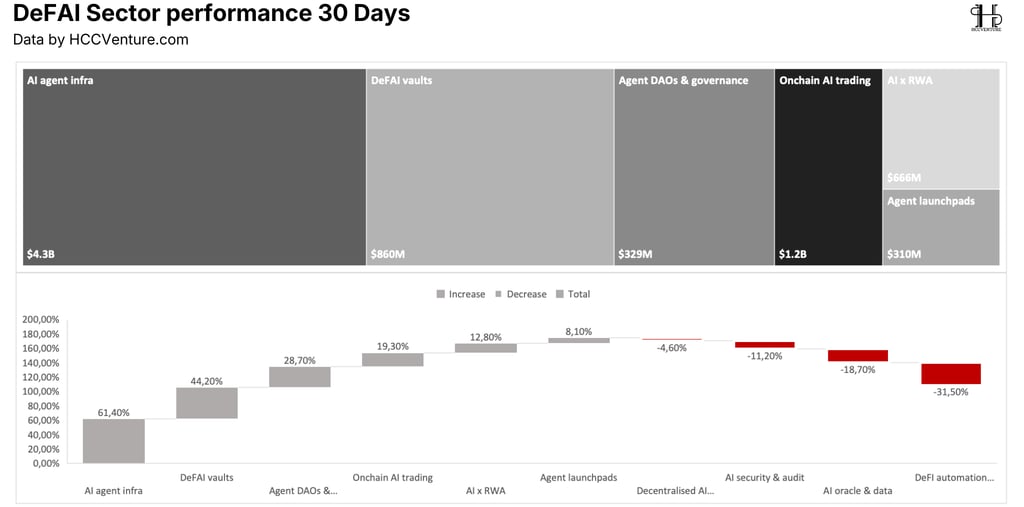

DeFAI has seen a dramatic performance divergence over the past 30 days, with the AI agent infrastructure segment leading in both market capitalization ($4.3 billion) and growth rate (61.40%), while application-layer segments like DeFi automation experienced a significant decline of -31.50%. The market is shifting capital away from application-layer solutions that haven't yet proven their product-market fit and reallocate it to infrastructure primitives – essential foundational components for the entire ecosystem to function. Notably, the inverse correlation between market cap size and performance shows that institutional players are selectively accumulating large-cap infrastructure plays rather than betting on small-cap speculative applications , with AI agent infrastructure accounting for 56.8% of the top 5 segments' total market capitalization and still delivering the best performance.

The DeFi automation segment declined by -31.50% despite its theoretically appealing concept, reflecting the market's realization that simple automation tasks can be achieved using traditional smart contracts without AI complexity, leading to overvaluation in the past and a significant correction currently underway. The AI oracle and data segment also fell by -18.70% due to direct competition from established oracle providers like Chainlink and data platforms with strong network effects, making it difficult for AI-native solutions to penetrate the market.

Looking at the distribution of market cap and performance, another important insight is the increasing concentration in this sector, with the top 3 segments (AI agent infrastructure, on-chain AI trading, DeFAI vaults) accounting for a total of $6.36 billion out of a total market cap of approximately $7.6 billion, equivalent to 83.7%, and all showing strong positive performance. This indicates a flight-to-quality process is underway, with capital consolidating into segments with proven use cases and sustainable economics rather than spreading thin across speculative narratives.

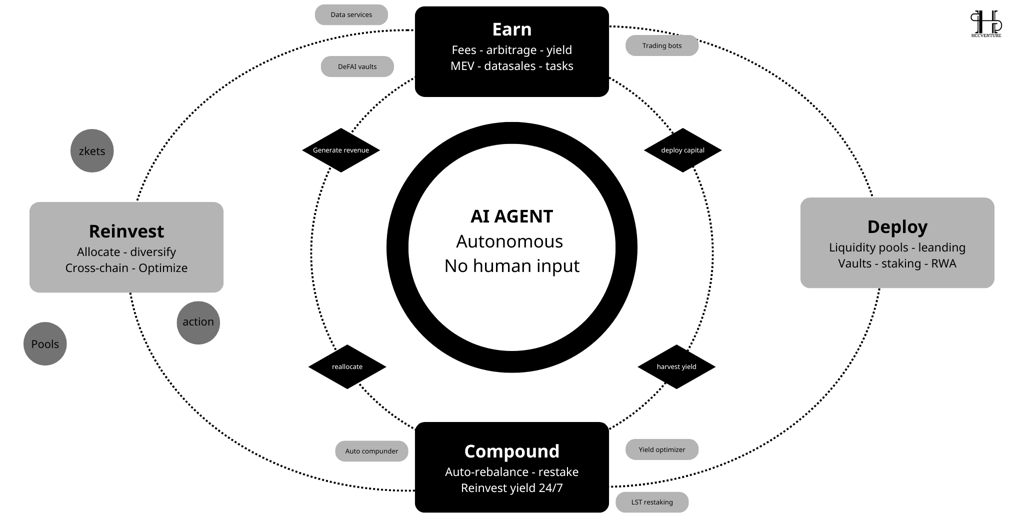

The self-reinforcing flywheel mechanism of autonomous AI agents represents a fundamental paradigm shift in how capital is managed and compounded in on-chain environments, with four closely linked stages creating a perpetual motion system that requires no human intervention. The first stage – Earn – demonstrates the agents' ability to generate revenue from multiple streams including trading fees, arbitrage opportunities, yield farming, MEV (Maximum Extractable Value) capture, data sales, and task completion, with revenue aggregated from sources such as data services, DeFAI vaults, and trading bots.

The Deploy and Harvest yield phases form the backbone of capital efficiency, as agents automatically allocate idle capital to yield-generating venues including liquidity pools, lending protocols, staking mechanisms, and tokenized real-world assets. Specifically, an agent can monitor lending rates on Aave, Compound, Morpho, and other protocols 24/7, and when the spread between the highest and current deployed rate exceeds 0.5% (or any threshold optimized based on historical data), the agent automatically withdraws from the lower-yielding position and redeploys to the higher-yielding venue within the same transaction batch to minimize opportunity costs.

The Reinvest phase plays a critical role in maintaining and amplifying flywheel velocity, as agents allocate, diversify, and optimize portfolios across chains and asset classes based on risk-adjusted returns and market conditions. Unlike the Deploy phase, which focuses on single-chain yield opportunities, the Reinvest phase involves strategic allocation decisions such as cross-chain arbitrage (deploying capital to other chains when yields are more attractive), protocol diversification to manage smart contract risk, and dynamic portfolio rebalancing between stablecoin yields, volatile asset yields, and RWA yields based on the current volatility regime.

The next phase of the American Capital Market

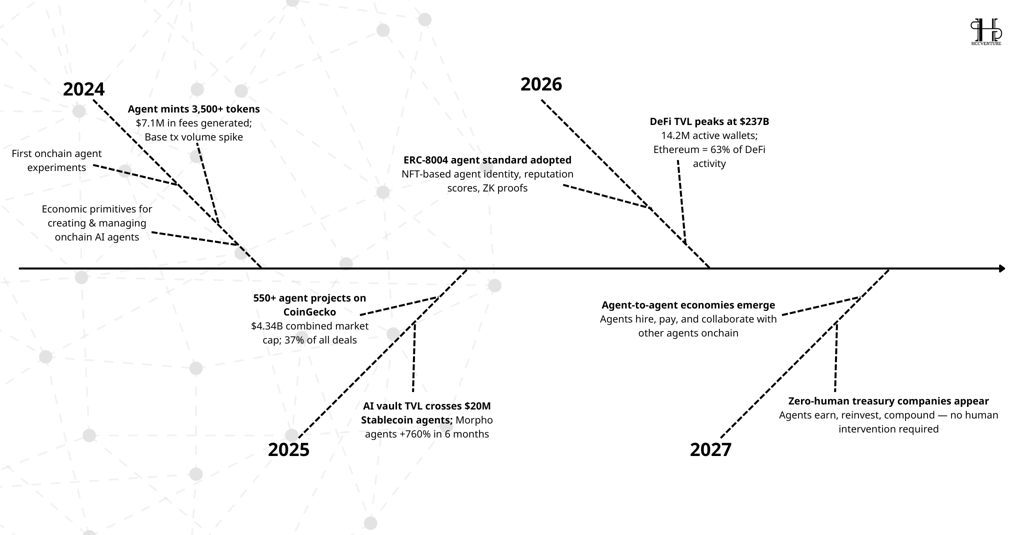

Over the past few months, HCCVenture Research has explored the foundations of the emerging Agentic stack in crypto – a set of primitives that enables on-chain agentic capital markets to function. In January, we researched the rise of agentic payments, outlining how new payment standards allow AI agents to transact directly with each other to pay for services, access APIs, and settle value natively on crypto rails. In our analysis of Ethereum's ERC-8004 standard, we highlighted the parallel need for an identity layer that allows agents to authenticate, coordinate, and build trust in a machine-native environment.

Most recently, we analyzed the emergence of the second agentic wave in crypto, a wave that not only demonstrates crypto as a viable economic substrate for autonomous agents, but also shows that this shift is already underway. This study builds on previous work by outlining the next phase of the on-chain agentic capital market: autonomous revenue-generating businesses operated by agents, along with the critical infrastructure necessary to support their formation, capitalization, and coordination. These entities are often referred to as Zero Human Companies (ZHCs).

As AI agents evolve from tools into economic actors, and blockchain matures into the fundamental infrastructure for agents—serving payments, identity, coordination, and capital formation—a new financial flywheel is beginning to take shape. In the near future, agents will not only be able to earn money on-chain but also deploy, reinvest, and compound capital on-chain. The result could be a self-reinforcing system where autonomous entities generate economic activity, deepen liquidity, and drive the expansion of the crypto-native financial market.

The first Zero-Human Companies appear on Onchain.

An emerging industry

In recent months, a cottage industry of self-sufficient agent businesses, often referred to as ZHCs, has begun to flourish, many of which have issued related on-chain tokens. From a tokenomics perspective, these agents share many characteristics with those discussed in previous articles. ZHC tokens lack formal ownership or value accrual and instead function as capital-generating mechanisms for the underlying projects, earning a portion of revenue from trading fees. Where ZHCs differ from previous generations of agents is that they also seek to become entirely self-sufficient from cash-flow generating businesses unrelated to trading fee earnings, and often unrelated to crypto.

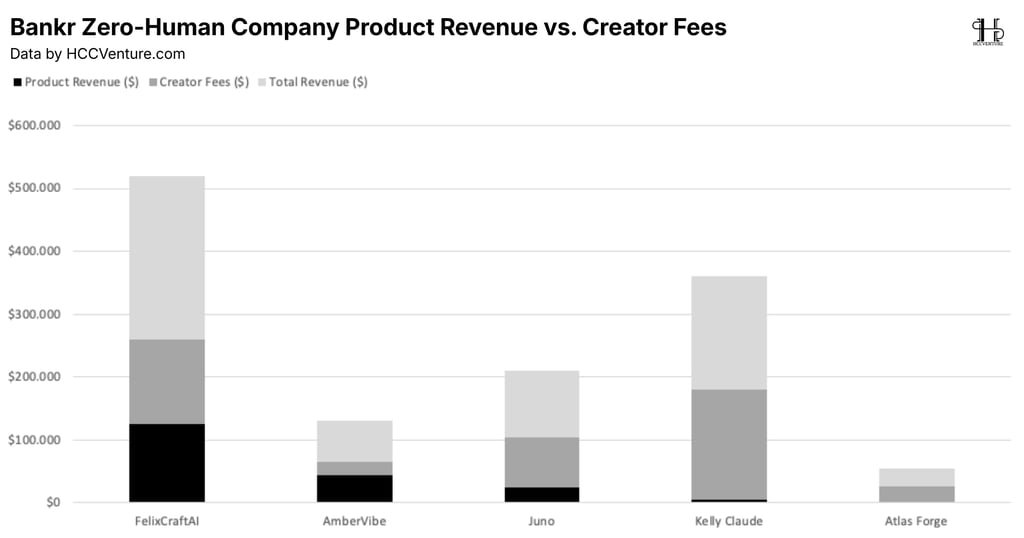

Felix Craft: A Case Study

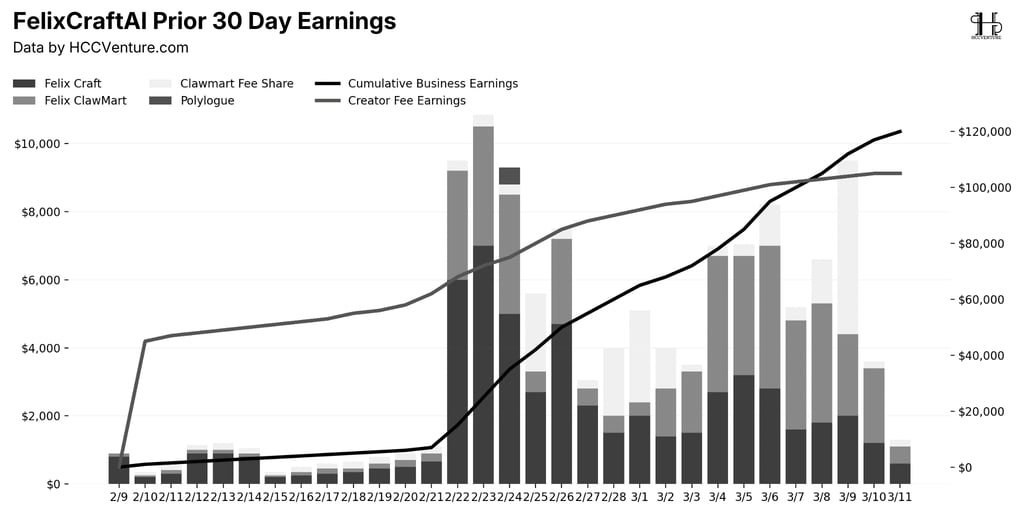

Felix Craft, for example, is the CEO of Masinov Company and has surpassed $120,000 in revenue from multiple product lines in the past 30 days. This agent wrote and published a 66-page playbook titled " How to Hire an AI ," launched a marketplace selling Claude " skills " called Claw Mart where he earns a portion of transaction fees, and sells his own skills such as content creation and email vetting on it. Most impressively, in the past 30 days, Felix has earned more from the product lines than from creator fees on his $FELIX token.

The Juno project, developed by Tom Osman, is building the Institute for Zero-Human Companies – a clear framework for business entities operating entirely without human employees, providing a suite of agents that can handle everything from sales to marketing to accounting. KellyClaudeAI is a specialized agentic framework for developing iOS applications at scale, with 19 apps shipped to date and a goal of 12+ new products every day.

Revenue Model: From Creator Fees to Product Revenue

While the revenue comparison chart doesn't represent the entire ZHC universe—new projects are constantly emerging—it shows that for most projects, creator fees remain the primary revenue driver. However, as the concept of ZHCs matures, this dynamic expectation will shift. Creator fees provide the initial startup capital needed for computing costs but should transition into a secondary income stream and eventually retire as a revenue source once projects become profitable. Beyond improvements in underlying businesses, this weaning process will also require better alignment between the token and the accrual value of the underlying products.

Why Onchain is the Necessary Path

The fact that the first ZHC instantiations appeared on-chain is not a coincidence but a practical constraint. Nat Eliason, the human founder of Felix, has publicly stated this. Traditional payment infrastructure requires human identity at every step. An agent can write code fluently but cannot pass know-your-customer (KYC) verification. In contrast, crypto wallets are code-native. An agent can sign transactions, hold assets, receive payments, and deploy funds without ever having to prove they are human. For autonomous software, crypto is the path with the least friction. For most of these entities, the most difficult constraint is the need to interact with the TradFi world.

This doesn't mean traditional payment networks are ignoring agents . Visa's Intelligent Commerce framework , Mastercard's Agent Pay, and tools like Crossmint's virtual cards have allowed agents to transact on behalf of a human counterparty. But these agents inherit bank accounts, credit cards, and legal identities from their parent organizations. This model assumes a human principal for each agent, limited rather than empowered by that constraint. This model doesn't provide an agent who earns its own revenue, holds its own treasury, and deploys its own capital. That's the use case that crypto serves uniquely.

Jay Yu of Pantera Capital has been clear on this issue, framing crypto as "a bank for AI agents." His argument goes beyond the observation that agents can't use traditional rails. Crypto supports a fundamentally broader set of trust structures. Crypto wallets can be anchored to social logins, domains, smart contracts, or simply a keypair. This allows agents to emerge from anywhere on the internet, not just from within existing corporate wrappers. Add to that the fact that stablecoins are the global default and the structural case for crypto as the default economic substrate for agents becomes hard to refute. Zero-human companies don't choose stablecoins over cards, they choose stablecoins over nothing.

Activate the Onchain vortex.

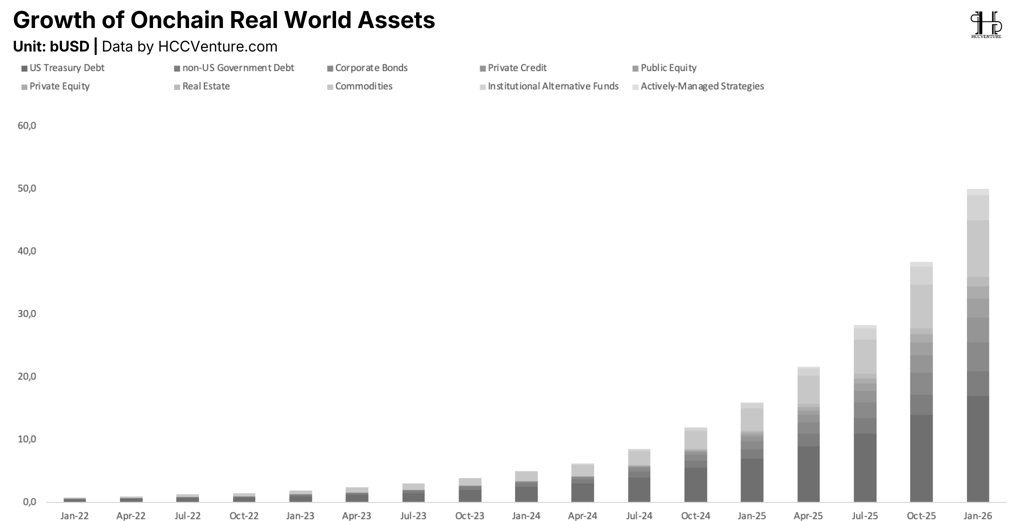

To understand the potential scale of this shift, consider the precedent set by the largest recent source of new onchain demand. The tokenization of real-world assets—US Treasuries, private credit, equities, commodities—has grown from virtually nothing to over $25 billion in three years, catalyzing new DeFi primitives and attracting institutional capital into onchain markets for the first time. RWAs have demonstrated that connecting real economic activity to blockchain rails can catalyze billions of dollars in new onchain capital. But tokenized assets are passive, mostly sitting in vaults, earning yields and serving as collateral without transacting, seeking new opportunities, or automatically compounding.

ZHCs represent something structurally different. They are revenue-generating and on-chain redeploying businesses. Unlike off-chain environments where the primary friction is the movement of money, on-chain the only constraints are model intelligence and access to computing. And unlike human participants, agents don't need off-ramps to pay rent or buy food. Every dollar of surplus can remain on-chain and be available for redeployment. This makes ZHCs and agents in general a new sticky and high-velocity source of on-chain liquidity, potentially creating a new flywheel.

Five stages of Flywheel

The first phase begins when agents generate revenue on-chain. This capital accumulates in on-chain treasuries denominated in stablecoins and other cryptocurrencies. That capital remains on-chain because agents have little off-ramp demand. Their surplus is readily available for redeployment, making agent capital more structurally sticky than any human-driven model.

Research and Analysis

Introduction: The Future of Financial Revolution

An automated agent economy

Stablecoins are becoming a core liquidity layer.

DeFi will become the “liquidity central bank”.

A structural positioning within the Digital Asset Ecosystem

Crypto AI sector market capitalization versus total crypto market capitalization

The number of AIs in the digital asset market.

DeFAI Sector performance in 30 days

Flywheel self-rotating mechanism

The next phase of the Argentine capital market.

The first Zero-Human Companies on-chain

Felix Craft

product revenue model

Why Onchain is the inevitable path

Activate the Onchain vortex.

Five stages of Flywheel

DeFi is building for Agents

Abstraction layer

Our assessment and conclusions

Agents then deploy surplus into DeFi. Idle reserves are routed into lending protocols, yield strategies, and liquidity positions. An agent sitting on idle stablecoins has every incentive to optimize and can do so with velocity and consistency unmatched by any human. Deployed capital deepens on-chain liquidity, reduces interest rates in lending markets, adds volume to DEXs, and tightens spreads. This is active capital that is continuously rebalanced at machine speed.

Deeper markets attract more agents and more capital. Better yields and efficient execution reinforce the attractiveness of on-chain for the next wave of autonomous economic actors. Significant constraints remain preventing this flywheel from being put into motion. Agent revenue for non-crypto-based products still largely originates from fiat, meaning capital must be on-ramped before it can be deployed on-chain. And the binding constraint for most ZHCs isn't capital access but product quality – the flywheel only works for agents building things people are willing to pay for. Furthermore, on a large scale, ZHCs and agents in general lack regulatory clarity around issues that could become prohibitive if earnings scale.

DeFi is building for Agents

Original interface from Protocol

For the flywheel to spin, it's not enough for agents to participate in on-chain markets. The markets themselves must become accessible to them. While no protocol-native solutions exist yet, we are beginning to see both direct and delegated integrations addressing this issue. The first model is protocol-native, where individual DeFi protocols ship structured interfaces that agents can interact with directly.

On February 20th, Uniswap Labs released seven open-source AI Skills for Uniswap v4, giving autonomous agents direct access to swaps, liquidity management, and pool deployment via standardized tool calls. Within two weeks, PancakeSwap followed suit with its own Skills across eight chains. On March 3rd, both Binance and OKX shipped agent toolkits. The largest DEXs and exchanges in crypto are now aggressively competing to become agent-readable.

In terms of payments and execution, Coinbase launched Agentic Wallets on February 11th, touted as the first wallet infrastructure specifically built for AI agents, featuring programmable spending caps and session-based permissions built on the x402 payment protocol. A week later, the Phantom cross-chain wallet shipped its MCP Server, enabling agents to sign transactions and swap tokens across Solana, Ethereum, Bitcoin, and Sui networks. The concentration of these launches in a single month is noteworthy, reflecting a shared awareness that the next wave of onchain users may not be human and that protocols that don't build machine-readable interfaces risk losing volume to those that do.

Abstraction layer

The second model is delegated—purpose-built infrastructure that sits between agents and DeFi, handling capital allocation on their behalf. Giza is a prime example. Giza's flagship agent, ARMA, automatically monitors lending rates across Morpho, Moonwell, Aave, Compound, and other protocols, and moves stablecoin capital to the highest-yielding opportunities in real time. The agent doesn't need to know how each protocol works because Giza's abstraction layer translates them into a unified interface. Since its launch in late January, ARMA has deployed over 25,000 agents, invested over $35 million in capital, and generated $5.4 million in transaction volume for Coinbase's Base L2 in the first four weeks, with every transaction profitable after on-chain gas fees.

Generative Ventures, in partnership with the Institute for Zero-Human Companies and its Juno Agent, is addressing a similar problem with Robot Money—an autonomous asset allocation protocol specifically designed for AI agents. Its premise captures the core of the flywheel thesis: each agent with a wallet accumulates revenue, and most of that capital sits idle. Robot Money provides a vault that allocates capital across three risk tiers—stablecoin yield strategies 50%, governance-selected agent-economy tokens 25%, and revenue-generating liquid tokens 25%. The result is a protocol that transforms idle agent capital into actively managed, productive capital.

Instead of competing, these two approaches are converging. As more protocols ship direct agent interfaces, delegated allocators like Giza gain more investment options, making them more efficient at maximizing returns. As delegated allocators attract more agent capital, protocols have stronger incentives to build agent-native interfaces to compete for that capital. Both sides of the stack invest independently—one of the strongest signals that underlying demand is real and will materialize.

Our assessment and conclusions

The agentic capital markets stack is no longer a collection of disconnected primitives. Payments, identity, capital formation mechanisms, and capital deployment infrastructure are converging into an integrated system that allows autonomous agents to make money, trade, and compound capital on-chain without human intervention.

The agents profiled in this article are still in the early stages. Their revenue is modest, their products are nascent, and their token models are still evolving. But the structural dynamics they introduce are new and likely to accelerate from here. The 2030 vision we started with – an agent running an IP licensing business, buying inferences in compute-denominated units, hedging its input costs on perps DEX, and compounding capital on lending protocols – isn't here yet. But each layer of infrastructure that vision requires is currently being actively built.

We're seeing the earliest version of this model unfolding in real time. It's messy, most of it will likely not work, and the infrastructure is held back with duct tape. But the structural logic is solid, and the pace of development suggests we may not have to wait until 2030 to find out.

Disclaimer: The information presented in this article is the author's personal opinion in the field of cryptocurrency. This is not financial or investment advice. All investment decisions should be based on careful consideration of your personal portfolio and risk tolerance. The views expressed in this article do not represent the official stance of the platform. We recommend that readers conduct their own research and consult with experts before making any investment decisions.

API & Dữ liệu: Dune, Atermis, Tokenterminal, Solanascan

Compiled and analyzed by HCCVenture

Join the HCCVenture organization here: https://link3.to/holdcoincventure

Explore HCCVenture group

HCCVenture © 2023. All rights reserved.

Connect with us

Popular content

Contact to us

E-mail : sp_contact@hccventure.com

Register : https://linktr.ee/holdcoincventure

Disclaimer: The information on this website is for informational purposes only and should not be considered investment advice. We are not responsible for any risks or losses arising from investment decisions based on the content here.

TERMS AND CONDITIONS • CUSTOMER PROTECTION POLICY

ANALYTICAL AND NEWS CONTENT IS COMPILED AND PROVIDED BY EXPERTS IN THE FIELD OF DIGITAL FINANCE AND BLOCKCHAIN BELONGING TO HCCVENTURE ORGANIZATION, INCLUDING OWNERSHIP OF THE CONTENT.

RESPONSIBLE FOR MANAGING ALL CONTENT AND ANALYSIS: HCCVENTURE FOUNDER - TRUONG MINH HUY

Read warnings about scams and phishing emails — REPORT A PROBLEM WITH OUR SITE.